Exceed Grain Marketing’s Client Exclusive report is dedicated to covering the ongoing trends and significant highlights within the local market, while simultaneously offering a perspective on the global landscape. This approach ensures a comprehensive understanding of the factors influencing the market at both local and international levels. Our aim is to deliver current, up-to-date information specifically tailored to the crops impacting your operation. Work with your Exceed Grain Marketing advisor to devise specific strategies that may work for your crop.

MARKET HIGHLIGHTS

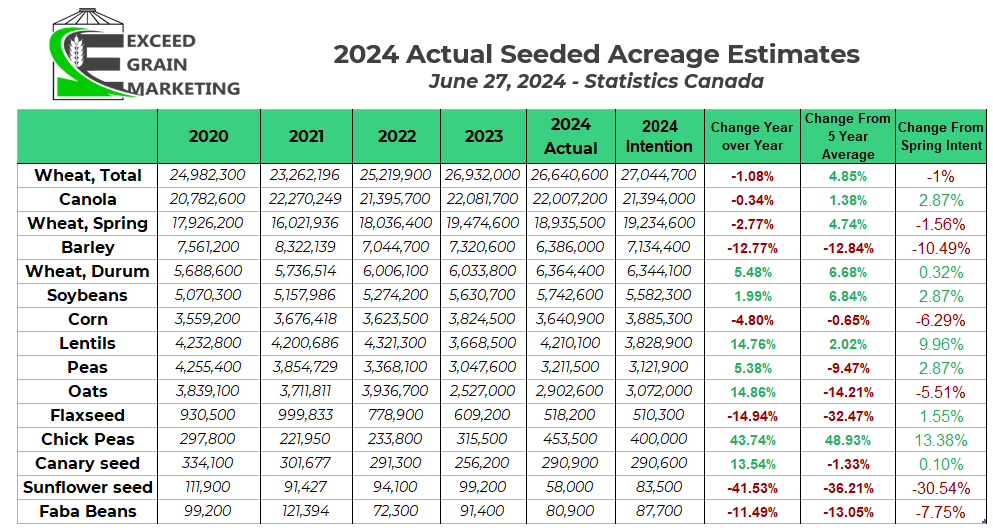

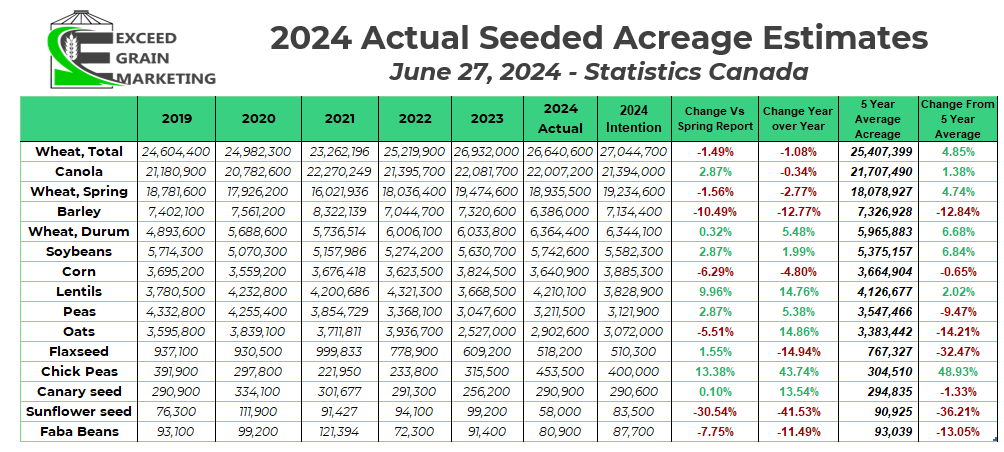

- Link to June 27th Statistics Canada Acreage Full Coverage

- 2024/25 Crop Year Recommendations – Click Link

- We advanced our Canola Sales Recommendation for old crop early last week. See Rec Page at bottom of report for further details. Work with your local grain marketing advisor to find best fit for your operation or strategy going forwards

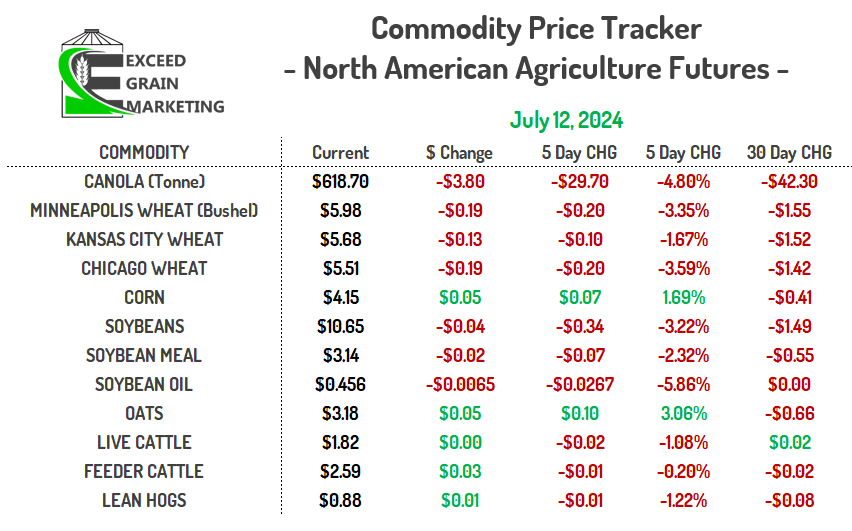

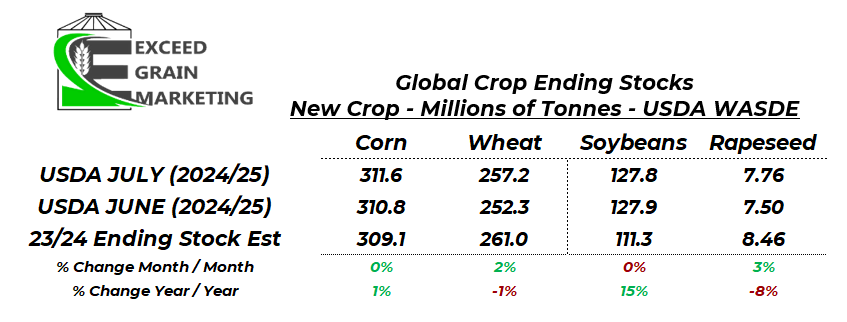

- USDA WASDE Report out Friday July 12th – Highlights:

- World Corn Ending Stocks Up slightly from Junes WASDE but close to estimates – 311.6 mmt vs 310.8 mmt last report

- World Soybean Ending Stocks Down slightly from last month and about 1mmt more than estimates heading into the report. 127.8 mmt vs 127.9 mmt June.

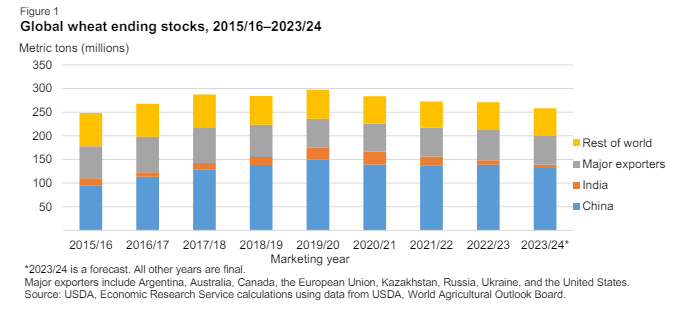

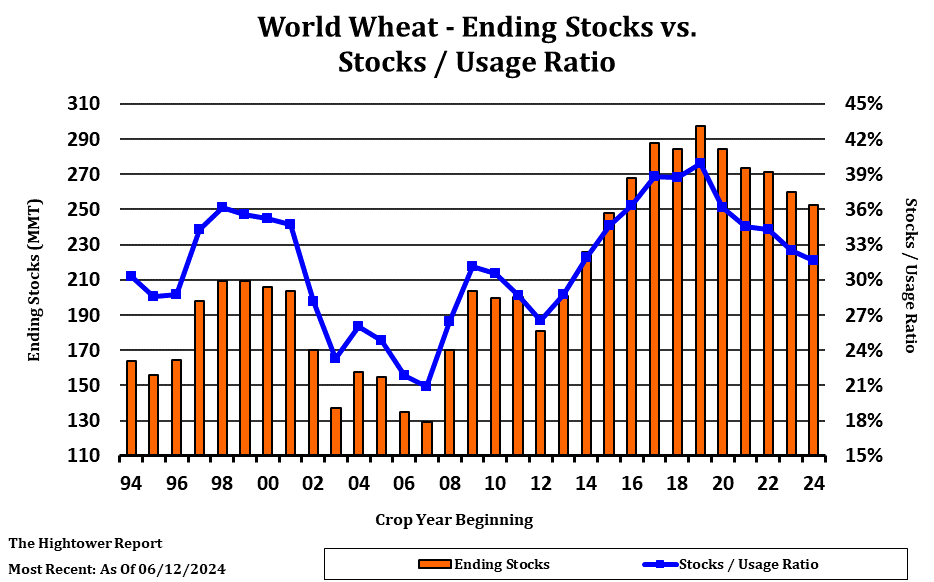

- World Wheat Ending Stocks up big time and was the “surprise” of the report. Junes USDA has wheat stocks as 252.3 mmt and estimates were around 252.1mmt. 257.2 mmt was the published number from the USDA for the July report

- Wheat traded lower immediately following the reports release and other grains were mixed. By the time the market close drew near, all grains were trading lower with the exception of Corn and Oats picking up a few pennies despite nothing really bullish for the corn market.

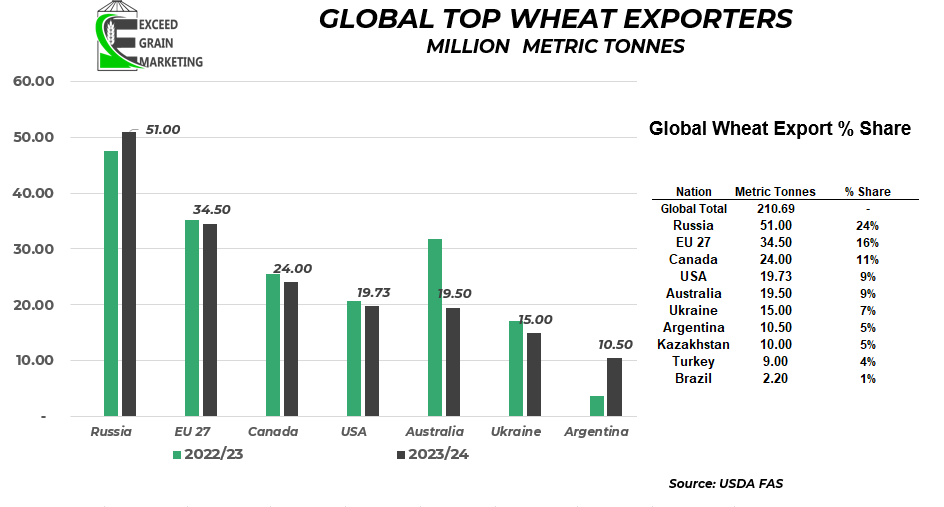

- USDA Left Ukraine and Russian wheat production untouched. 19.5 mmt and 83.0 mmt respectively.

- Big moves in the wheat side of the report was a 1mmt bump in Canadian wheat production to 35.0 mmt and US wheat production up a massive 3.5 mmt.

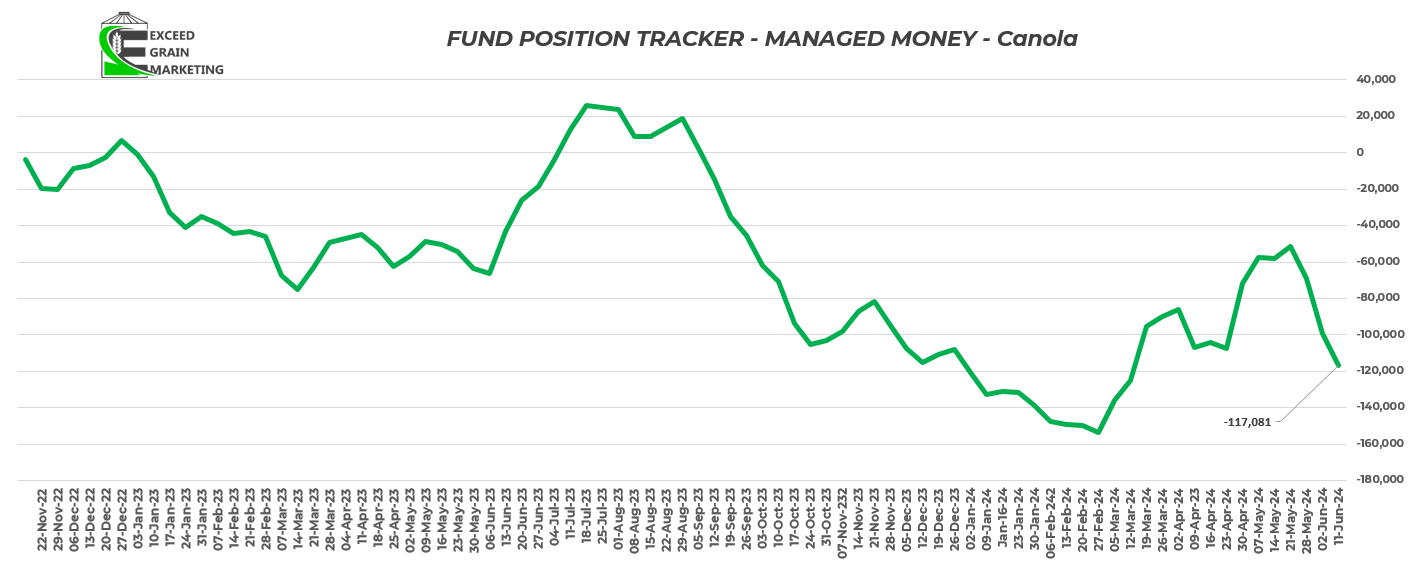

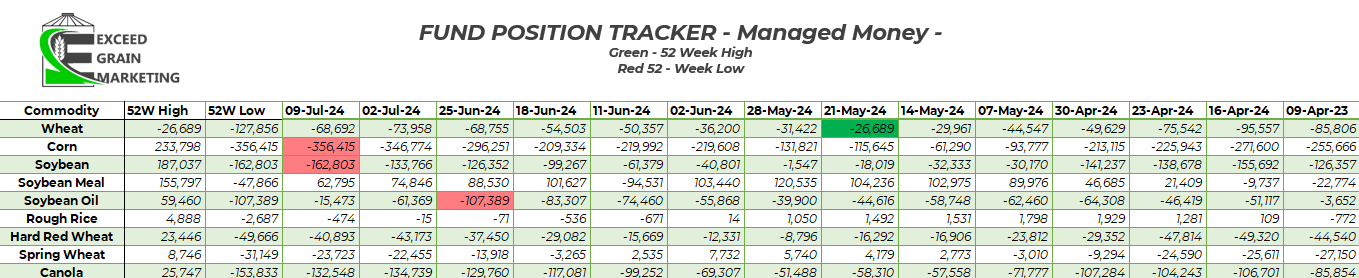

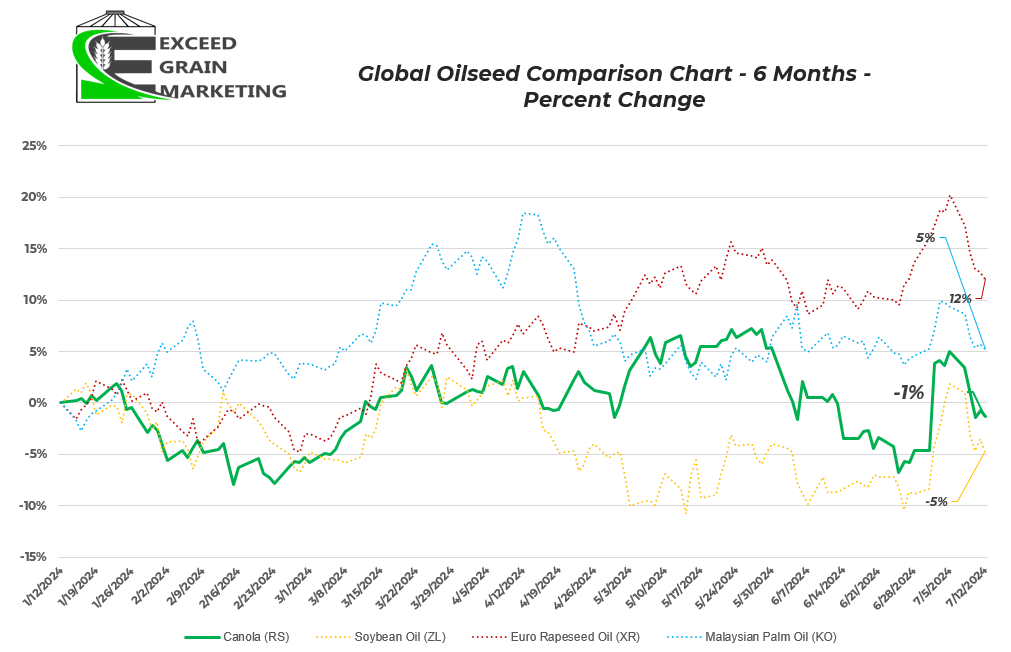

- Funds are massively short many markets, particularily Corn and Soybeans although, see chart below. Canola short positions not quite as low as February/March but would be record short for the time of year.

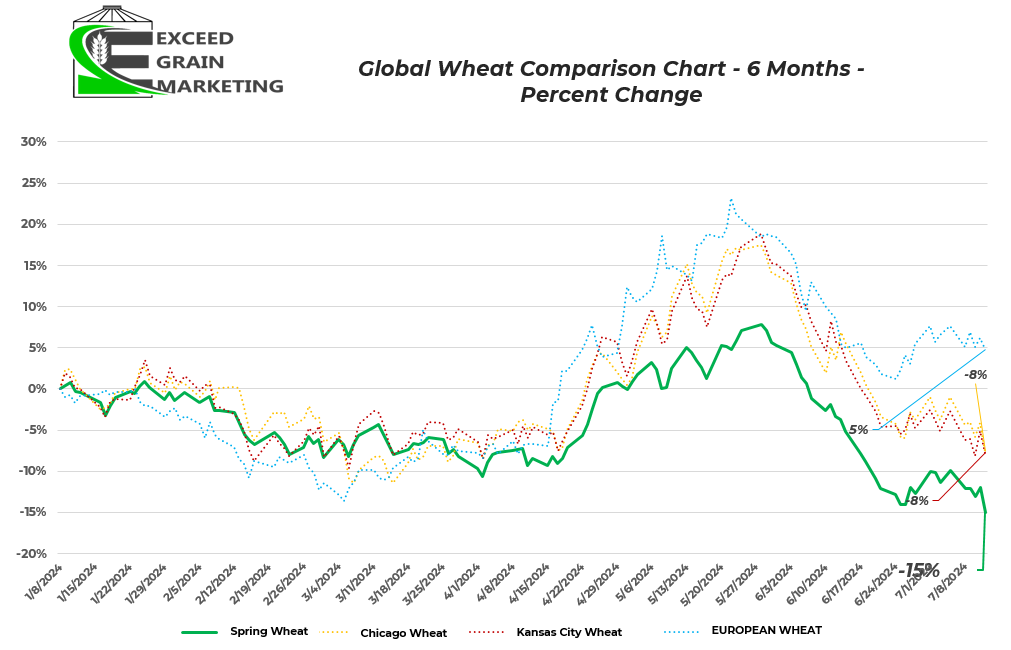

- Corn and Soybean futures prices sitting at 4 year lows. Wheat sitting in a simular spot but some of the contracts found lower values in recent months.

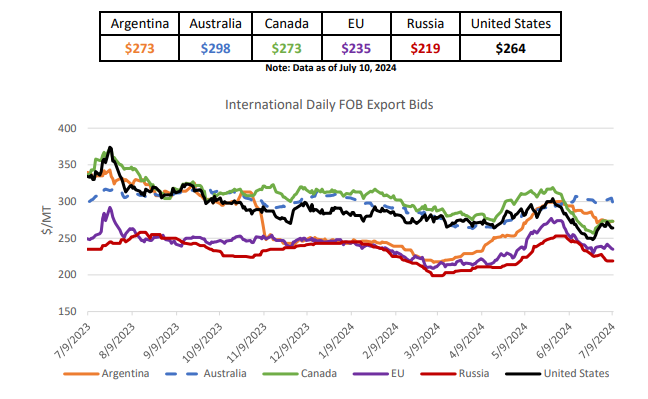

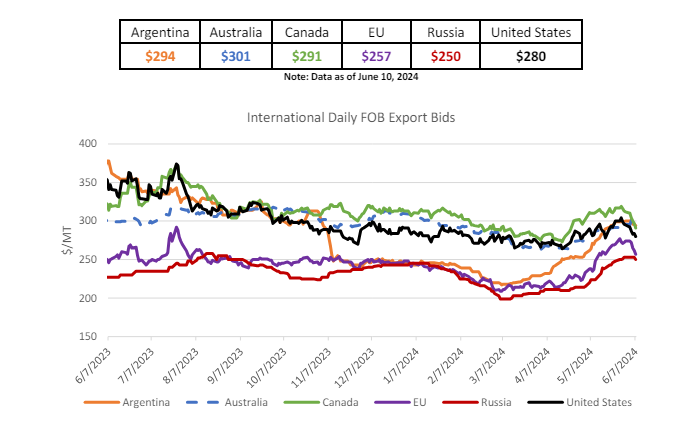

- Global wheat prices lower. Russian wheat $31 per tonne lower month over month.

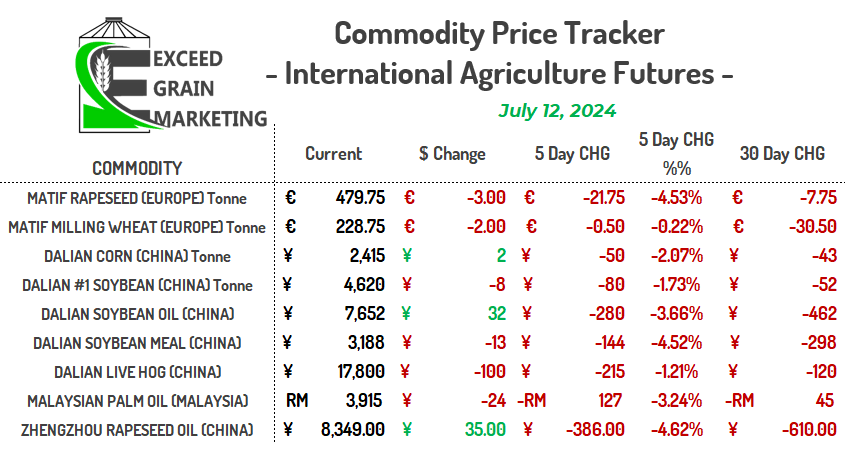

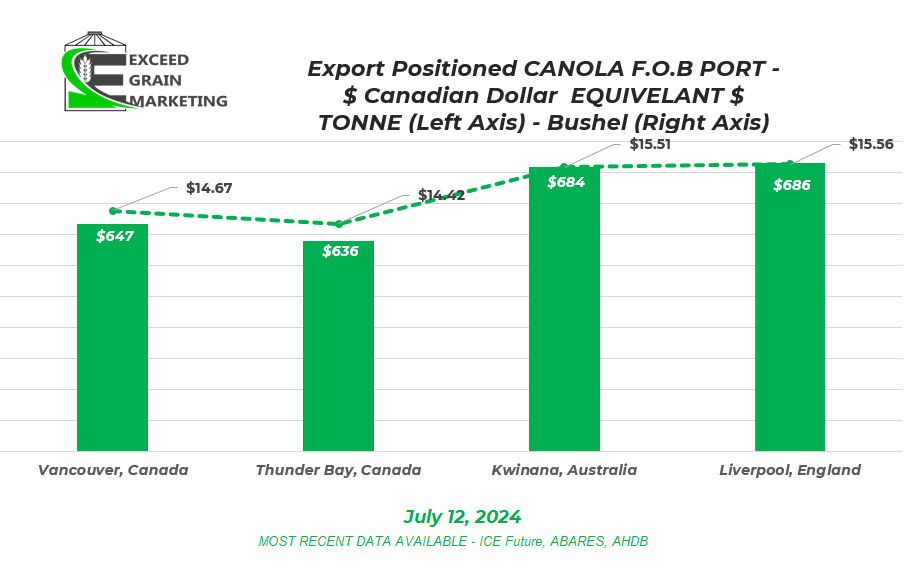

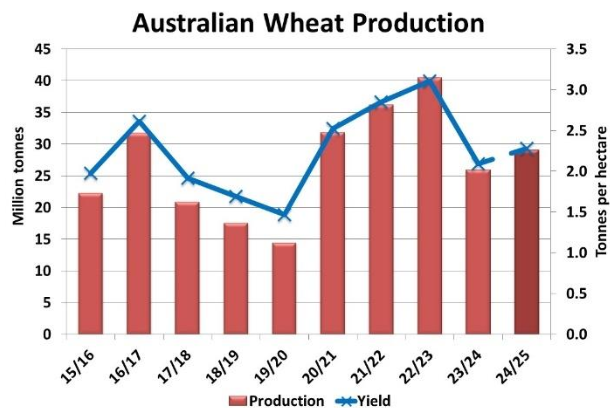

- Australian wheat pricing more expensive than Canadian wheat right now, same story for Australian canola. See charts below. Typically Canada has been carrying a premium to Australian canola in recent years and has caused Canada to lose out on some key sales this past year due to cheaper foreign supply.

- Market has a big crop prices in and it will be difficult to get a rally unless there is a demand story to be built or there is a sudden onset supply scare of some substance.

- US new crop demand is not great. First Soybean sale to China was booked this week for the 2024/25 crop year. About 4 months later than normal. Demand prospects need to improve before seeing stronger sentiment towards this crop.

- Harvest underway in Black Sea Wheat. Yield prospects still quite mixed but some private analysts are increasing Russian wheat estimates closer to the 84/85 mmt level, vs the 80/82 mmt estimates out a month ago. Still much to be said on this crop. Yields on the early crop were likely better than expected but now it sounds like yields are underperforming as they get further into the crop.

- Rumors floating that Russia may impose wheat export restrictions within the next month. This is nothing novel as Russia has done this plenty of times in the past but tends to be more prevalent if the crop is a shade on the smaller side and they want to keep domestic milling prices in check as well as get the most for their exported products.

- EU harvest underway. French wheat under 5% completed. French crop conditions the lowest in 4 years and the crop will likely be sub 30mmt vs the 35mmt crop last year and one of the smaller ones in recent years. Higher carry in stocks will be the gamechanger here although as wheat carry was quite substantial in France and should minimize the supply shortages.

- USDA and Stats Canada acreage reports below

- USDA Crop Acreage Report released June 28th 2024 – Highlights:

- Corn Acreage came in higher than expected. 91.5 million acres vs 90.34 pre report estimates

- Soybean Acreage came in lower than expected. 86.1 Million Acres vs 86.75 pre report estimates

- Wheat acreage came in slightly lower than expected 47.24 Million Acres vs 47.66 pre report estimates. Spring wheat was 11.3 million acres of this total and right near expectations.

- For Some Smaller, less covered crops by the news wires:

- Canola area came in at 2.663 million acres for US plantings vs 2.344 million acres last year.

- North Dakota is essentially where all the canola is grown. 2.05 million acres in North Dakota alone. Washington and Montana make up the rest of acreage.

- Flax Acres in at 140,000 all in Montana and North Dakota. 178,000 last year

- Pea acres up 1.03 million acres vs 966,000 last year

- Chickpea acres 502,000 acres vs 372,000 last year

- Lentil acres 836,000 vs 546,000 last year

- Other notes from the report: June Stocks

- June 1st stocks all came in above estimates but not far off from expectations. June 1st corn stocks at 4.99 billion bushels vs 4.10 last year. Soybean stocks 970 million bushels vs 796 million bushels last year. wheat at 702 million bushels vs 570 million bushels last year.

- Overall June 1st stocks look fairly heavy, but the market has been working with this notion all year in United States, so none of this comes as much of a surprise

- Statistics Canada Acreage Release on June 27th:

- Wheat: Saskatchewan Producers Reported no change in wheat acres year over year at 14.2 million acres. The decreases over year came from a drop of 1.6% drop in wheat acres in Alberta and a 1.4% drop in Manitoba. Spring wheat acres were down 2.77% year over year but still higher than the 5 year average

- Canola: Canola acres came in high end of pre report estimates and significantly higher than early planting intentions of 21.4 million acres. Canadian Producers reported a total planted acreage of 22 million acres, an extra 600,000 acres give or take. Despite this, canola managed to hold onto a gain for the remainder of the trading day following the report release.

- Durum: Durum acreage came in very close to estimates pre report, no major surprises here. Durum acreage came in at the highest since the year 2000. Durum acreage definitely on the higher side but as expected.

- Full coverage of the Statistics Canada report can be found by clicking here

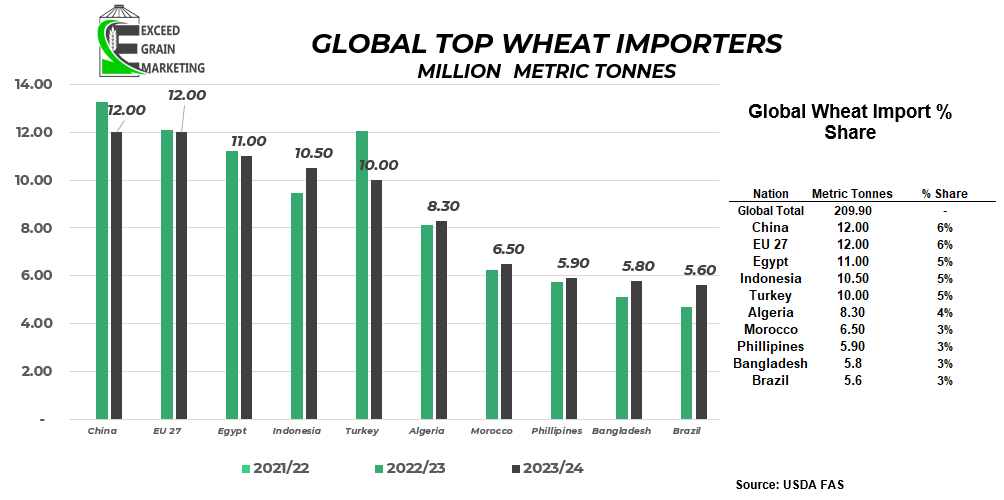

- Turkey banning wheat imports until October to help control domestic prices. Turkey is typically Russia’s largest wheat importer.

- European Union released their tariff guidelines in May for Russian and Belarussian grain imports. As of July 1st it is being reported that cereal crops (wheat, barley, ect) will be subject to a 95 euro per tonne tariff into the EU and oilseeds will be 50% tariff.

- Frost in parts of Germany and Poland late April / Early May has private analysts down to around 18mmt. Last year around 20mmt

- The narrative has already begun that EU will need to import around 6mmt of Rapeseed/Canola for the upcoming campaign. This past year Canada missed out on most EU business in favor of Ukraine and Australian origin of cheaper origin.

- North American producers will welcome India’s extension of the Yellow Pea tariff exemption. Yellow pea imports will remain exempt from import duties until October 31st, 2024. Moving the exemption into the new crop season. Domestic yellow pea bids have increased as a result.

- Desi chickpeas will now be exempt from tariffs until March 2025.

- Australia has turned to planting more Desi Chickpeas this year, especially in Western Australia. Acres up 80%

- Australia is expected to plant a record 885,000 acres of lentils

WESTERN CANADIAN CROP NOTES

Canola:

- Canada will be working hard to pick up some of the shortfall in the European crop, much of this business we lost out on last year to Australian canola due to us being overpriced in to our secondary markets. EU needs to import around 6mmt of Canola this year partly due to the shortfall in their own crop. EU rapeseed crop 1.1 mmt smaller than last year

- USDA moved Canadian canola production to 20 mmt. One of the largest crops in recent years according to the government agency. Global canola production down about 1mmt from last year.

- Canola has moved seasonally lower in recent weeks, but found a short term bounce the start of July. In general Markets appear satisfied with the state of the current Western Canadian crop despite some heavy rains in particular areas such as Northeastern Saskatchewan and Western and central Manitoba. Although much of the prairies moisture is “adequate” it is unjust to paint the region with a broad brush. Manitoba has many areas that are very wet and some flooded acres, while central Alberta has growing pockets that need to catch a rain here soon.

- We hit some important sales targets for our grain marketing clients Mid May and again in early July due to the run up in futures from the February lows. See recommendation section below. We recently made a rec to shape up some of the old crop sales as well for producers. See details in the rec page below.

- Canola global pricing below. Canadian Canola moved cheaper than Australian FOB.

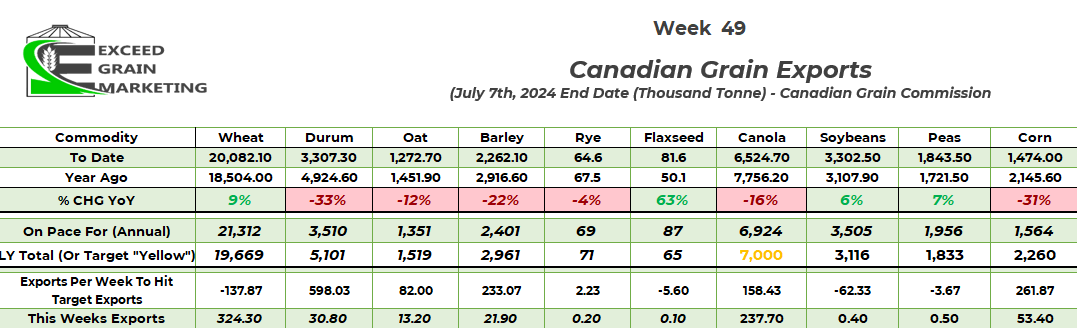

- Canola export current pace of 6.9+ mmt is not great overall and would be one of the lowest levels of exports in decades. See chart below for reference. We have moved closer to that 7.0 mmt mark in recent weeks as some strong exports on the tail end of the marketing year so far. Only 3 more weeks left of export reporting for the crop marketing year. Important to note the massive legwork on the export side in recent weeks although as mid winter we were on pace for a 6.0mmt crop export pace

- Crush is running at a very impressive pace, looks like we will surpass and hit a 11mmt + record.

- Crushers hold the winning bid for new crop 2024 harvest

- For a more in depth analysis on Canola Specifically, check out our June 2024 Canola Fundamental report by clicking here: Canadian Canola Market Fundamentals – June 2024

Wheat:

- Wheat markets focused on the ongoing US Winter Wheat crop harvest which is progressing well and looks like it will come in as expected. No major surprises as of yet.

- For the Majority of May, Russia / Black Sea weather was the driver of wheat markets. Some significant frosts in Russia in first half of May causing some havoc with crop conditions. Now dryness in the same regions have been drying and lack of rainfall during some critical crop growth periods. The wheat crop harvest has begun and initial yields are mixed. Some of the very first early yields were higher than expected but now trending lower as harvesters get into the later crops.

- USDA July placed the Russian wheat crop at 83mmt, unchanged from the June report. Ukraine 19.5mmt, down from 23 mmt last year.

- USDA July put Canadian wheat up by 1mmt to 35mmt and US wheat up around 3.5 mmt to just shy of 54.7 mmt

- Private analysts calling the crop anywhere from 79 to 85 mmt. Was closer to 93mmt earlier in the year. The USDA posted 91.5 mmt last years crop, the year prior was argued to have been higher and closer to that 100 mmt mark unofficially. So important context when looking to compare crop sizes.

- Indian stockpiles of wheat lowest in 16 years. This week the nation stated that they will not remove import tariffs and will look to bridge the gap in other ways. It was widely speculated up until a few days ago that India would enact certain measures to entice more wheat into the country. India signaling to the market that it will not enact any special measures to shore up stockpiles.

- US winter wheat crop coming off good without much delay. Looks like a slightly better than expected crop. Harvest pressure.

- Russia’s ministry of agriculture reporting that 830,000 hectares or over 2 million acres of crop were lost due to the multiple frost events of the first half of May. Privates saying at least double this. Russia called a state of emergency in many states to help producers have easier access to funding.

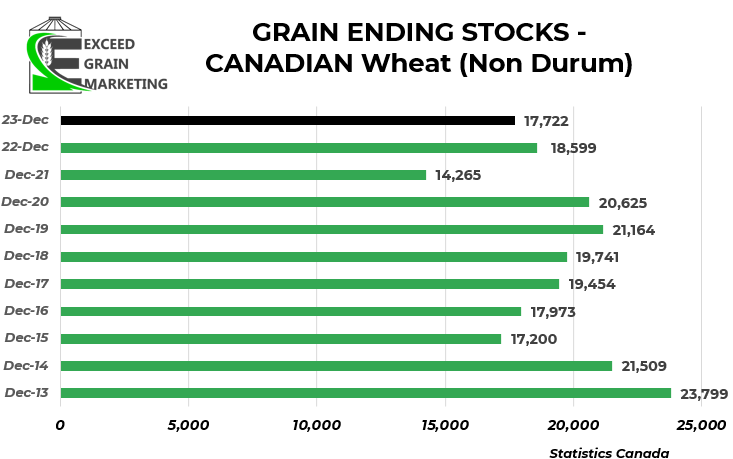

- Forecasted wheat global and domestic ending stocks coming in at the tightest levels since the 2015/16 crop year.

Special Crops

- More Durum acres in Canada and United States but we know some issues with the Durum crop overseas. Lots of the global durum pricing waiting to see how Canadian crop plays out. Durum prices down from early spring on anticipation of a good North American crop.

- Yellow Pea and Lentil Acreage expected to grow in Canada for the marketing year. The pulse crops acreages were higher spring 2024 due to some profitable selling opportunities. Pulses still some of the more profitable crops out there, bids have slid from spring due to good farmer selling but remain profitable

- Canadian peas will face stiffer competition going forwards into China as some Black Sea peas able to price into the region. Some of these peas were affected by early May frosts.

- India reduced Yellow Pea import tariffs from 50% down to 0% was extended for several months and now sits at October 31st, 2024. Was only in place until end of March but another month, and then another, was added to get exports into the nation. No word yet on if this tariff exemption will be kept in place, a consideration to be made when marketing this years crop.

- Red Lentil reduced import tariffs into India extended until March of 2025

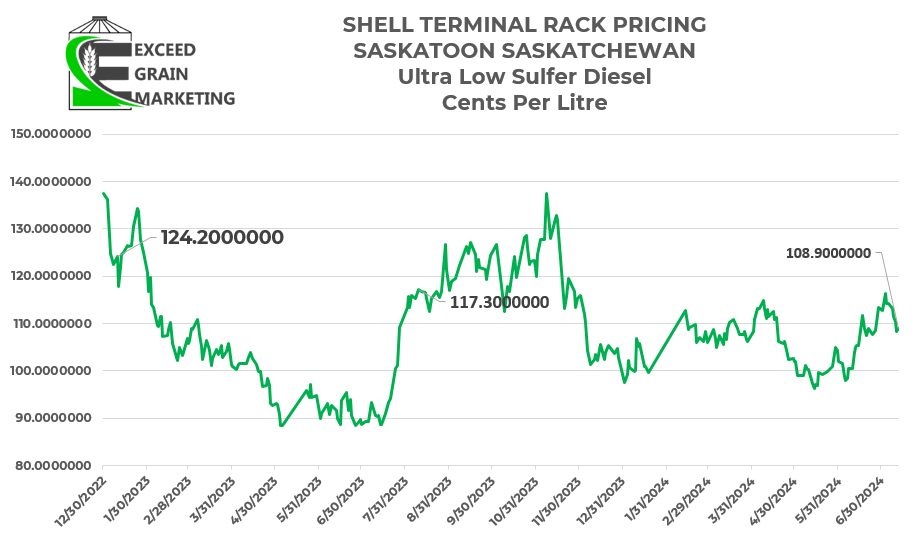

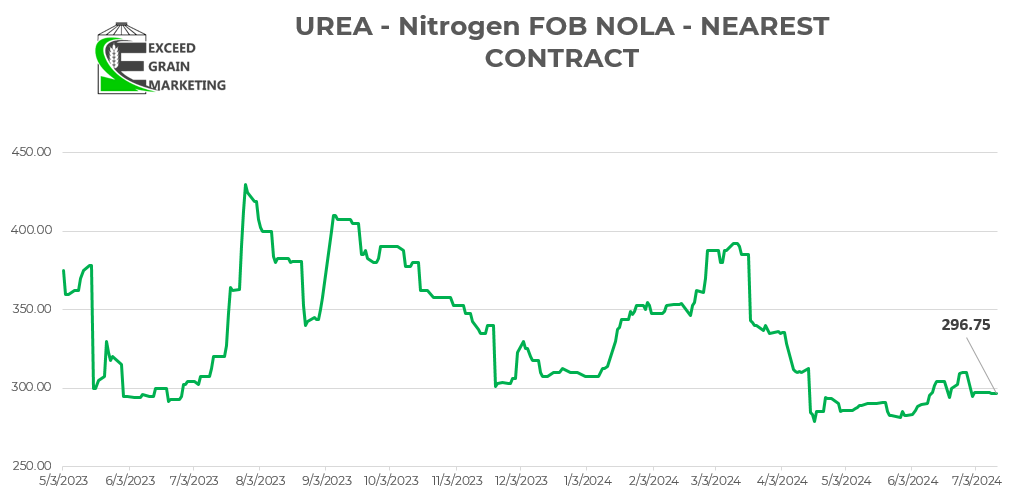

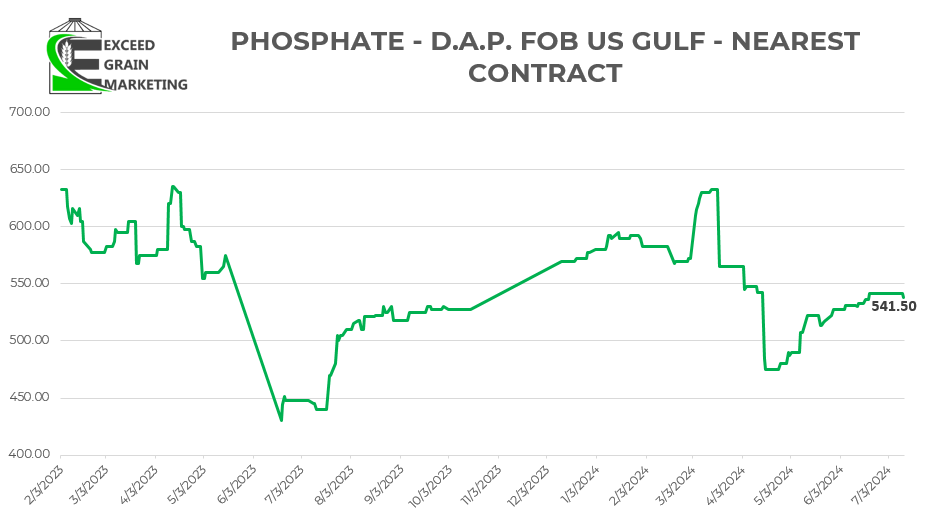

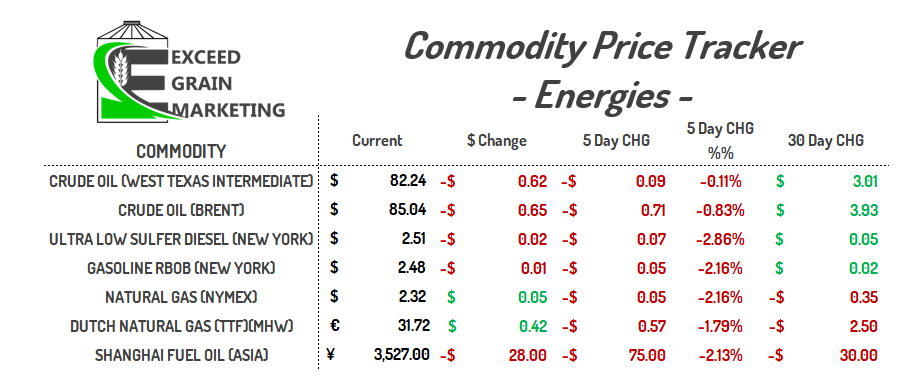

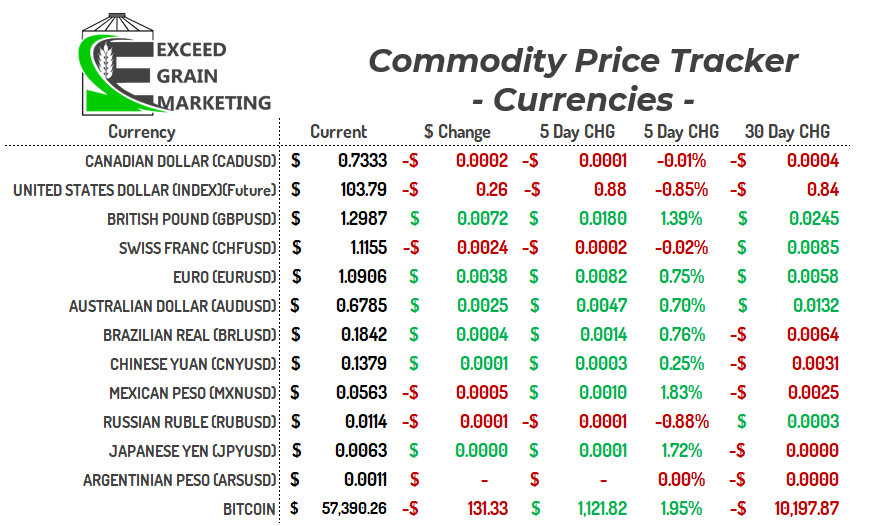

Currency – Energies – Fertilizer

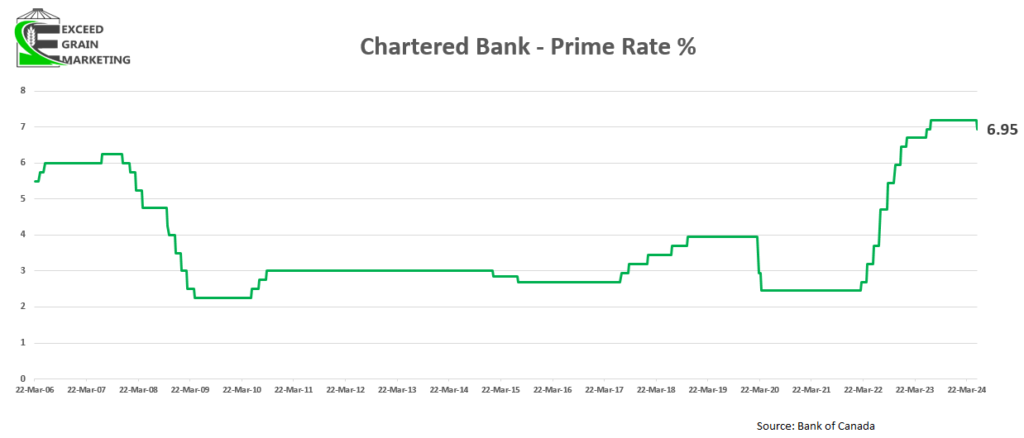

- Prime sits around 6.95% at major Canadian banks.