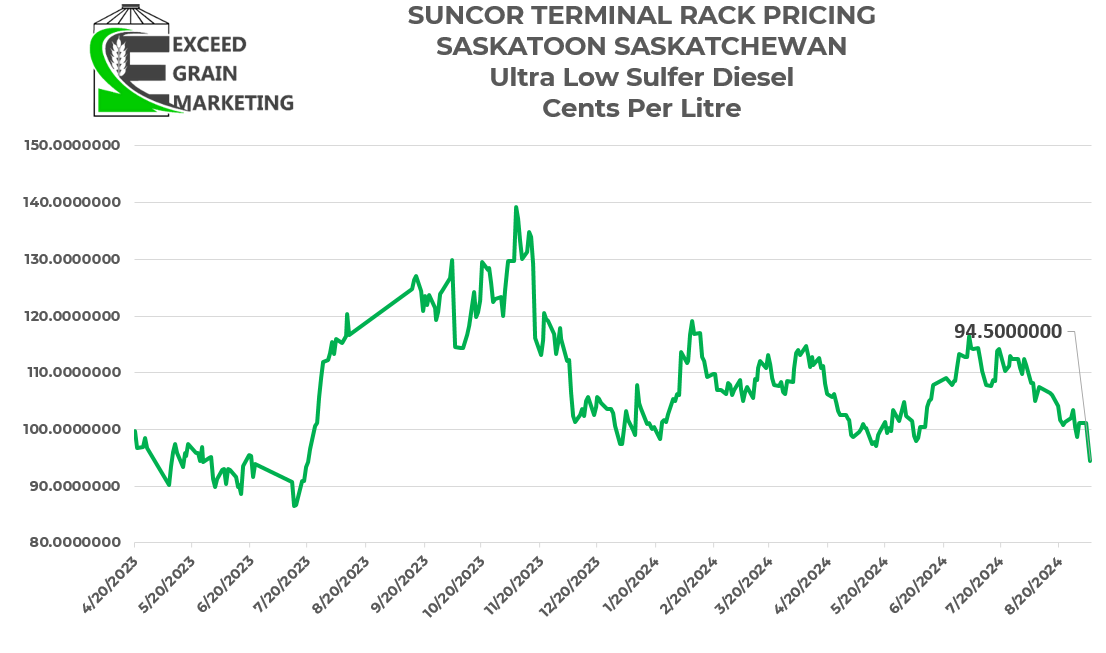

Western Canadian Crop Market Update

Click Here To Access 2024/25 Crop Recommendations

Canola

- Updated Feed Barley and Yellow Pea recommendations in tab above. Click green link above to access.

- Canola suffered this week from news of China launching and Antidumping probe into Canadian canola on Tuesday morning. Canola traded limit down on the news before closing down $20 per tonne.

- The Antidumping investigation is likely linked to the Electric Vehicle and US steel tariffs launched by Canada in late August.

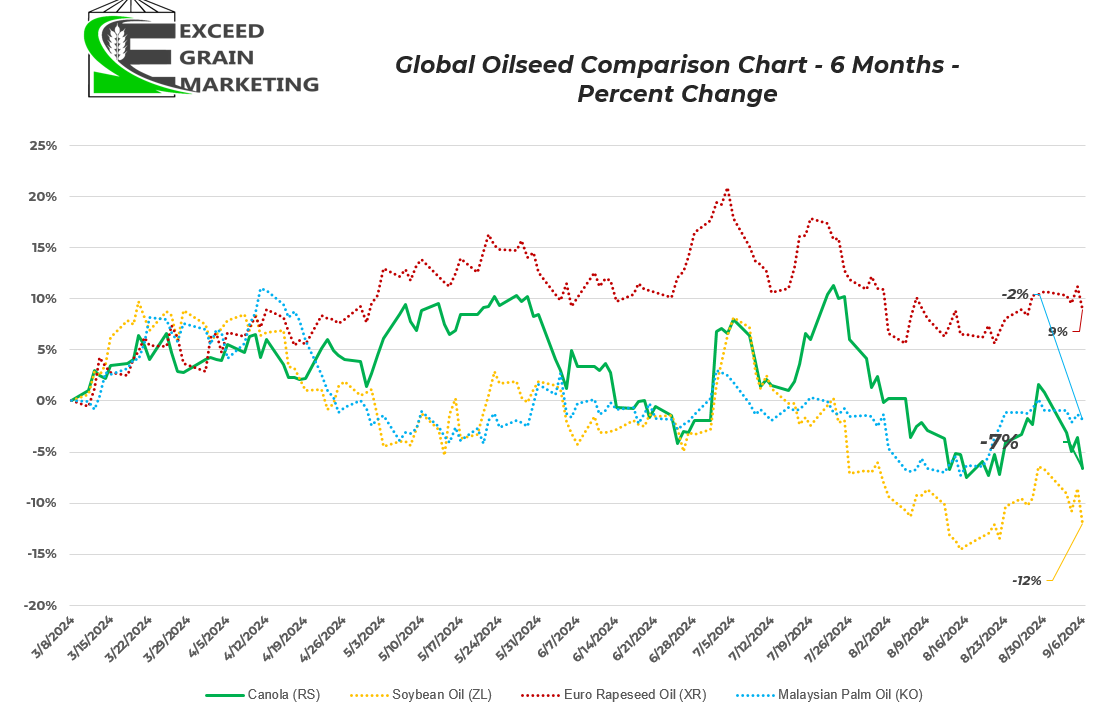

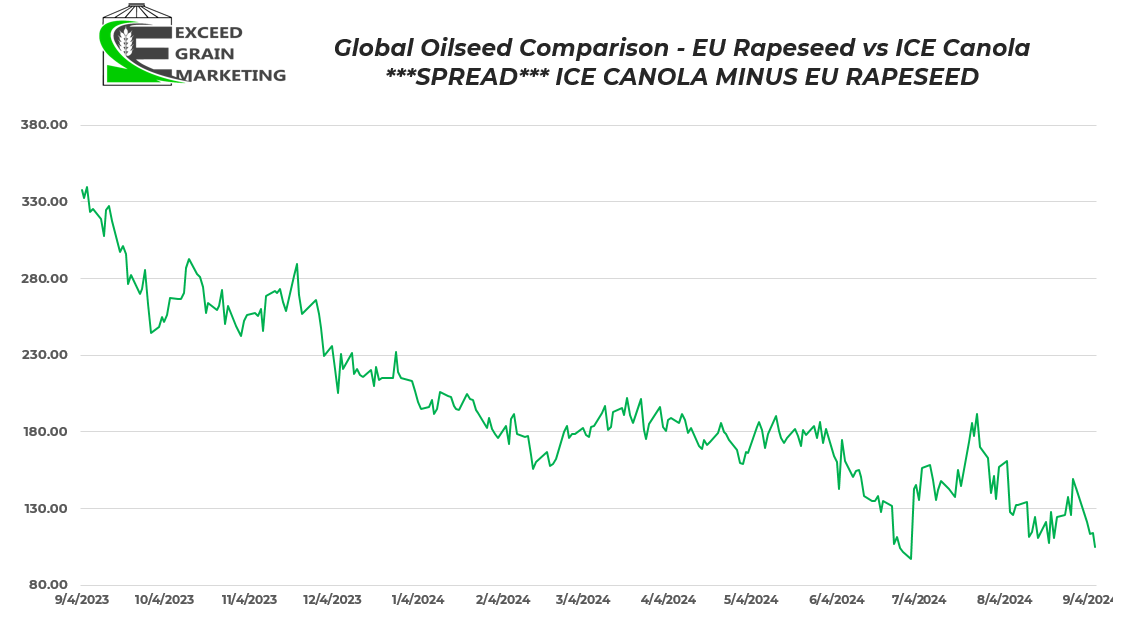

- Canadian canola some of the cheapest FOB origins globally, this time last year, canola was some of the most expensive.

- We have been seeing some consistent overnight sales of US Soybeans into China for new crop production in the past two weeks, we are still behind pace on soybeans but Corn sales sales starting to look like export program could pull together here.

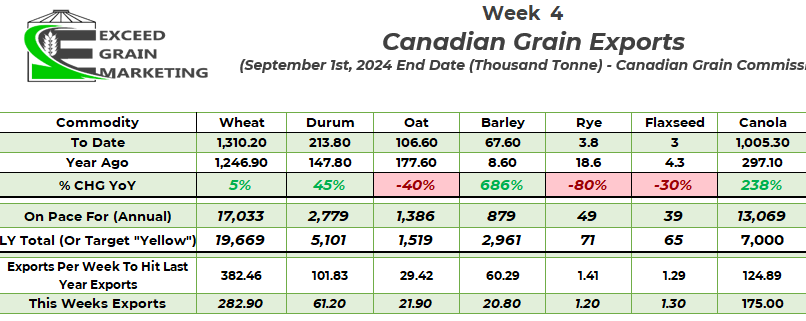

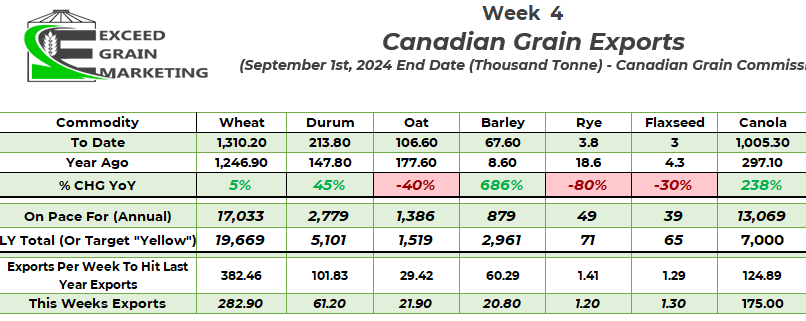

- Canada does not have any system for reporting sales, only reports actual exports. After week 4 of the marketing year, we have moved out over 1 mmt. 297,000 was the figure last year so a much better start to the marketing year.

- 485,000 tonnes sitting in port export position so should be a steady flow to begin with., a good start to an export program. This is exactly what we were missing this time last year, export program was not good by any standards.

- Exporters need consistent rail export capacity, looks like that issue is resolved for the time being, but picture is not 100% clear.

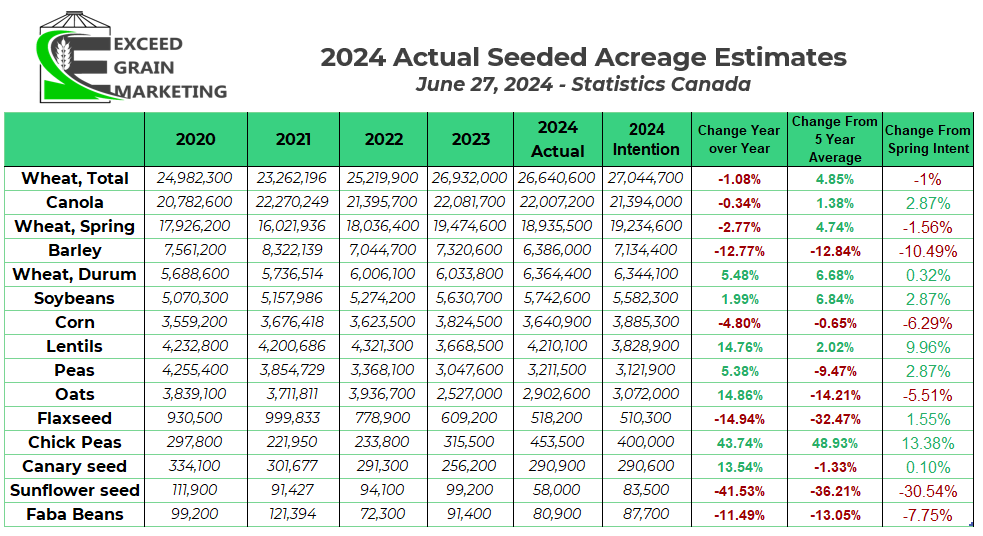

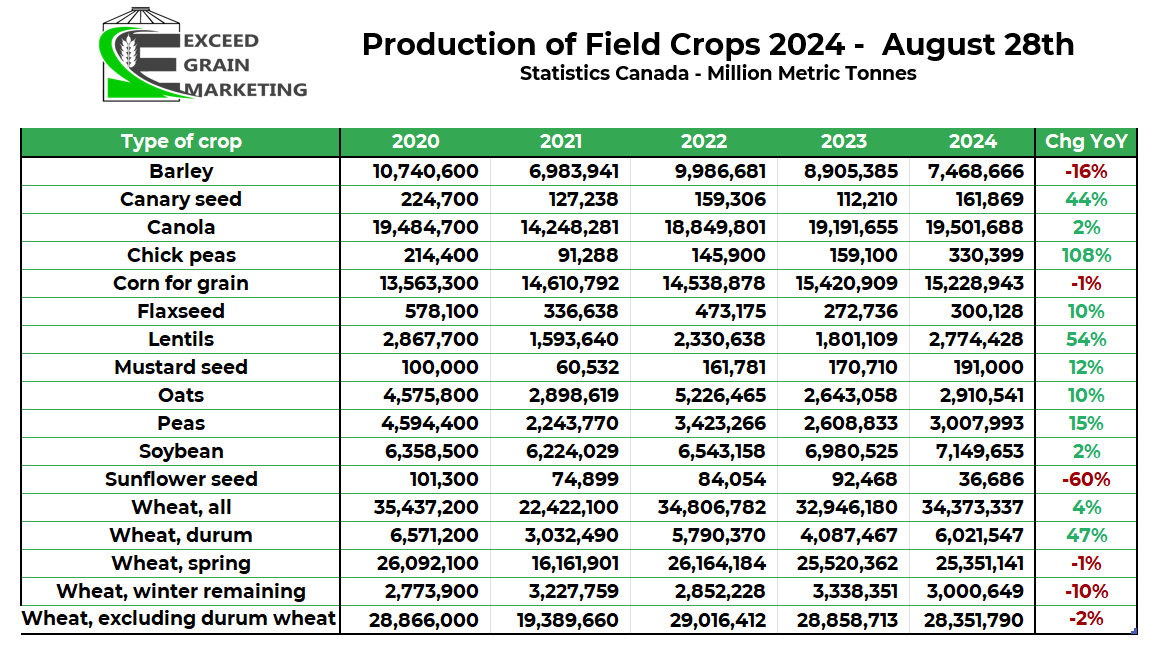

- New crop canola was available to the market starting September 1st. Initial yields coming in below expectations and has most private analysts sitting at 19mmt crop or less. Stats Canada put out a 19.5 mmt figure

- Overall market sentiment understands that we have a large Corn and Soybean crop coming in the United States.

- United States soybeans FOB sitting at some of the cheapest values in the globe. North American grains in general very cheap and we will need some impressive usage / export numbers to incent traders to take their fingers off the sell button.

- Overall sentiment towards ag commodities has been negative with Corn and Soybeans both hitting contract lows in recent sessions as well.

- For the short term, rallies need to be sold into if producer is undersold. Know your position and where you want to be sold. Opportunities will need to be capitalized upon in short order. Work with your advisor to “stickhandle” cashflow, logistical and other requirements.

- PRODUCTION:

- Western Canadian Crop forecasted to be larger than last year. USDA forecasting a 20mmt crop for Canada.. Most private analysts have the crop at 19.5mmt or smaller at the start of August but are quickly pushing the number closer to a 19mmt figure. Stats Canada at 19.5mmt

- The top end yield has been trimmed. Many producers reported a great start to the crop but things dried out in the past 4-6 weeks and heat came intensely during this same timeframe. Crop coming in smaller than anticipated.

- Very early canola yields mostly below expectations with pockets of good.

- EXPORTS and USAGE:

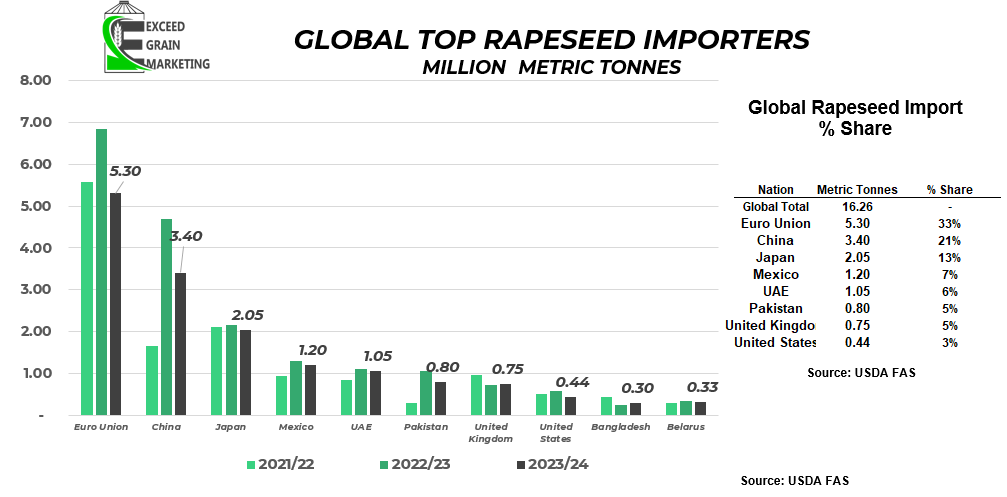

- European Union forecasting a smaller crop than last year and harvest is getting close to wrapped up. Crop estimates from government agencies state around 19mmt crop. Private sources call the European crop closer to 18mmt. EU needs around 25mmt total and larger imports will be required. Canada exported next to nothing this past marketing year to EU. Through the first 11 months of the crop marketing year, we exported 103,000 tonnes to Belgium. Few years ago, it was not uncommon to do 500,000 to 1.5 mmt in years where EU faced crop shortfall.

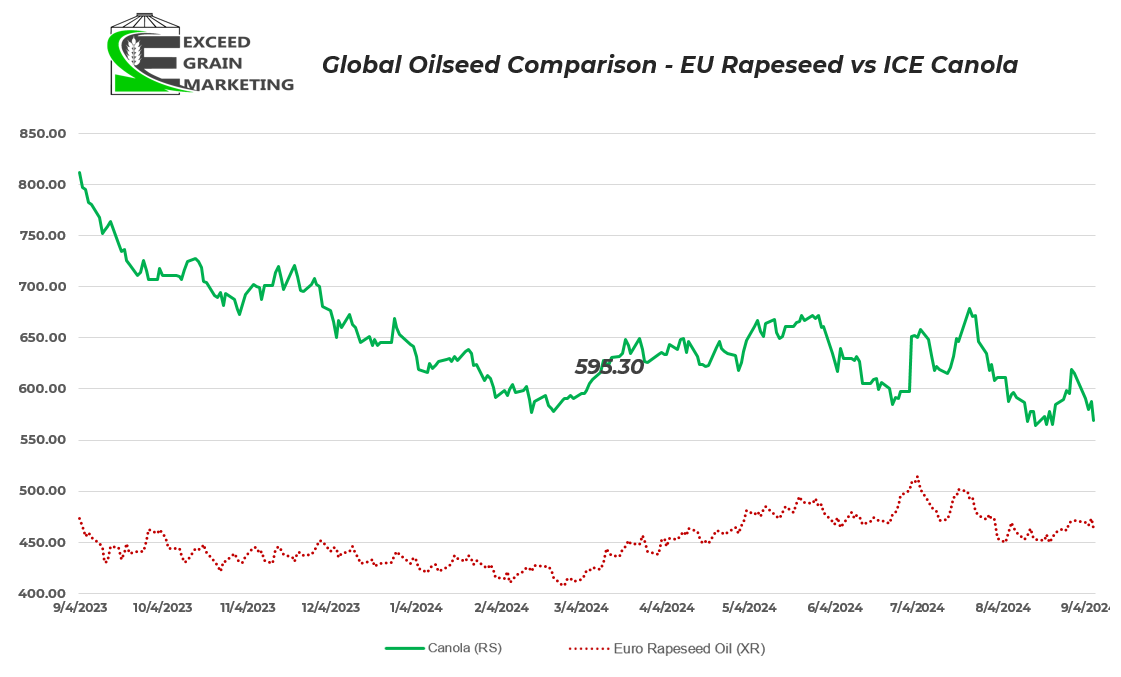

- OLD CROP: For the 2023/24 canola export program, Canadian canola was much to expensive to compete with Australian Canola for the first half of the export program. By early January, Canadian canola exports were only tracking for 6mmt of total exports, a dismal export number. It was not until exports picked up last half of the year where we came in right around 7mmt.

- AAFC has 2024/25 export forecast at 7.0 mmt. This is viewed as a conservative figure, many private analysts sit around 8.0 mmt assuming Japan, Mexico and European Union will likely be in for more crop, time will tell.

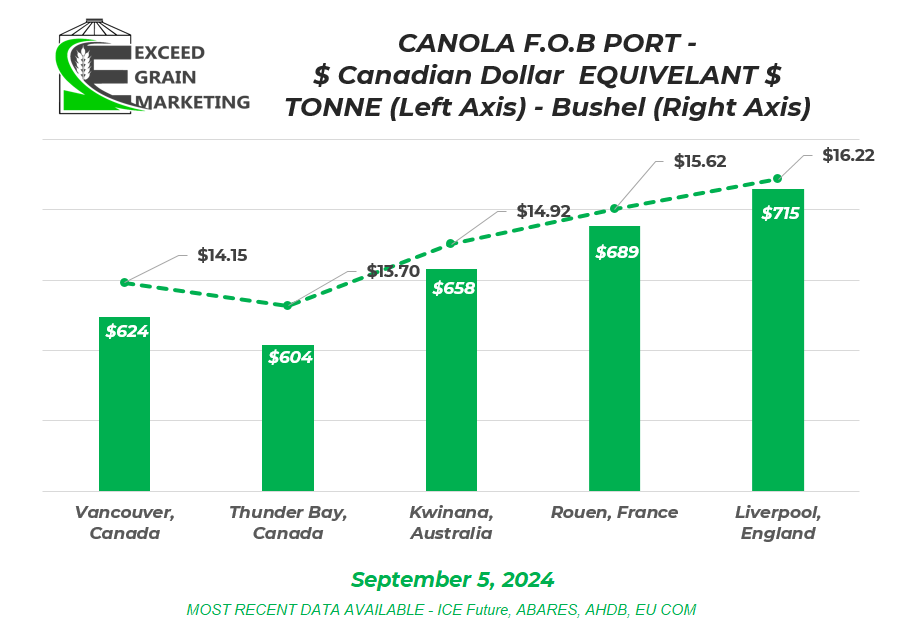

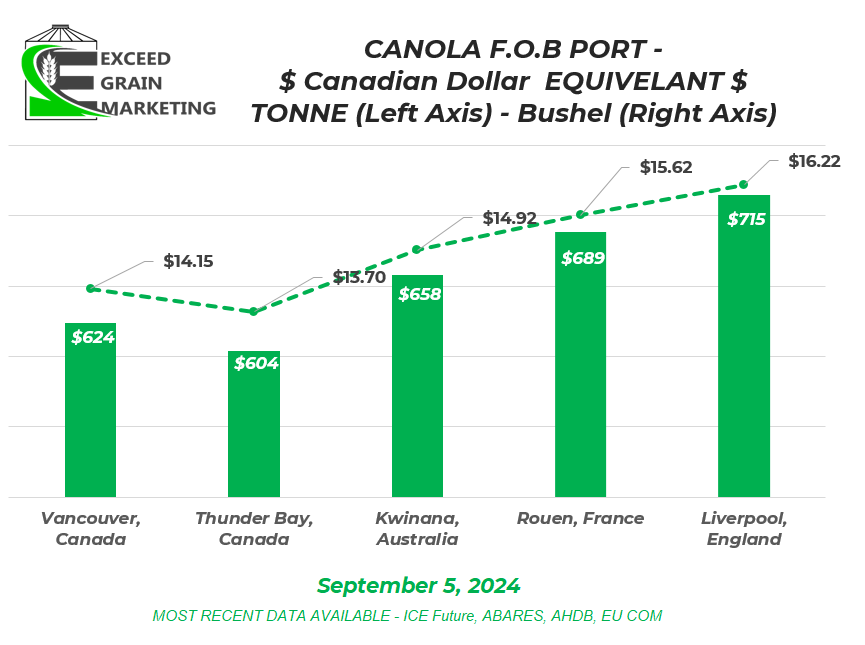

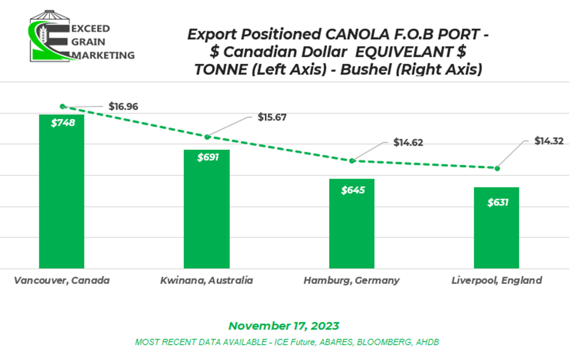

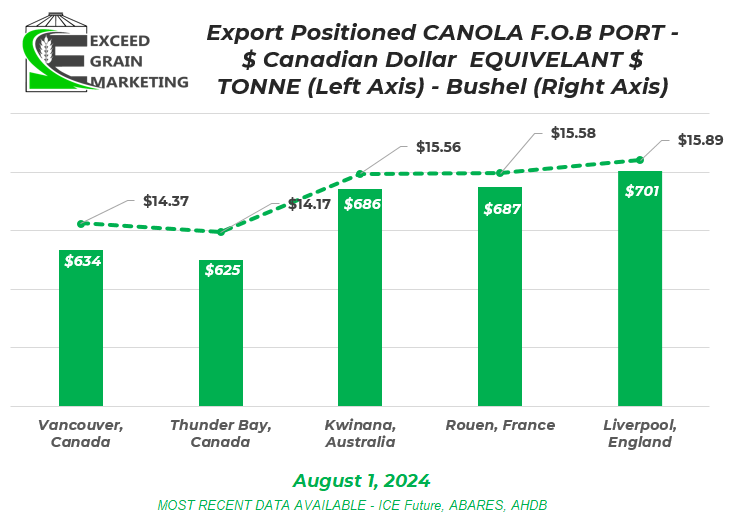

- See Global FOB canola prices chart above and historic ones below.

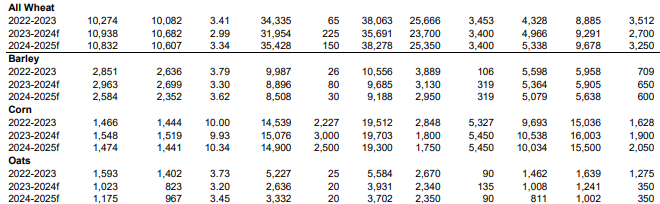

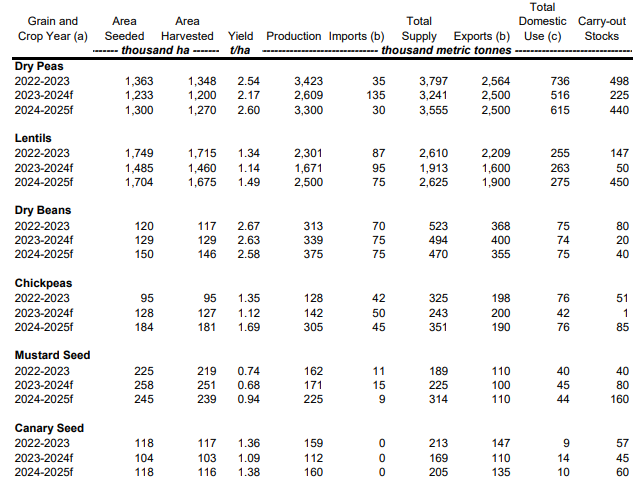

- AAFC Charts below from July 22, 2024 report.

- GOING FORWARDS:

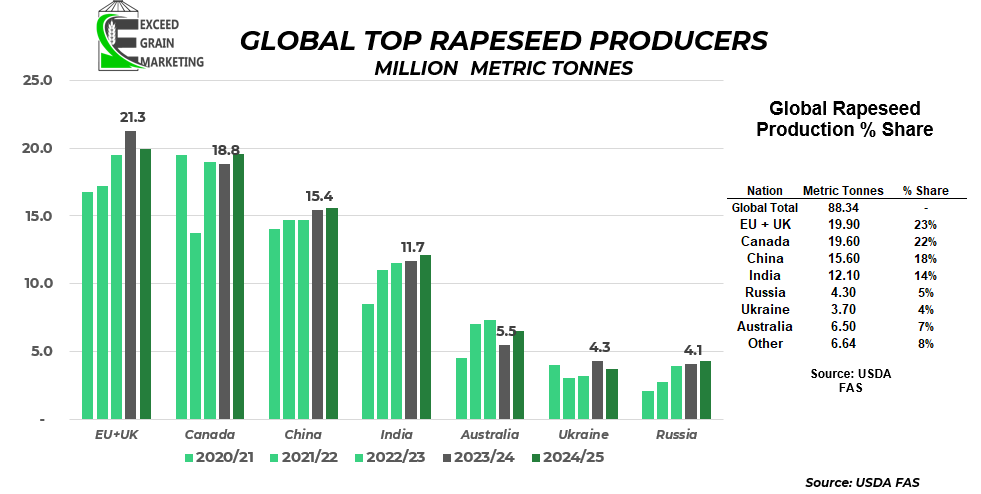

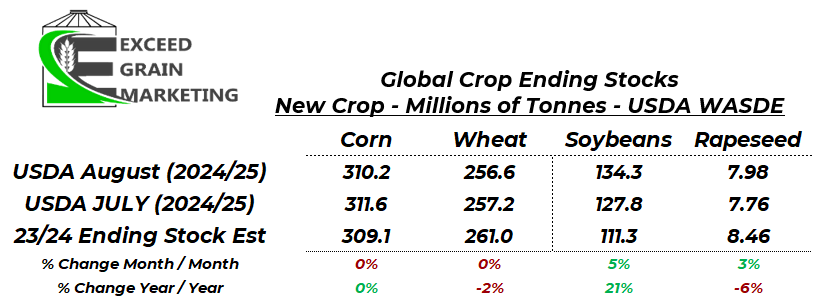

- Harvest is in full force. It is key that traders get a good start to the canola export program. Which shows promise so far. Chinese trade spat will cause logistical headaches going forwards. Global Rapeseed and Canola balance sheet has potential to tighten up longer term, ending stocks already shaping up 9% smaller than last year according to USDA figures. Will mostly depend on what Canadian canola crop comes in at. We know other global production regions well enough already as harvest underway. Early yield reports showing lighter than earlier anticipated

- Australian crop the wildcard here, although their crop is expected to be 200,000 tonnes smaller than last year. This crop is in the ground and will be harvested Oct/Nov/Dec. 5.5 mmt

Spring Wheat

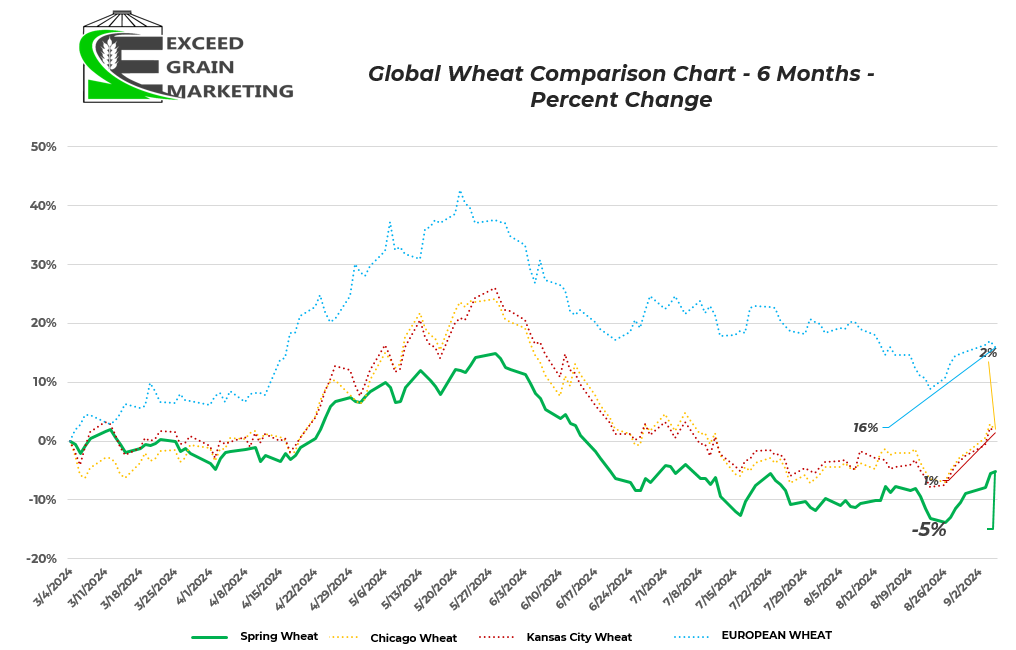

- Spring Wheat values found some strength with a 7 day jump in futures values before settling lower into the Friday trade. Good quality and abundant yield being reported in northern United States. Cereal values weighted down in general.

- Spring Wheat futures still sit about $2.00 USD per bushel from their late May peak

- Wheat, Corn and Soybeans all sitting near levels last seen in 2020 and making new contract lows in recent weeks before some strength through the first part of the week

- Markets have been in a downwards trend since the end of May. No weather stories and prospects of a potential record yield from North Dakota, the largest Spring Wheat producing state in the USA

- For the short term, rallies need to be sold into if producer is undersold. These rallies will be more challenged as we get closer to harvest. Know your position and where you want to be sold. Really work closely with your advisor on your general marketing plan, decide what crops need to move and what crops we are keeping at home. Weight the risk and reward of each decision.

- PRODUCTION:

- Canadian non durum wheat crop expected to be large. 1.2 mmt larger than last years crop. Around 29MMT is expected to be produced according to AAFC’s latest stab at the crop size. Looks like ending stocks could be more burdensome than earlier forecasted as well.

- Wheat will come down to quality. Protein levels and quality will be closely watched. Plenty of producers concerned about potential fusarium infection due to rains around heading and anthesis.

- Early harvest wheat quality in Western Canada is not good at all. Lightweight is the main issue. Protien looks alright so far, Some disease is prevalent.

- Global production – Winter wheat crop is off in the United States. Quality was quite good and plenty of good yields reported. US Spring wheat harvest will commence shortly but majority of fields will be ready to go mid August. Market expects a good crop, private tours are touting it to be a record yield in North Dakota.

- Across the pond, wheat quality is questionable at best. Some multi decade low wheat yields being reported in Germany and France Plenty of low protein wheat coming off fields in Russia, Ukraine, Germany, France, Poland. Grading issues a concern over rains at harvest especially in France and Germany.

- French wheat is forecasted by private analysts at around 25 mmt. Last year the crop was closer to 35mmt

- EXPORTS and USAGE:

- Global balance sheet for wheat actually tightest in several years. Ending stocks of 257 million tonnes vs 260 to 285 mmt range in recent years. Balance sheet amongst key exporters even tighter.

- Ukraine entered Russia’s Kursk region early August, first true offensive onto Russian soil since the war began.

- Canadian exports last year were particularly strong, not due to cheapness, but due to the quality of the crop. We need some good new crop quality coming into the system to give us the blending capacity we need. Canadian crop was blended and fit a gap in the market. Exporters looking to hit the same niche this year and push wheat exports as strong as they were last year.

- AAFC has 2024/25 export forecast at 20.5 mmt. This is viewed as a strong year and will keep ending stocks in check.

- AAFC Charts below from July 22, 2024 report.

- GOING FORWARDS:

- Harvest is in full force, wheat prices are at some of the lowest levels in 4 years. We are 30% sold new crop overall and will await quality results before making next cash sale move.

Corn

Soybeans

Oats

- Western Canadian oat production is trending to the light side. Some early oat harvest having trouble hitting spec for 2CW. 3CW is prevalent.

- Oat prices are sit at $3.75 to $4.50 new crop across the prairies. The $4.50’s belong to the glyphosate free market. Oat market prices have followed other ag commodities lower. Oats were anticipated to have been heavily sold by producers early in the production year when values were about $0.50 to $1.00 per bushel higher than todays values.

- Oat crops loosing top end yield with the heat and dryness. Test weight is an issue with lack of any precipitation towards the end of the filling period. Oat balance sheet could tighten up if yield losses come to fruition. North East sask and Western Manitoba will call the shots on this crops balance sheet. Early harvest not great for weights

- Lowered yield sentiment in recent weeks should keep oat inventories in check. Front end demand is largely covered off for oats although and pricing will depend on post harvest demand and how this crop actually shakes out. AAFC is calling for a carryout of just 350,000 tonnes which would be considered very tight. Private analysts are higher but adjusting balance sheets lower in recent weeks.

Barley

- End users / Maltsters came out of the gate early with bids and appear to have covered off front demand. Malt supply issues are prevalent. High Protein is a problem and some problems have maltsters and exporters keeping bids firm. Central Sask exporter bids increased around $0.25 this past week.

- Maltsters will need to be nimble here to source the proper supply they need.

- Corn is the Achilles heel to feed barley pricing. Corn is very cheap and even with barley values about 40% lower year over year, it still struggles to find competitiveness into feed rations. Barley is pricing into Alta feedlots competitively right now, but walks a fine line with corn.

- Exports are not expected to be anything special as we largely lost a pile of market share to the Australian market exporting into China.

- Malt is the play this year and grade at harvest will dictate price sentiment. Early malt bids are still holding place, slightly increasing.

Pulses

- Lentil yields are coming in across western Canada. Good portion is off, less than earlier anticipated in most cases. Balance sheet revisions will be made lower than they were in early July. Some small pockets reporting way above average yields but more common than not to see less than anticipated yields. Some grade issues, disease.

- Global demand will be the key factor here. A few key sales to export markets will dictate the balance sheet massively come the end of the marketing year.

Durum

- Durum harvest well understood in western Canada. Yields leaning to the disappointing side from prior estimates and light weights are commonplace. There are plenty of grade issues. Disease showing itself this year as some rains fell at prime time for disease timing. Crop easily smaller than July estimates. Grade will be the stickhandling part of marketing this crop.

Flax

- Flax production is forecasted to be quite small this year with less acreage going into the ground. In fact, Flax acres are the smallest since the mid 1940’s. Flax prices will be influenced by EU demand. Russia’s flax crop will be challenged to move into EU borders this year due to new import tariffs that began on July 1st for flax which will be scaled up in the coming years.

Our market intelligence reports incorporate information obtained from various third-party sources, government publications, and other outlets. While we endeavor to maintain the highest standards of accuracy and integrity in our reports, we acknowledge that the information provided may contain inadvertent errors or omissions. As such, we accept no liability for any inaccuracies or missing information in the data presented. Furthermore, these reports are not intended to serve as standalone investment or financial advice. We strongly advise that any financial or investment decisions be made in consultation with a professional market advisor. Reliance on the content or forecasting provided within of our reports for making financial decisions without such professional advice is at the sole risk of the user.