Exceed Grain Marketing’s Client Exclusive report is dedicated to covering the ongoing trends and significant highlights within the local market, while simultaneously offering a perspective on the global landscape. This approach ensures a comprehensive understanding of the factors influencing the market at both local and international levels. Our aim is to deliver current, up-to-date information specifically tailored to the crops impacting your operation. Work with your Exceed Grain Marketing advisor to devise specific strategies that may work for your crop.

MARKET HIGHLIGHTS

- Grains finished off Fridays session with some good strength into the close even in the last few minutes of the trade.

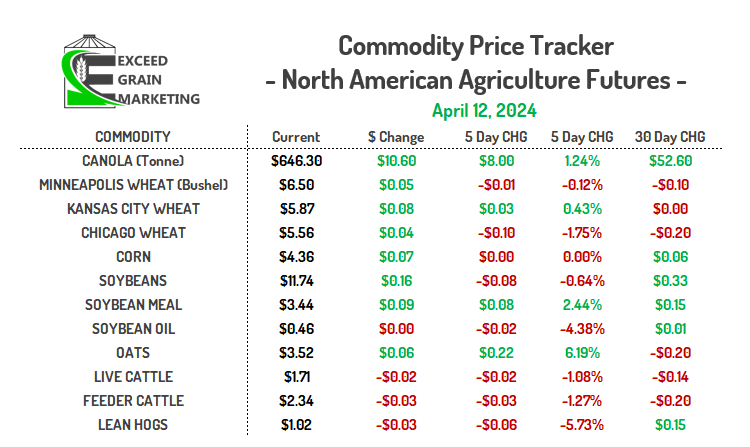

- Canola closed the trading day up $10.60 for the trade day, almost regaining yesterdays losses. Up $8.00 per tonne for the week. Canola took back its independence from soybean oil today after following it lower yesterday. EU rapeseed had an incredibly good day today as well, giving canola the confidence boost it needed to close out higher on Friday.

- Soybean oil was the lone soldier lower in the North American markets trading lower.

- Solid Days in all other North American grains, Corn, Beans, Wheat all make some recovery from yesterdays post WASDE hangover.

- We are entering an exciting time in global grain production.

- Brazil soybean harvest is almost completed around 80% complete, corn crop getting into some important growing stages of its life cycle. Precipitation being closely watched for corn here and this remains a weather market for the second crop corn.

- Argentinian soybean crop harvest just started, less than 5% complete.

- North American crops beginning to go in. Corn planting underway in southern regions and just beginning in key states such as Illinois (2% complete). Expect some significant progress in coming weeks. Some rains are forecasted for most drought struck corn and bean regions.

- Canadian planting taking place in the prairies and down into Montana/North Dakota. Very early yet.

- EU crops are out of dormancy and we will be watching the weather there closely.

- Australian crops going in for Canola and Spring Wheat, Barley, Pulses. Seeding is underway in many areas. Western Australia is a mixed bag for weather. Some drought and some areas of ample moisture.

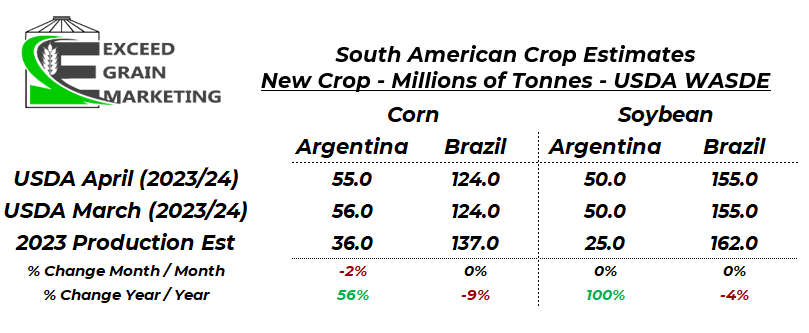

- CONAB yesterday put Brazilian soybeans at 146.5 mmt corn at nearly 111 mmt, big divergence from the USDA’s figures as you can see in tables below, market not putting much weight into this spread although.

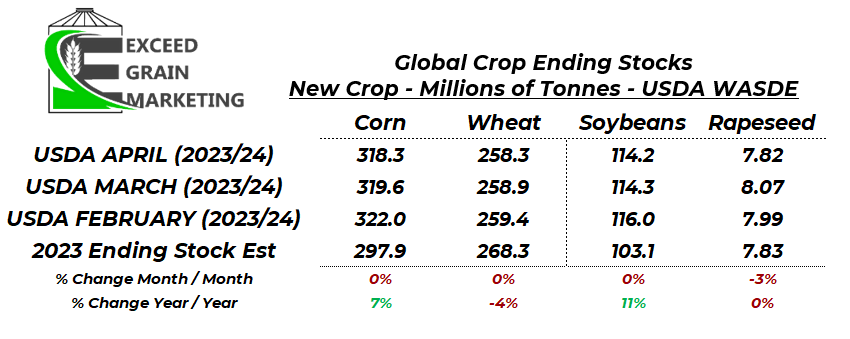

- USDA WASDE April 10th Highlights:

- Tables of the Trade Below

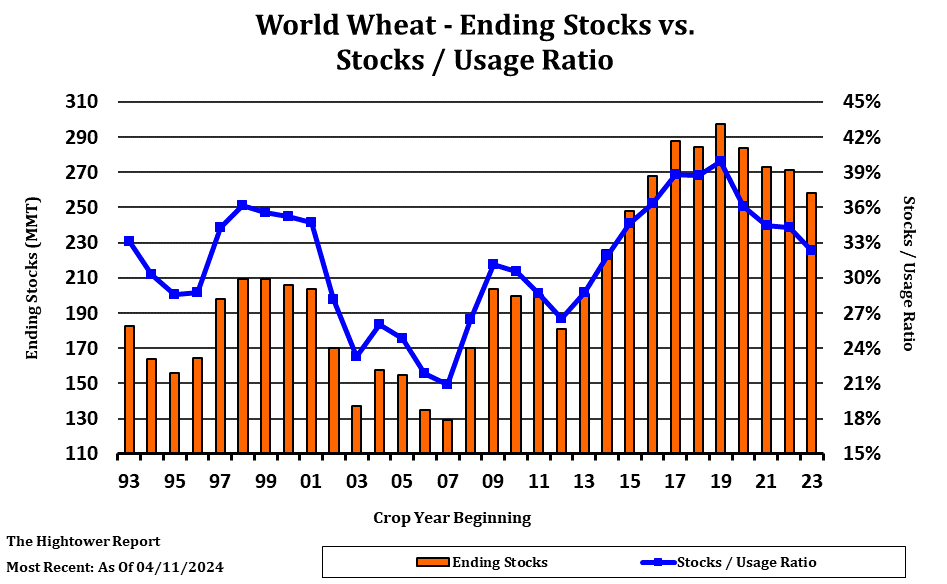

- Global Wheat ending stocks at 258.3MMT vs 258.8 last months and 259.1 pre report estimate

- Global Corn ending stocks at 318.3 mmt vs 319.6 mmt last month and 316.7 mmt pre report estimate

- Global Soybean ending stocks of 114.22 vs 114.27 last month and 113.7 pre report estimate.

- Soybean oil at 5.16 vs 5.01 last month

- Rapeseed/Canola ending stocks of 7.82 mmt vs 8.07 mmt month prior.

- Next month for the May WASDE we get new crop estimates.

- Strategie Grains, French Private Analysts place EU barley up 10% year over year. Rapeseed production at 18.1 mmt vs 18.3 month prior, 19.9 mmt was the production number last year.

- French wheat conditions reported to be at 64% good to excellent, lowest level since 2020.

- China reported to have cancelled up to 5 panamax ships of Ukrainian corn this week, amidst lower prices for Chinese domestic corn prices.

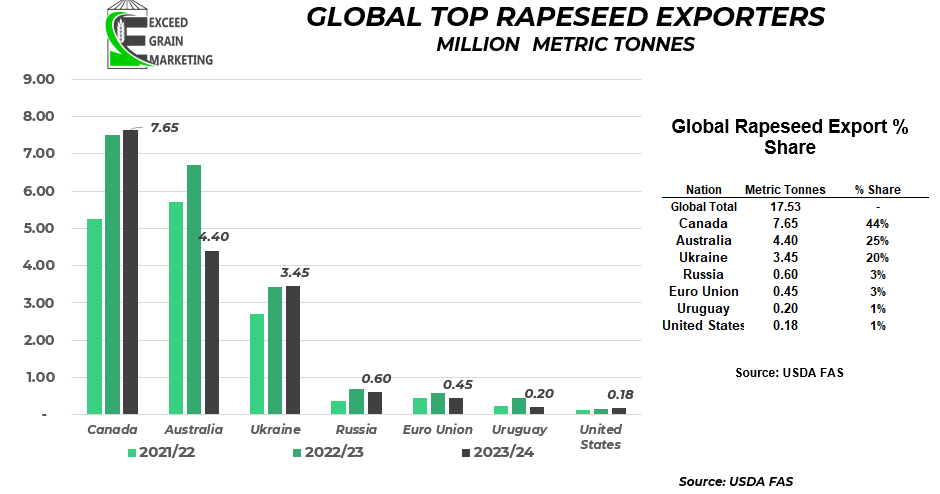

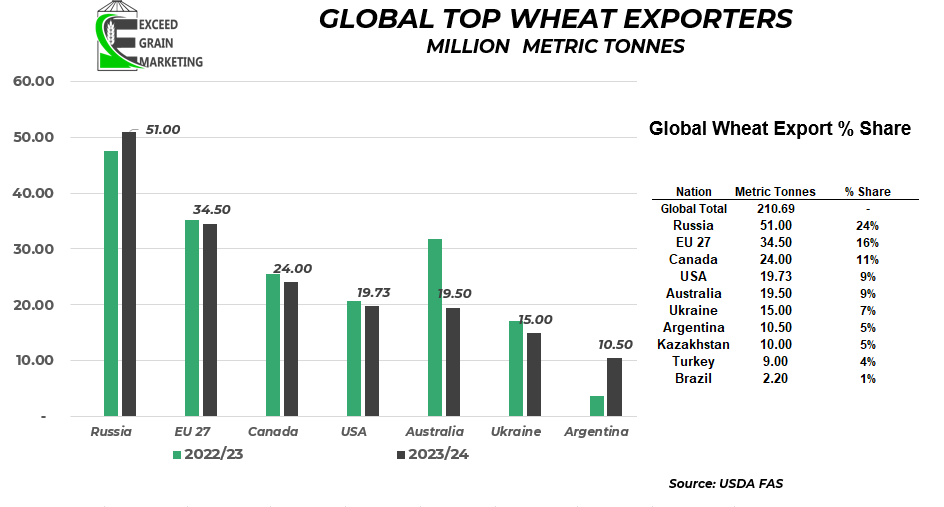

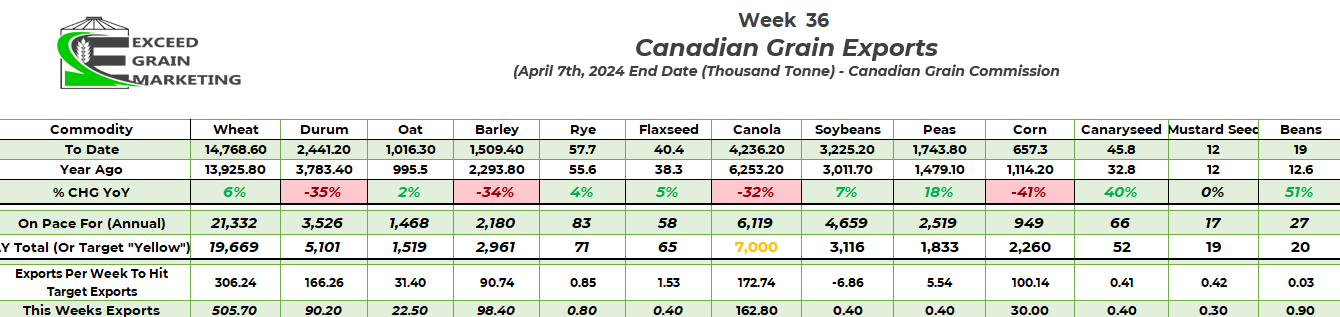

- New Weekly export figures were released on Thursday. We shipped 162,000 tonnes of canola in the first week of April, enough to maintain our pace of 6.1 mmt of movement. Heading into the marketing year, analysts were looking to move upwards of 8mmt, which almost can not be done at this point in the marketing year. Exports need to keep strength throughout the tail end of the marketing year to meet current reduced export estimates. Wheat exports currently still firing away at an incredible pace. We exported 505,000 tonnes this past week and are on pace for a record pace of 21.3 mmt. Current pace is 6% higher than last year. We will run into two different scenarios with wheat, we will ration out supplies because this pace likely cant keep up due to supply in the Canadian market, or supplies are much higher than industry estimates elude to.

- Pea export pace up 18% year over year, due mostly to reduction in Indian tariffs.

- Canola crush pace still on for 11mmt or more, which would be a record crush. Lower than expected exports of Canola early on in the marketing year has hurt the most. Private analysts looking roughly at a 2.5mmt carryout. Not a massive carryout, but also a carryout that does not get end users shaking in their boots.

- More below in the Canola section, but be cognizant of crush capacity filling up in front months and how your plan works around that.

- Advance Payment Program payments are now available to Canadian farmers for the 2024 program year. Starting April 1st the advance is available to producers. Often referred to as the CCGA cash advance. The program provides up to a $1 million cash advance with a $250,000 interest free bearing portion.

- European Union proposed new tariffs on Russian grain: 95 Euro per tonne for grains. 50% for other crops. Subject to approval by the 27 member organization. If you are a Flax producer, keep an eye on this.

- Recommendations Page Updated at Bottom of Report

Prior Report Section

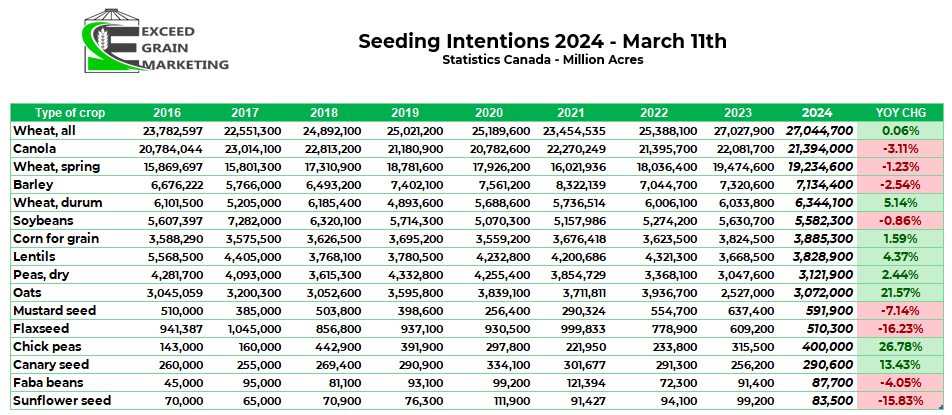

- Statistics Canada Acreage Estimates Analysis (March 11th).

- Canola acres down year over year, Spring wheat and Barley were down as well.

- Chickpeas showing the largest percentage gain year over year and Flaxseed the largest drop.

- Oat acreage came in on the low side of pre report estimates despite a large year over year spike in acres. Oats still running some relatively low acreage numbers compared to years past. Take a look at chart below to see the past few years of acreage

- Canola came in near the bottom end of pre report estimates, but more in line with some longer term averages for acres.

- Stats Canada conducted the survey from December 14th – January 22nd and surveyed 9,600 farms. There have been significant changes in New Crop markets since this time and one can expect that final planted acreage will shake out a tad different than what was reported.

- Prospective Planting Acreage (March 28th, 2024)

-Corn 90.04 million acres vs 94.6 million last year and 91-92 million acres expected pre report

-Soybeans 86.5 million acres vs 83.6 million last year and 86.5 to 87.5 pre report

-Wheat 47.5 million acres vs 49.6 million last year and 47-47.3 pre report

Of the wheat acres 11.3 million are destined to be spring wheat vs 11.2 last year

Corn was the surprise in todays report with limited estimates reaching as low as a 90.04 million acre corn number.

Quarterly stocks report was also released today. Stocks came in fairly close to estimates with some divergence. Corn lower and beans and wheat stocks higher The most notable takeaway from the stocks report is the growth from last years stocks at the same time.

Quarterly Stocks Report:

-Corn 8.35 billion bushels vs 7.4 billion bushels

-Soybean 1.85 billion bushel vs 1.69 billion bushels

-Wheat 1.09 billion bushels vs 0.94 billion bushels - March CONAB Brazil:

- CONAB lowered soybean production estimates from 149.4 to 146.9 mmt. The corn estimate was lowered from 113.7 to 112.8 mmt.

WESTERN CANADIAN CROP NOTES

Canola:

- We hit some important sales targets for our grain marketing clients in past few weeks due to the recent run up in futures from the February lows. See recommendation section below. May Canola has touched the $640 level multiple times here in recent weeks.

- Crushers filling up domestically for the front months as producer selling took up much of the front month capacity. Most crushers bidding June onwards. If need crusher movement, need to build a plan around that. June/July/August is where most capacity lies within the crush. Be cognizant of export and crush capacity as we get closer to the dates.

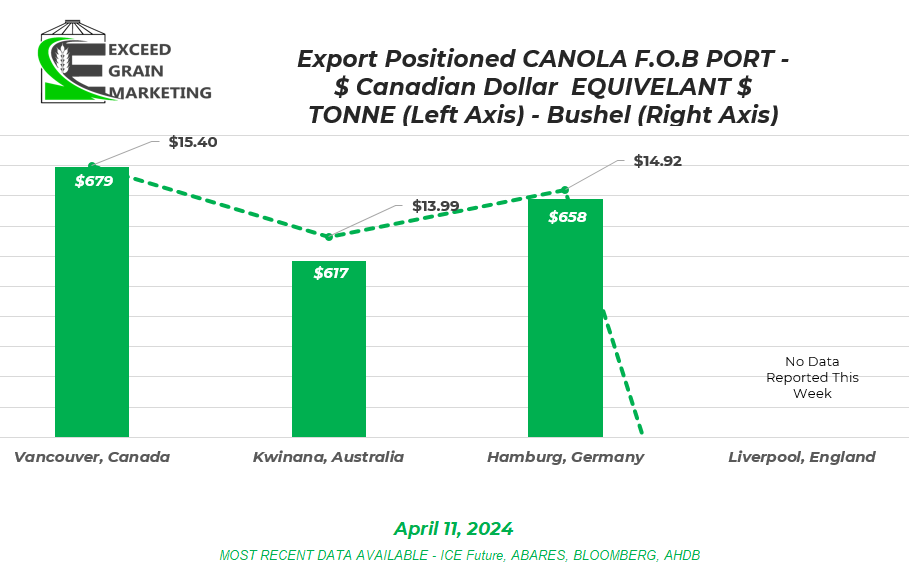

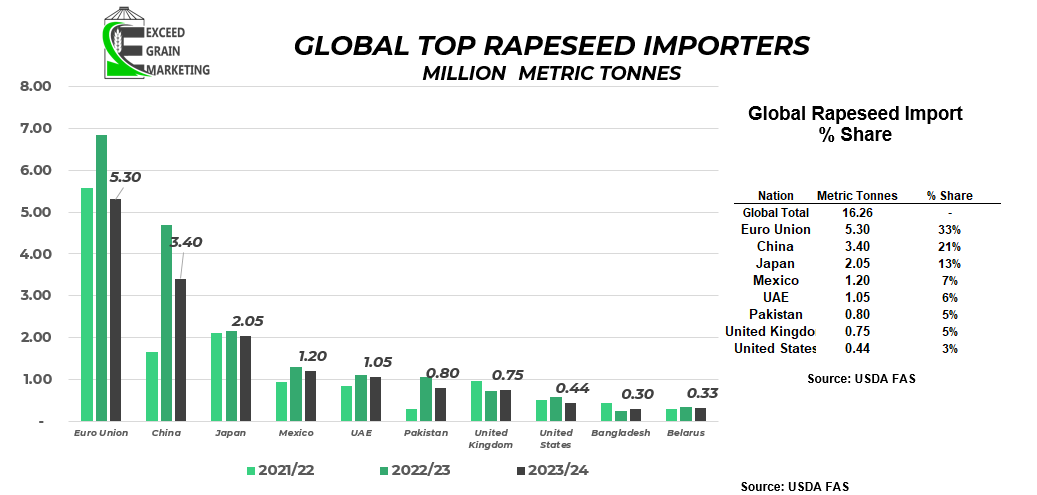

- Canola now once again pricing more expensive than Australian Canola after being cheaper than them in late February and into early March. The difference between exporter bids has narrowed up significantly in recent weeks. Canola carried such a premium to Australian canola and EU canola through the first half of the marketing year. It narrowed up significantly for several week but is showing signs of building that spread again. Chart above shows most recent bids at some key export regions in Canada, Germany, Australia and England.

- Canola exports bouncing around. Good week 36 with 162,000 tonnes leaving Canada, but Week 35 numbers were dismal with what looks to be one ship leaving shorelines, the week prior, almost 250,000 tonnes was moved.

- Current export pace of 6.0+ mmt is not great overall and would be one of the lowest levels of exports in decades. See chart below for reference

- We need to grab exports on the tail end of the marketing year to maintain a reasonable carryout in the market. We have 16 weeks of export left in this marketing year. Need consistent movement here on forwards

- Crush is running at a very impressive pace, looks like we will surpass and hit a 11mmt + record. Markets need to see exports pick up to get any sort of strength into the domestic trade (Basis).

- Canola will trade at the mercy of foreign veg oils for the time being (Palm, Soy, Rapa).

- Crusher bids still dominate but are falling closer to exporter prices, depending on the month. Most exporters sit close to the $14.00+ mark today, depending on region and Basis levels. Crushers still hold the leading bids, but the regions are getting fewer and further between and months are getting tighter.

- For a more in depth analysis on Canola Specifically, check out our April 2024 Canola Fundamental report by clicking here: Canadian Canola Market Fundamentals – April 2024

Spring Wheat:

- Russia has been playing games with exporters here since start of April, revoking some export licenses of key exporters and then reinstating them within a few days. Analysts believe the government mostly using this as a way to control exporters and let them know that they still rule the roost if unwilling to comply with government requests.

- Anecdotal reports of Russian farmer selling slowing down due here recently. New crop will be off beginning in July and the anecdotal sentiment is towards producers willing to sit on inventories for the time being.

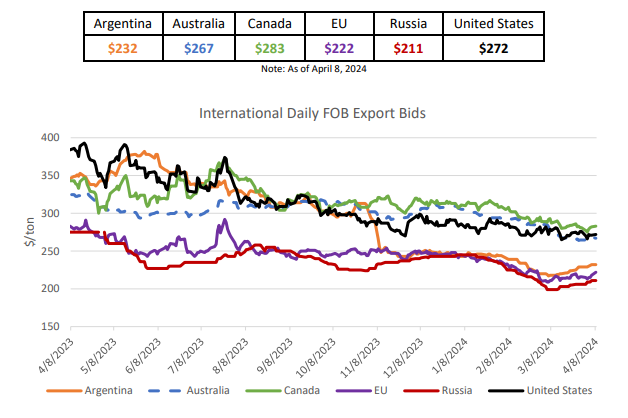

- Russia wheat values sitting in the $200 to $220 FOB Russia per tonne level on some recent tenders. Some reports of Russian wheat trading for as low as $200 per tonne in recent weeks for low protein wheat 11.5%. Prices appear to have firmed slightly and remain cheap, but stable.

- Domestic wheat bids in Western Canada touching that $8.50 range for old crop. $7.50 for new crop.

- Looks like Black Sea regions willing to dump grain here before summer. New crop will be in the system starting July 2024 so exporters looking to keep product moving.

- Canadian Wheat exports and domestic usage is still considered very strong. At the current pace of exports and domestic usage, rationing will be needed. This does not always mean price correlates accordingly, as we have seen in recent weeks. Prices have seen producers selling into them.

- Wheat exports expected to easily surpass last years levels at current pace and are on track for an 8% increase year over year. Likely not able to make that happen although as rationing will supersede this.

- 2023 Old Crop Canadian wheat of good quality. 97% graded as either a #1 or #2 HRSW

- 80% had falling number above 350 seconds

- Wheat trade right now is mostly demand based. We have a good idea on global supplies for the most part.

- Forecasted wheat global and domestic ending stocks coming in at the tightest levels since the 2015/16 crop year.

- Next thing market will be watching for is crop progress in the US and EU winter wheat crops and Spring Wheat planting conditions.

Special Crops

- Tunisia tendered for old crop Durum last week. Looks like Viterra picked up some of the business. $30USD per tonne cheaper than a similar tender about 2 months ago.

- Yellow Pea and Lentil Acreage expected to grow in Canada for the marketing year. The pulse crops are showing some excellent return potential for the 2024 cropping season if producers can bring it to yield at harvest.

- Special crop markets closely watched Marchs release on acreage estimates from Stats Canada.

- Barley acreage drops to 7.1 million acres. Fits in line with some trendline averages

- Barley prices lower than last year, as with many crops. Some $5.00+ feed opportunities available central Sask. Greater as you move closer to Feed centers. Add $1.25 to $1.50 for Malting.

- Durum acres up 5% year over year. One of the largest acreage estimates in recent years

- Lentil and Pea acres up year over year but still not out of line with recent history.

- One thing to note from this report is that it was collected from December to January 15th. Lots has changed in this timeframe.

- Canadian peas will face stiffer competition going forwards into China as some Black Sea peas able to price into the region.

- Canadian red lentils also competing with a larger Australian crop. Indian lentil harvest taking place here in the coming weeks and crop is expected to be of a healthy size. Looks like higher availability for global export market

- India reduced Yellow Pea import tariffs from 50% down to 0% was extended for another month until the end of June 2024. Was only in place until end of March but another month, and then another, was added to get exports into the nation. Pea bids did show some strength about two weeks ago but have toned back in recent days as the exporters square up their positions ahead of key deadlines

- Durum exports lagging behind last years pace. Durum exports have somewhat disappointed traders as we missed some key export opportunities early on due to some better than expected Mediterranean/Turkish crops. New crop Durum bids have fell from earlier on. $10.00 was attainable but now sits closer to $9.00. Local variances.

- Durum growing regions of Canada have got some recent precipitation but will be dependent upon some key rains following planting, producers somewhat hesitant to price aggressively on new crop. Some precipitation has came through end of March and into April, producers hesitant to price as bids have fell from earlier on as well.

- Red Lentil reduced import tariffs extended until March of 2025

- Red Lentil new crop sitting around $0.32 and $0.52 for greens. Act of God coverage bids slightly lower

- Yellow Peas – Old crop yellows $12+ on the renewal of the India tariff exemption. Bids are not consistent amongst buyers. New crop $10.00 and upwards of $10.50 range. We will need to see further tariff exemptions to keep premium in the market. **UPDATE: Tariff Exemption extended until end of June 2024**

- Flax Bids in the $16.00 range central prairies. Some large divergence in bids so please look into where you are pricing. Flax bids have been picking up here recently. Speculation of a sale through the seaway made for spring and concern about Kazakh supplies and whether new EU tariffs against Russian grains will affect supplies.

- Feed Barley has picked up some ground, gaining some traction. $5.25+ bids are commonplace . Still competing heavily with US corn origination. New crop feed barley $5.00 in some cases. Big Spreads depending upon buyers.

- Feed Barley at the mercy of US corn crop prices and Currency.

Latest Key Fundamental Report Highlights

- STATS CANADA ( DECEMBER)

- March 11th we got Principal Field Cropping Areas – See above

- December 5th production estimates. Stats Canada report came in and was mostly as expected but higher than the prior report released pre harvest.

- Canola- 18.3 mmt vs 18.3 mmt pre report estimate

- Spring Wheat – 24.7 mmt vs 24.0 mmt pre report estimate

- Barley 8.9 mmt vs 8.6 mmt pre report

- Oats 2.6 mmt vs 2.6 mmt pre report

- Durum 4.0 mmt vs 4.1 mmt pre report

- Corn 15.1 mmt vs 15.0 mmt pre report

- Soybeans 6.98 mmt

- Lentils 1.7 mmt vs 1.7 mmt pre report

- Peas 2.6 mmt vs 2.6 pre report

- Flax 0.272 vs 0.290 pre report

- Most of the production numbers are higher than they were in the early days of harvest when ideas for the canola crop were floating around a high 17’s number. Same could be said for Durum and a few other select crops.

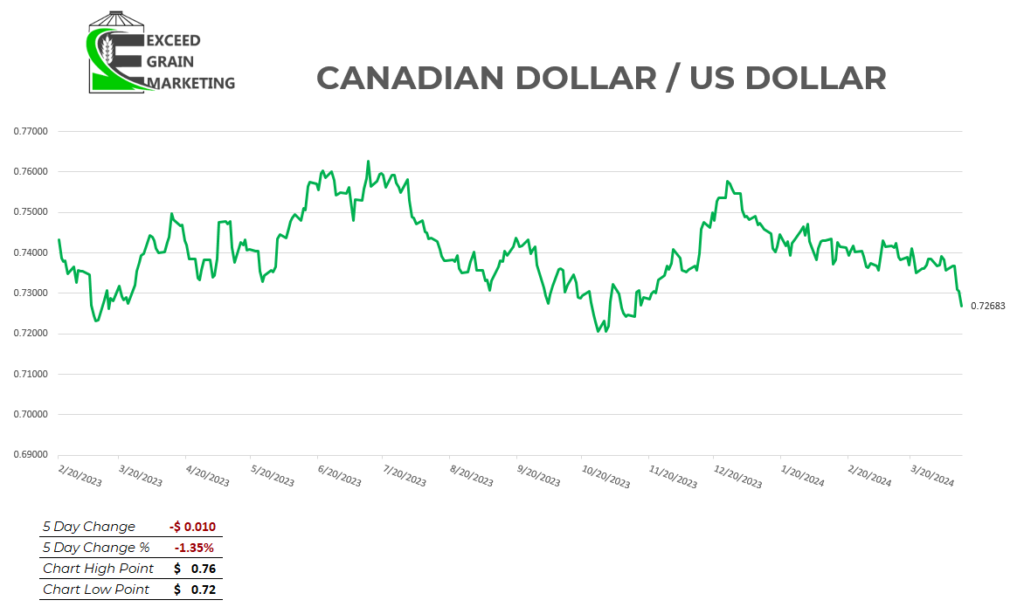

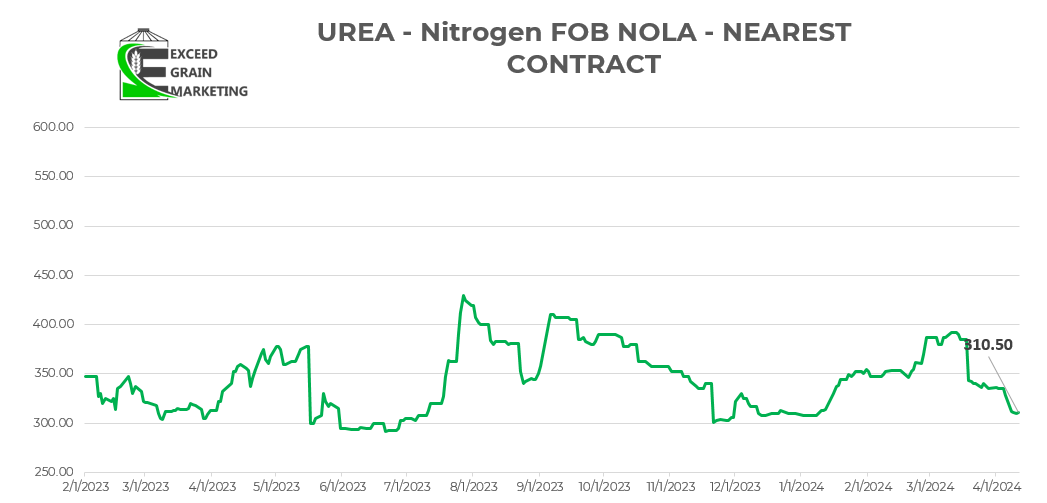

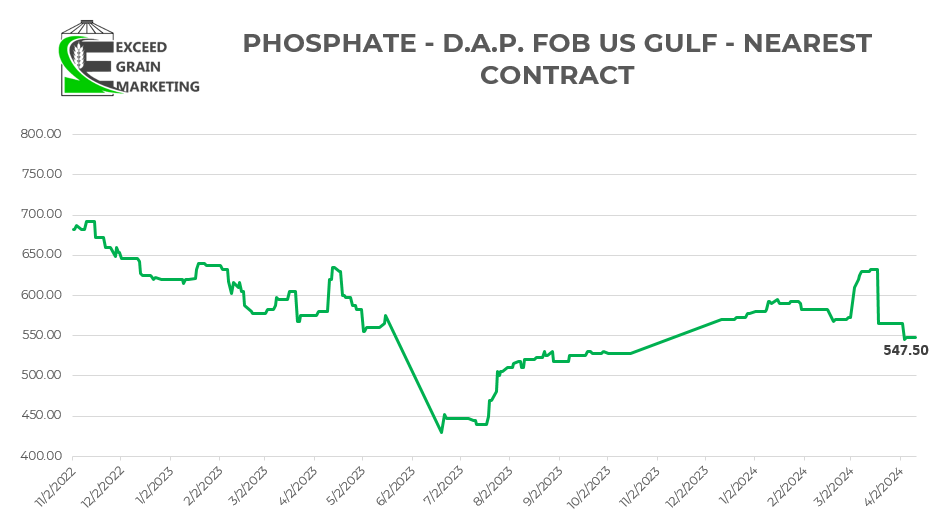

Currency – Energies – Fertilizer

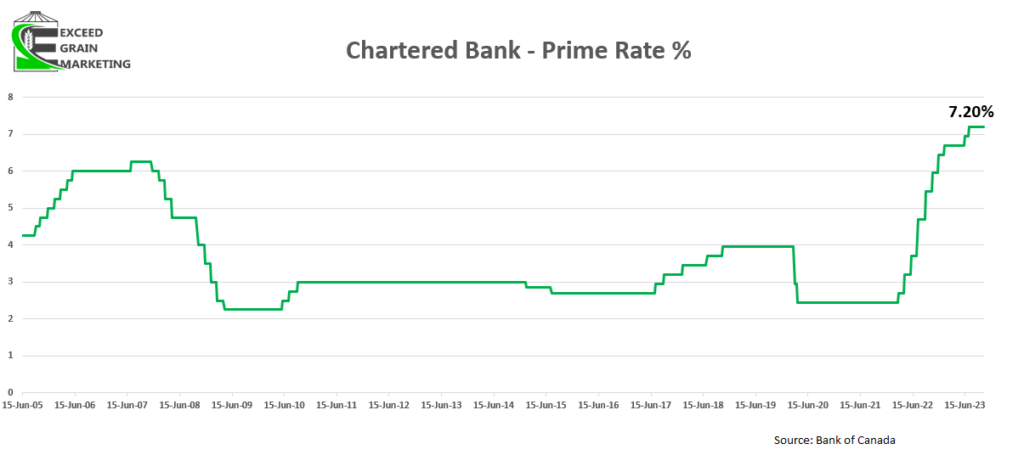

- Bank of Canada Stays Put with current interest rates at the latest interest rate meeting. Prime sits around 7.2% at major Canadian banks. Hinted that we could be higher for longer. Cuts will not be significant if they do come. The Bank of Canada has also recently hinted that one could face another rate hike but it is hesitant to do so given that Canadians are feeling the pinch of higher rates.

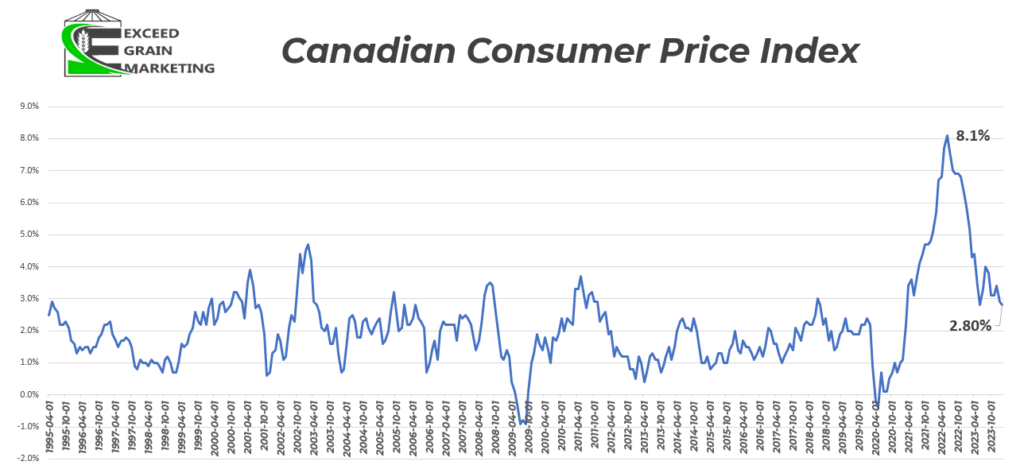

- Canadian CPI Still “Sticky” and sits at 2.9% as of the latest announcement in February.