MARKET OVERVIEW

Grain and oilseed markets finished the shortened trading week under pressure, with the removal of Middle East war risk becoming the dominant theme. The U.S. and Iran have settled their conflict for now, and the Strait of Hormuz has reopened with initial shipping traffic moving through providing more crude oil to the market. That pulled a significant amount of risk premium out of crude oil, sending oil markets back toward pre-war lows and weighing heavily on the veg oil complex. Canola was down $34/MT over the past five trading days, while soybean oil was the weakest market in the group, falling 6.7% on the week. U.S. markets are closed today for Juneteenth, making it a shorter four-day trading week, with futures set to reopen Sunday night. The market will now be watching closely to see whether the U.S.–Iran peace deal holds and whether energy markets can stabilize after the sharp risk-off move.

Soybeans found modest support late in the week after China booked its first confirmed U.S. soybean purchase for the fall shipment window. China bought 132,000 MT, while another 120,000 MT sale was announced to “unknown destinations,” which is often viewed by the trade as potential Chinese demand. That helped soybeans finish $0.08/bu higher over the past five days, despite the broader fund liquidation that has pressured grains in recent weeks. Attention now shifts to Tuesday, June 30, when both Statistics Canada and USDA release seeded acreage reports. These reports will be watched closely, especially in Canada, where seeding was later than normal in some regions. Last year, Statistics Canada’s acreage survey was conducted from May 15 to June 12 and included roughly 25,000 respondents, so the market will be looking for detail around this year’s survey timing, farmer response rate, and whether late seeding was fully captured.

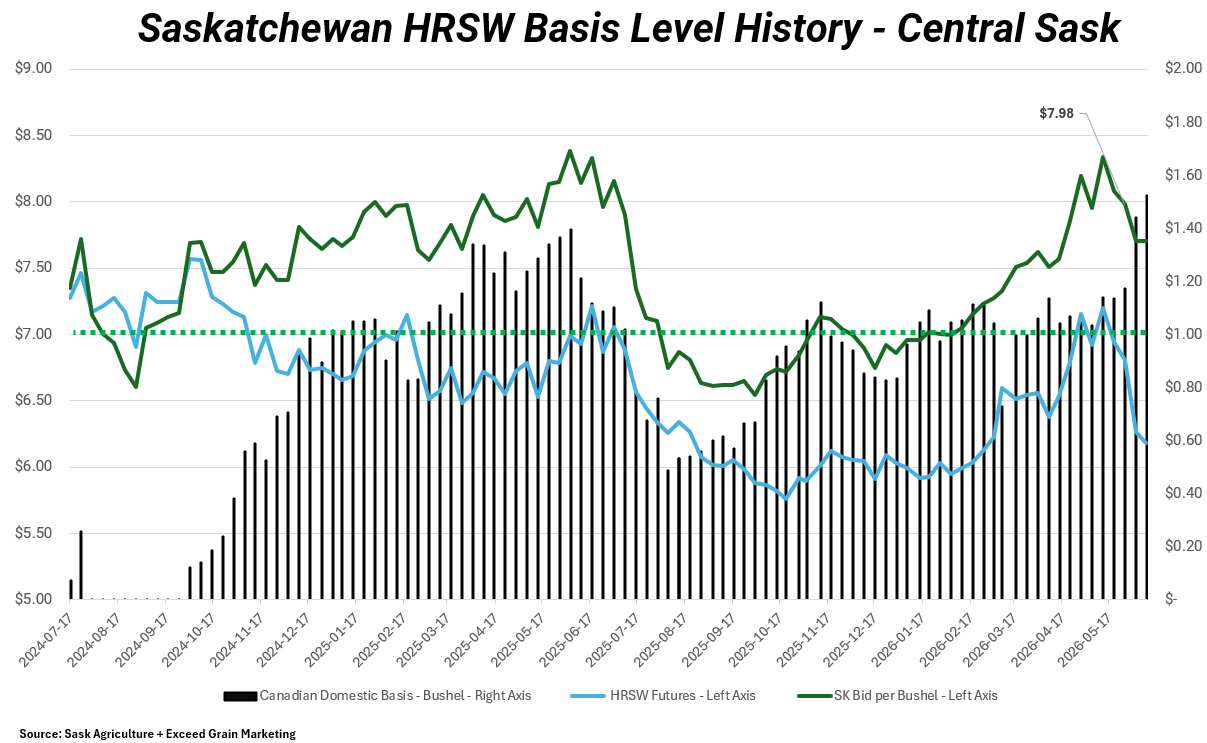

Locally, canola demand remains firm as crushers still appear to have some late-season crush coverage to fill into July and August. Export movement has also been stronger than earlier anticipated, removing some of the supply that domestic crushers expected to access later in the crop year. Wheat cash bids remain relatively strong despite weaker futures, with basis levels at some of the strongest values seen in months. In many areas, cash wheat bids are still holding in the $8.00–$8.25/bu range even as futures have faded. Barley export demand remains active, and oat demand has also started to show up late in the marketing calendar, with several exporters more active in the market over recent days. Overall, futures remain defensive, but local cash demand continues to provide pockets of support across several Prairie markets.

Canola

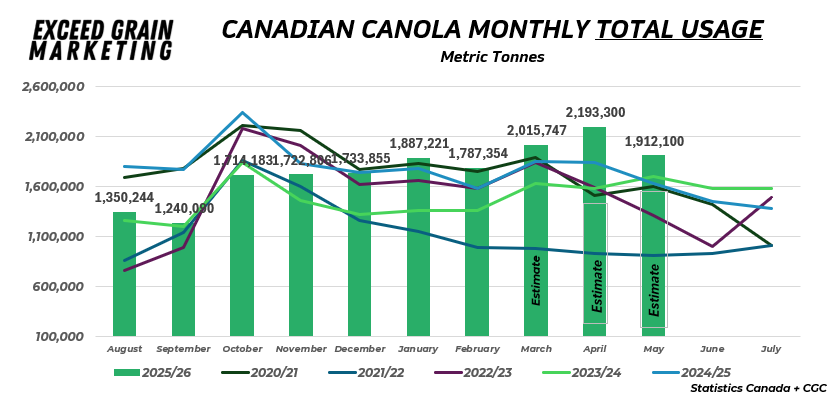

Canola demand remains the strongest supportive feature. Locally, crushers still appear to have some late-season coverage to fill into July and August, which is keeping cash demand active. Exports have also been stronger than many expected earlier in the year, and that movement has removed some of the supply that domestic crushers were likely anticipating would remain available later in the crop year. That does not make the market outright bullish on its own, but it does mean the Canadian balance sheet still has underlying support beneath the futures weakness. New crop business appears to be strong with front month crush filling up but some competitive basis levels further out signaling good demand and we believe a strong export book for off the combine.

The next major focus for canola will be seeded acreage. Next Tuesday, June 30, both Statistics Canada and USDA will release seeded acreage reports, and the Canadian number will be closely watched. Last year, Statistics Canada’s acreage survey was conducted from May 15 to June 12 and included roughly 25,000 respondents. This year, with seeding running later than normal in parts of Western Canada, the market will be watching the survey timing, response rate, and whether late seeding decisions were fully captured in the acreage estimate

Western Canadian crop conditions are establishing well overall. There are still pockets to monitor, especially where excessive rainfall has caused issues, but at this stage there is not a broad Canadian production problem forcing the market to rebuild weather premium as of yet. Lots of growing season ahead of us.

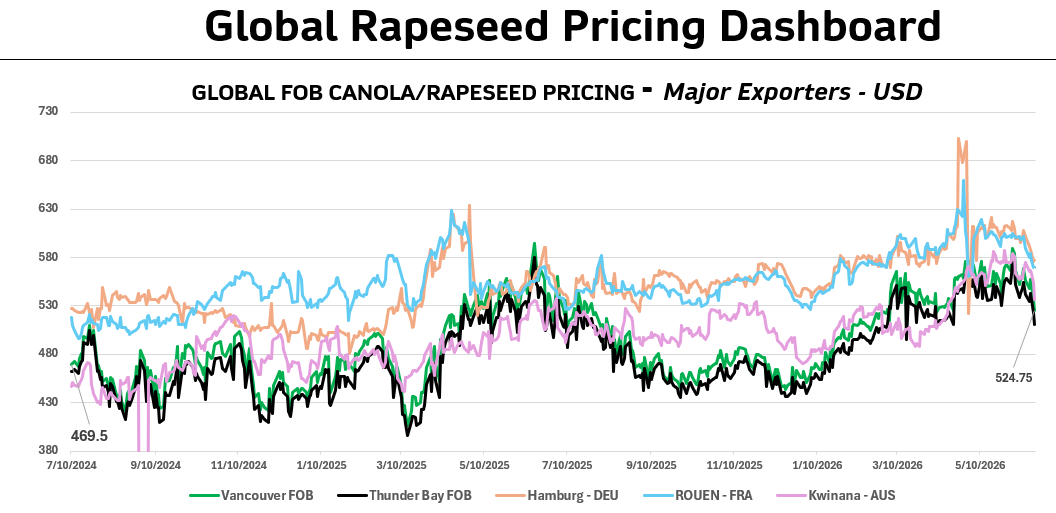

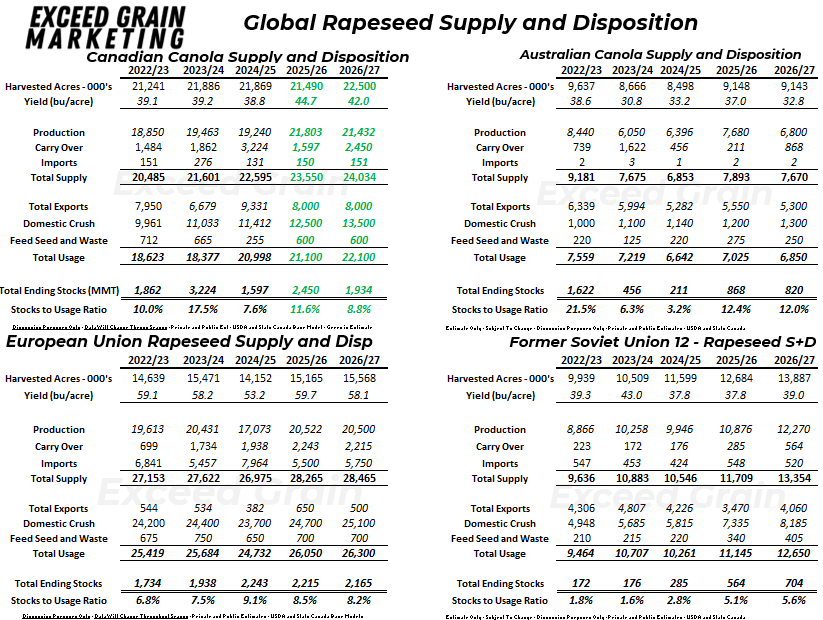

Global competition is also becoming more important. Australia has received strong rains, and while official crop estimates remain near 6.2 million tonnes, production could move higher if conditions hold. The EU is also moving toward harvest with a solid rapeseed crop expected. That does not remove support from Canadian canola immediately, but it could create more export competition later in the season.

What to Watch For In Canola Markets:

- Canadian Crop Mostly Looks Good: Canadian crop looks good overall, despite some areas struggling with wet and unseeded acres. The Peace region of Alberta and far southern Saskatchewan remain the driest areas to monitor, though there is not yet a widespread Prairie production concern.

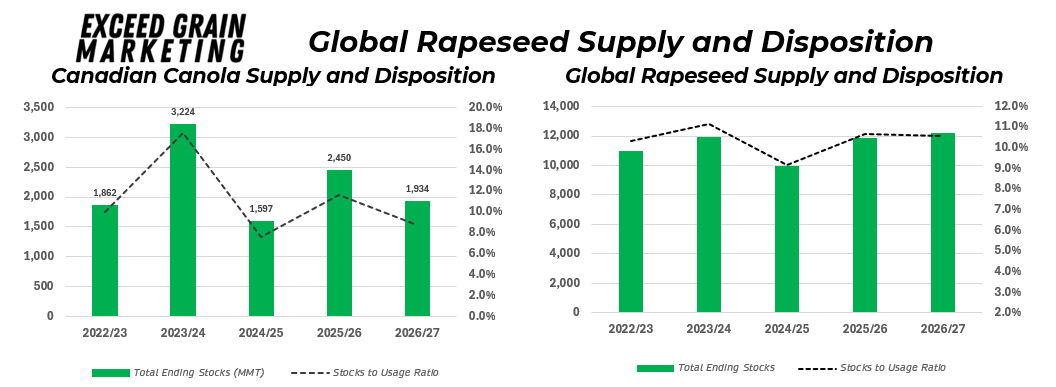

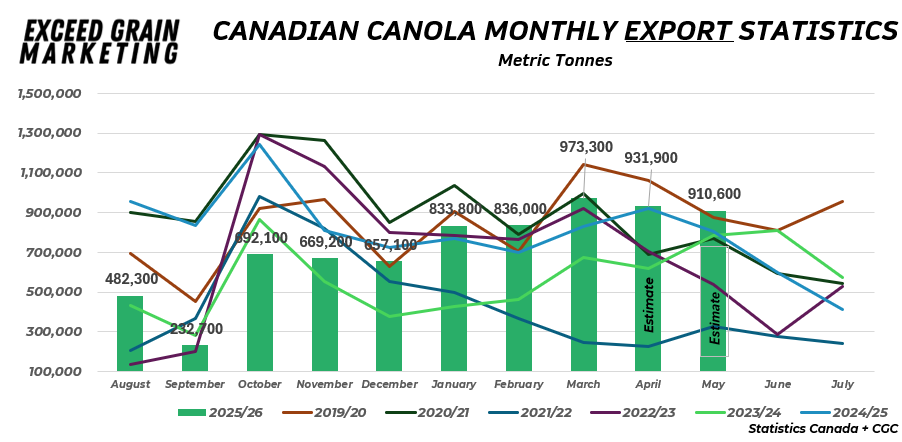

- Old Crop Demand Has Tightened the Balance Sheet: Canadian canola exports are tracking closer to 8.7 million tonnes, far stronger than expectations earlier in the crop year. Domestic crush is also running near 12.5 million tonnes, up roughly 7% year over year. That combination has pulled projected carryout closer to 2 million tonnes, which is relatively tight given the additional crush capacity coming into the market next season.

- Global Supply Competition Is Improving: Australia has received very good rains in recent weeks, improving early new crop prospects. The European Union is also expected to begin harvesting a solid rapeseed crop in July. These crops do not immediately erase Canadian demand, but they do add more global supply competition and could make FOB pricing more important as the market moves into summer.

New Feature: Swipe right or left through the Interactive Charts Below:

Spring Wheat + Durum Markets

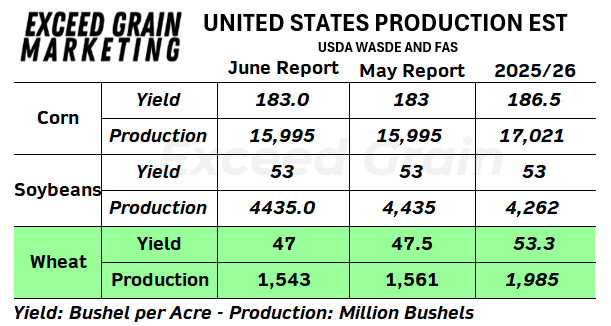

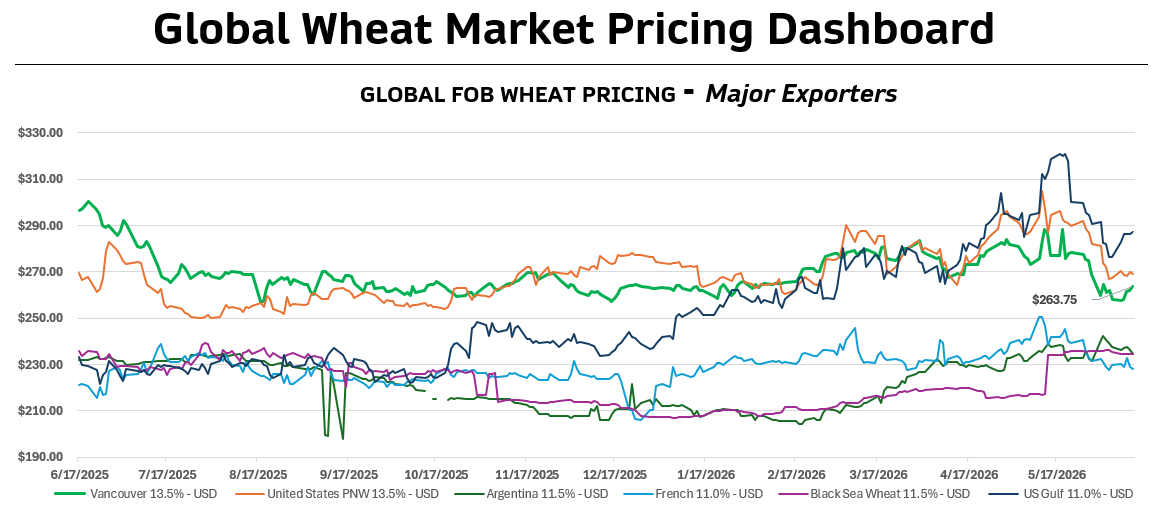

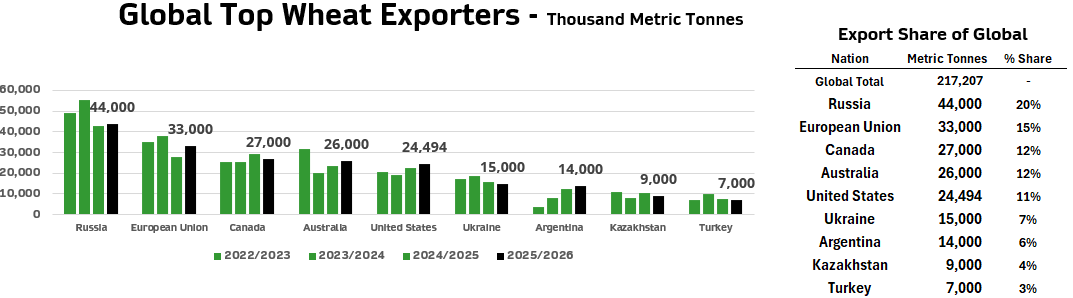

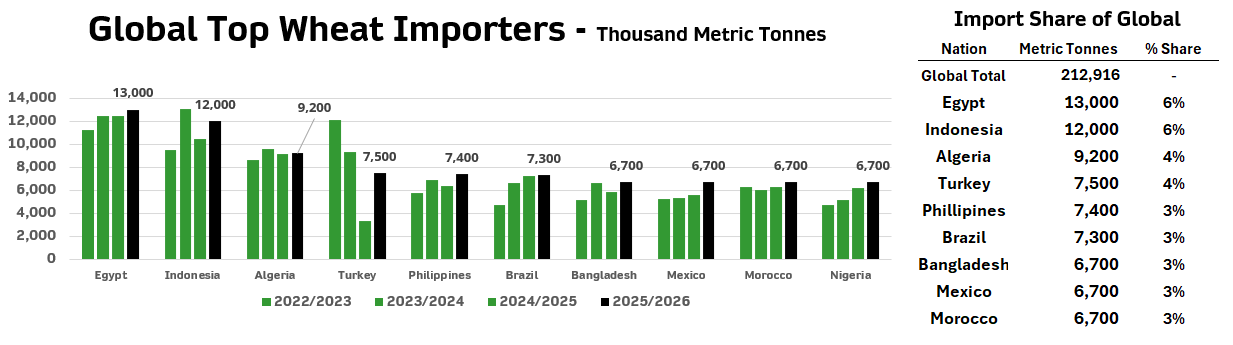

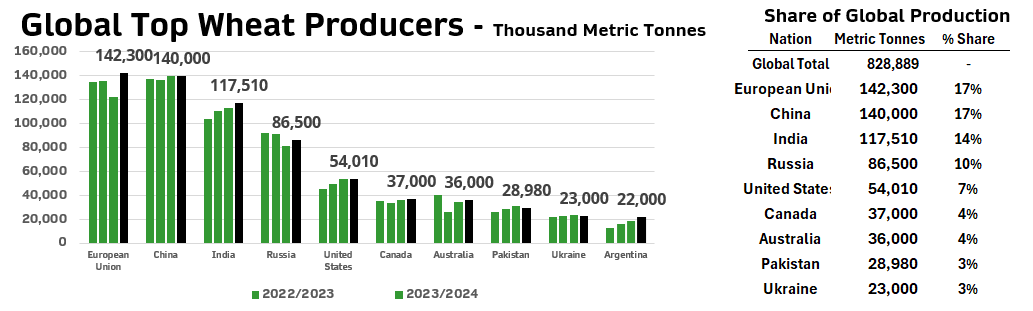

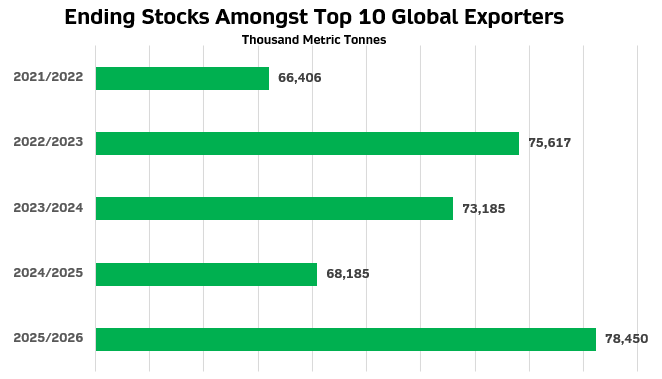

The global wheat balance sheet is still supportive, but not urgent. USDA pegged 2026/27 global wheat ending stocks at 275.4 million tonnes, down roughly 2% from last year. That keeps the world wheat situation from looking burdensome, but it does not create an immediate shortage story either. The market likely needed a larger production cut, a sharper decline in global stocks, or a more meaningful export demand signal to shift sentiment. Instead, the report gave the market enough reason to stay cautious, but not enough reason to rebuild long exposure. Without a weather threat, the market will be hesitant to run the crop higher at this current time.

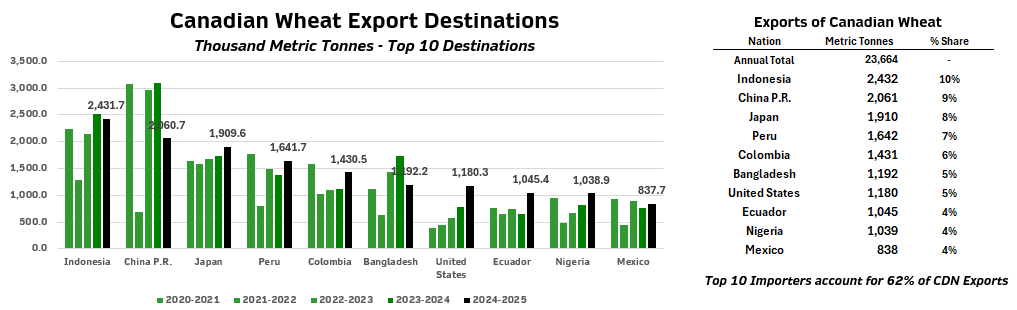

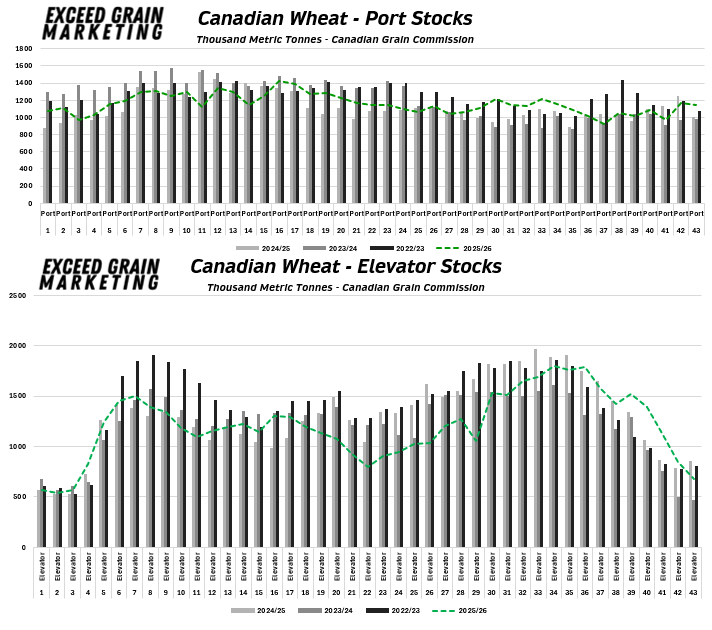

The cash market is telling a slightly different story than futures. In Western Canada, wheat basis levels have strengthened to some of the best levels seen in months. Cash bids are still holding in the $8.00–$8.25/bu range in many areas despite weaker futures, which suggests end users and exporters still need coverage. That basis strength is important because it shows the local market is tighter than the futures board alone would imply. See basis chart attached to the report. Canadian wheat still remains quite competitive for a higher protein wheat and could shape up well for early season exports.

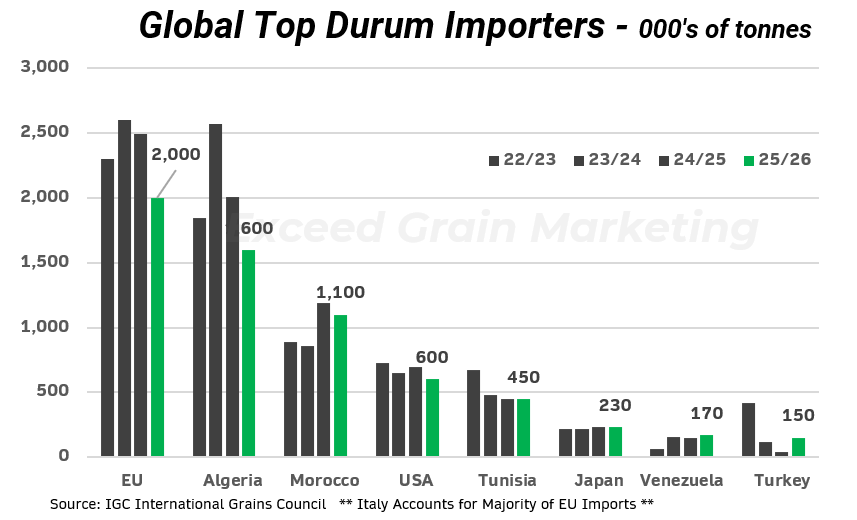

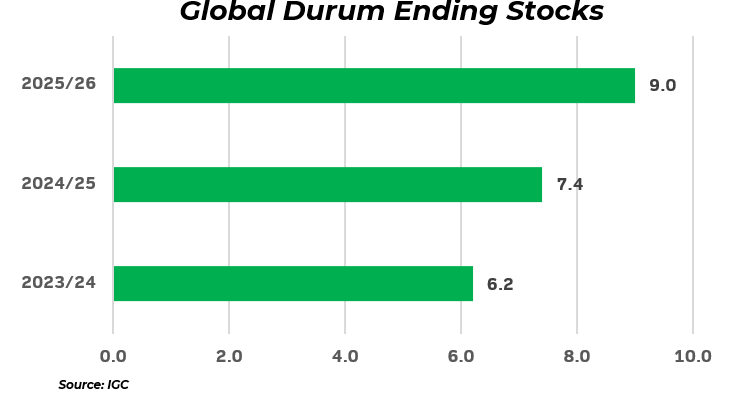

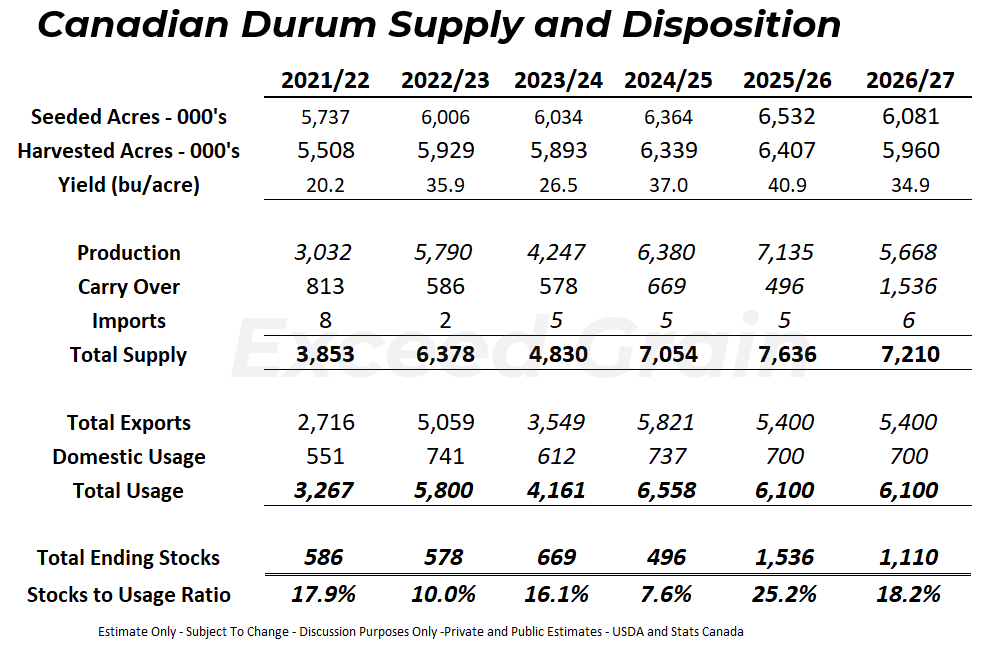

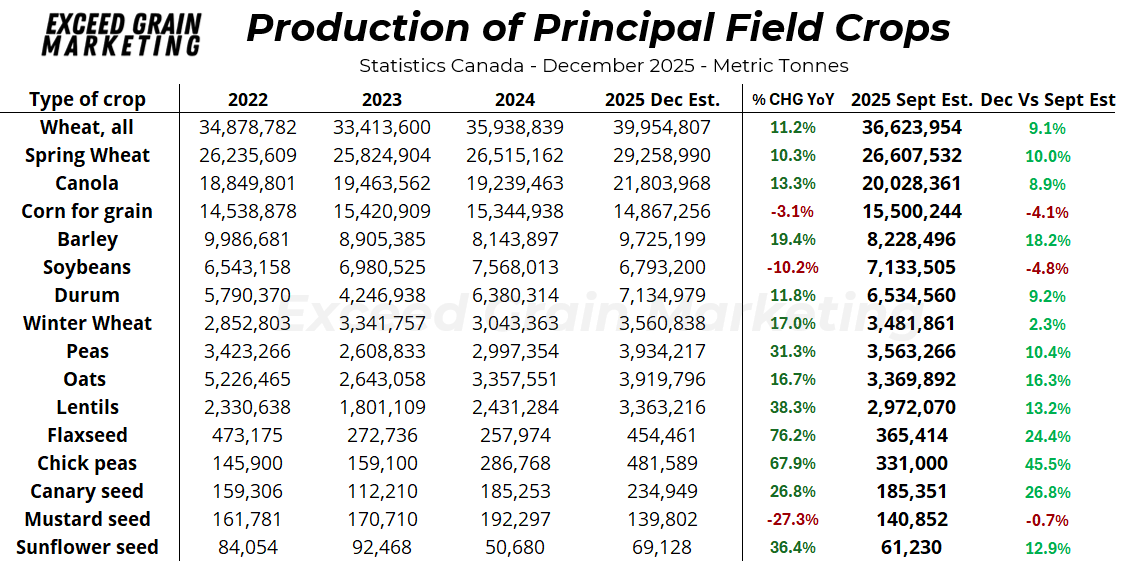

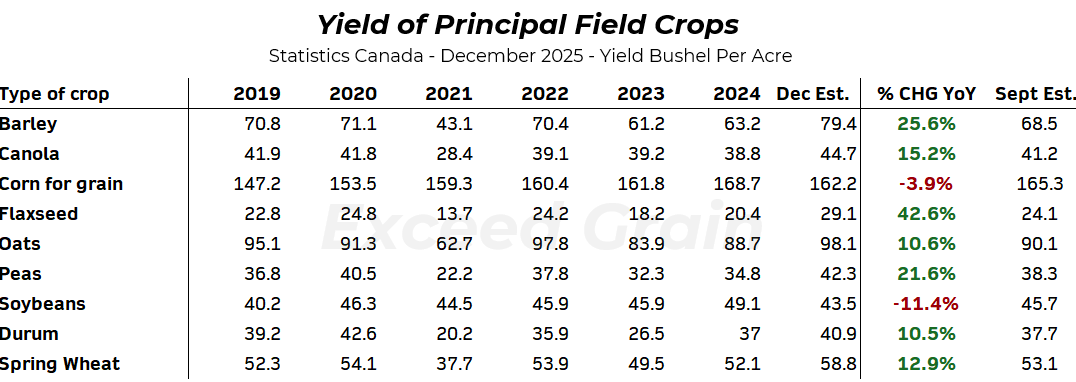

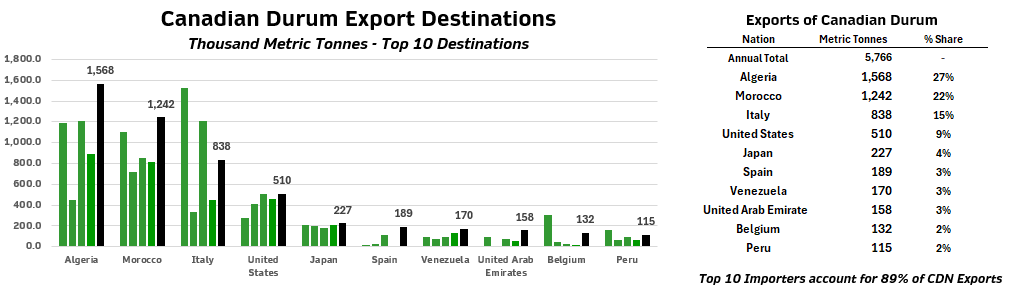

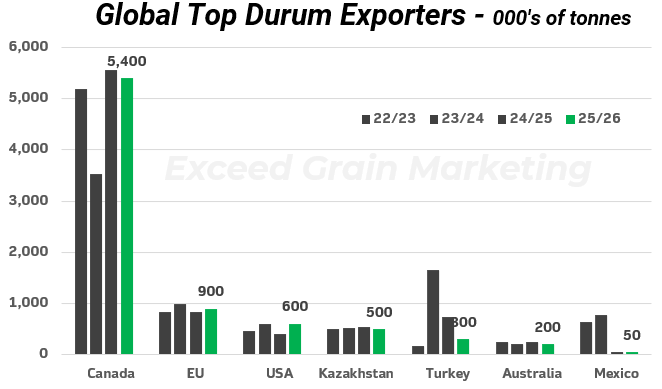

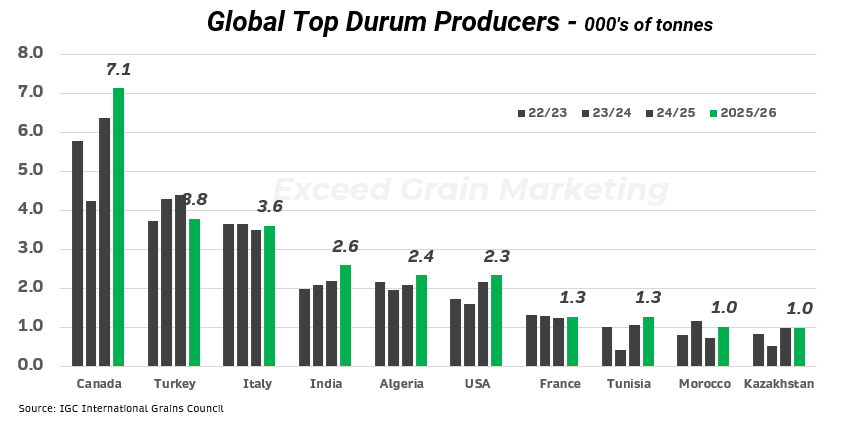

Durum remains quieter than spring wheat, but it is still worth monitoring. Improved crop prospects and harvest progress in North Africa have reduced import urgency into some of Canada’s key durum markets, limiting upside in old-crop values. At the same time, Canadian durum production remains important because the balance sheet does not have a large cushion if Prairie weather turns adverse. Current estimates point to Canadian durum acreage and production being down roughly 1 million tonnes year over year, which keeps the market sensitive to any production issue later this summer. It will be interesting to see the June 30th Durum figure as it ends up and we will have that data avaliable shortly.

Overall, wheat futures remain defensive, but the cash market is holding together better than the board suggests. WASDE confirmed smaller U.S. supplies and lower global stocks, but not enough to spark any interest in the futures markets. Durum remains steady but flat with North African crop harvest limiting demand urgency. Wheat markets will need to reassess whether prices have fallen far enough relative to smaller U.S. supplies, stronger Canadian basis, harvest quality risk, and still-uncertain global production.

What to Watch For In Wheat Markets:

- June 30th USA and Canadian Wheat Acreage: Less or more than the market anticipates will lead to short term moves and could create opportunity

- Harvest quality still matters: USDA confirmed smaller U.S. wheat supplies, and winter wheat harvest quality remains a key risk as rain moves through harvestable areas. The HRW drought story is already well known, but wet harvest conditions can still create protein and quality issues. French wheat conditions, Chinese harvest quality rumours, and Northern Hemisphere weather all remain worth monitoring.

- Durum and global supply need reassessment: Durum remains flat as strong North African crop prospects limit import urgency, but the market will reassess quickly if Canadian production risk develops. More broadly, Australia and Argentina are expected to produce smaller wheat crops than last year, which may matter more once fund liquidation slows. Wheat has lost momentum, but global exportable supply still does not look overly comfortable.

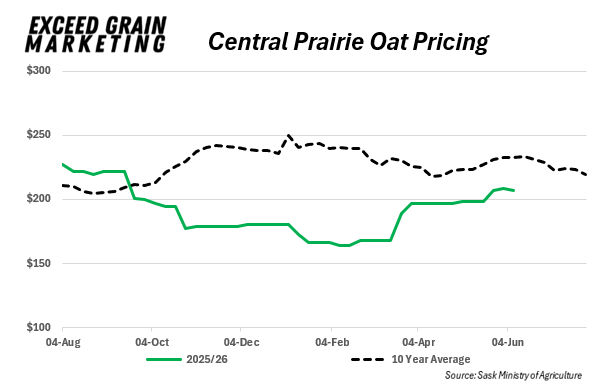

Oat markets bids have improved from winter lows in some regions, but the move has not been aggressive enough to suggest a major demand shift. End users appear to be covering needs selectively rather than chasing the market higher. $3.50 central Sask, $4.20 central Manitoba

Acreage remains the bigger underlying story. Oat area is expected to be lower as producers continue favouring canola, wheat, barley, and other crops with stronger economics. For now, the market does not appear overly concerned, likely because demand has also been quiet. However, if acreage is meaningfully lower and summer weather becomes less cooperative, oats could become more sensitive later in the season. 2026/27 balance sheet looks tightening. Oat market watching the June 30th report very closely

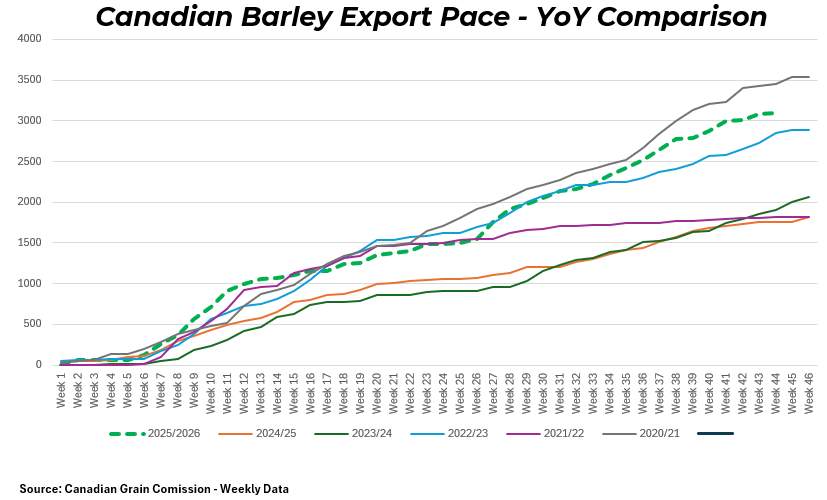

Barley markets flatening and pulling back slightky in recent days as old crop coverage is being met by end users. Old crop malt values remain very close to feed barley prices as domestic maltsters appear to have covered most nearby needs. New crop feed barley bids are generally above $5.25 while malt opportunities are only carrying roughly a $0.75 premium in many cases.

Canadian barley acreage is expected to increase roughly 5% year over year and could climb even higher depending on how planting progresses through late May. Statistics Canada also revised Canadian barley production estimates higher recently.

Despite larger acreage expectations, exports continue running very strong at roughly 70% ahead of last year with Canadian barley pricing competitively into global feed markets. Planting delays across portions of Saskatchewan remain supportive near term, particularly in northern growing regions still dealing with cool and wet conditions. The stronger exports are tightening the balance sheet and we will soon provide fresh S+D estimates for the Canadian crops

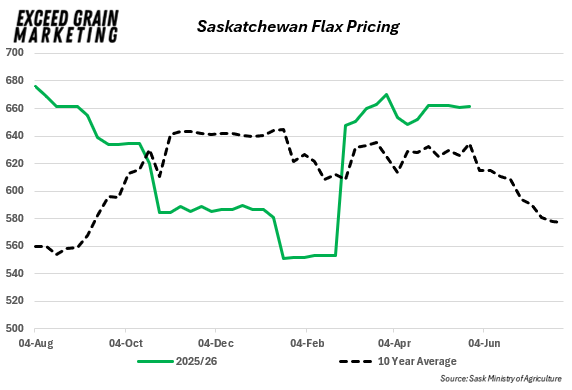

Flax markets continue trading in a relatively quiet tone overall with expectations for Canadian flax acreage up roughly 20% to 21% year over year. However, acreage estimates remain somewhat questionable now that prices have softened from earlier highs and other crop economics remain more attractive in many regions.

Canadian flax supplies are currently viewed as relatively comfortable overall with larger Kazakhstan production also adding pressure to global balance sheets. Stocks-to-usage projections for Canadian flax remain fairly large unless some stronger export demand unexpectedly develops later in the crop year.

Recent strength in vegetable oil markets has provided some modest support to flax values

Canary seed markets continue trading under pressure overall with Canadian ending stocks projected near 171,000 tonnes which is considered a very heavy carryout for the market. Current values remain in the low $0.20 per pound range, well below the $0.30 levels seen prior to spring seeding last year. The weaker pricing environment is expected to result in a meaningful drop in acreage for 2026 as producers shift toward crops with stronger economics.

Despite the large carryout projections, canary seed markets can sometimes behave differently than traditional row crops as producers are often willing to store the crop longer term rather than move it as an immediate cashflow commodity. This tends to keep inventories in tighter hands and can limit how aggressively ending stocks alone pressure the market. Canary seed bids have improved modestly over the past few weeks, however overall market tone remains relatively soft given the comfortable supply situation.

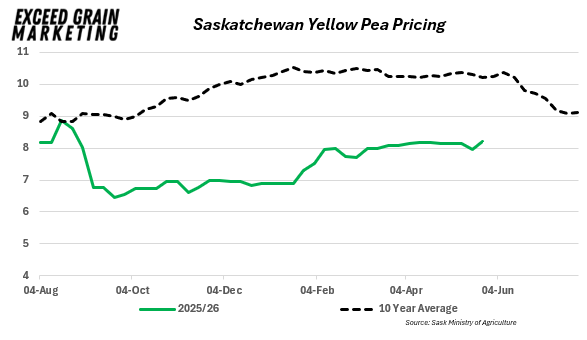

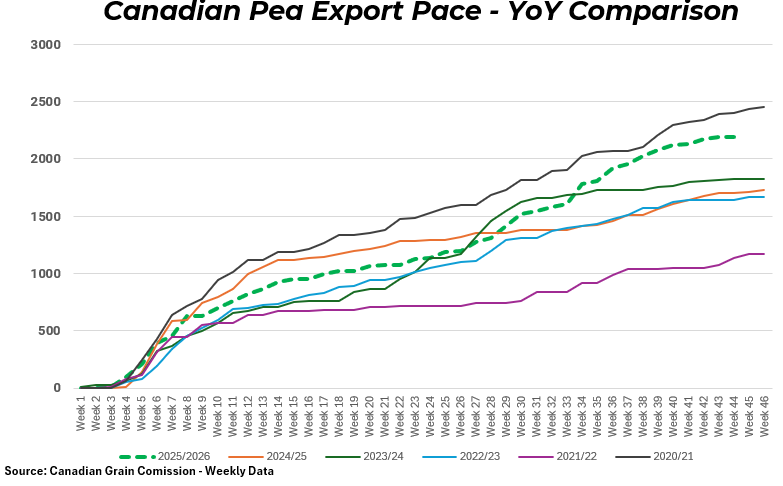

Pea markets continue trading in a relatively flat and comfortable tone overall with domestic yellow pea bids generally around the $8.00 per bushel range. New crop bids are also not showing much aggressiveness at this point with most opportunities remaining near that same $8.00 area.

The market continues facing expectations for a relatively large carryout moving into the next crop year and stronger export demand will likely be needed to tighten the balance sheet meaningfully. China remains the key demand factor the market continues watching as additional Chinese buying would be needed to help absorb larger available supplies.

Foreign yellow pea values have also strengthened modestly recently which has helped support the overall market and allowed Canadian bids to stabilize around current levels. Pulse acreage overall is still expected to decline year over year across Western Canada as producers continue favoring stronger economics in competing crops. We will watch Indian Monsoon Season which is just beginning and the initial rains have been later than anticipated. One report suggests rainfall totals are 40% below normal so far.

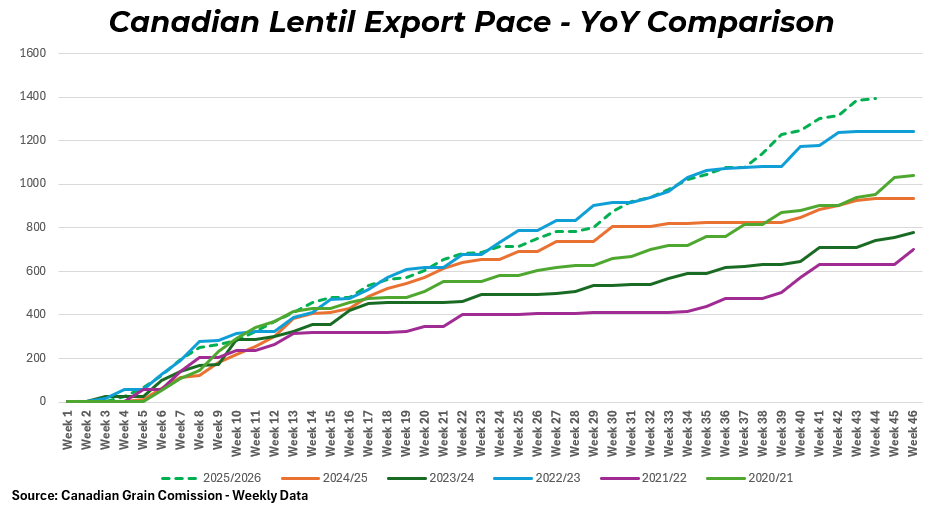

Lentil markets continue holding a relatively steady tone overall with red lentil bids generally in the $0.26 to $0.27 per pound range while large green lentils continue trading closer to the $0.25 area. New crop red lentil interest has also been surfacing around the $0.24 per pound mark as buyers begin working coverage for the upcoming crop year.

The lentil market continues balancing expectations for burdensome Canadian ending stocks, particularly in green lentils, against lower acreage expectations across parts of North America. U.S. lentil seeded area is expected to decline roughly 22% year over year which could help tighten North American supply somewhat moving forward.

Prairie planting progress for lentils has generally been advancing at a reasonable pace overall. Parts of southern Saskatchewan lentil country received some beneficial rains this week following earlier dryness and extreme winds that had been creating some concern around establishment conditions. Forecasts continue calling for warmer temperatures moving forward with scattered thunderstorm activity remaining in the outlook.

Overall, lentil markets remain relatively rangebound for now with the trade continuing to monitor final seeded acreage, export demand and growing season weather through early summer.

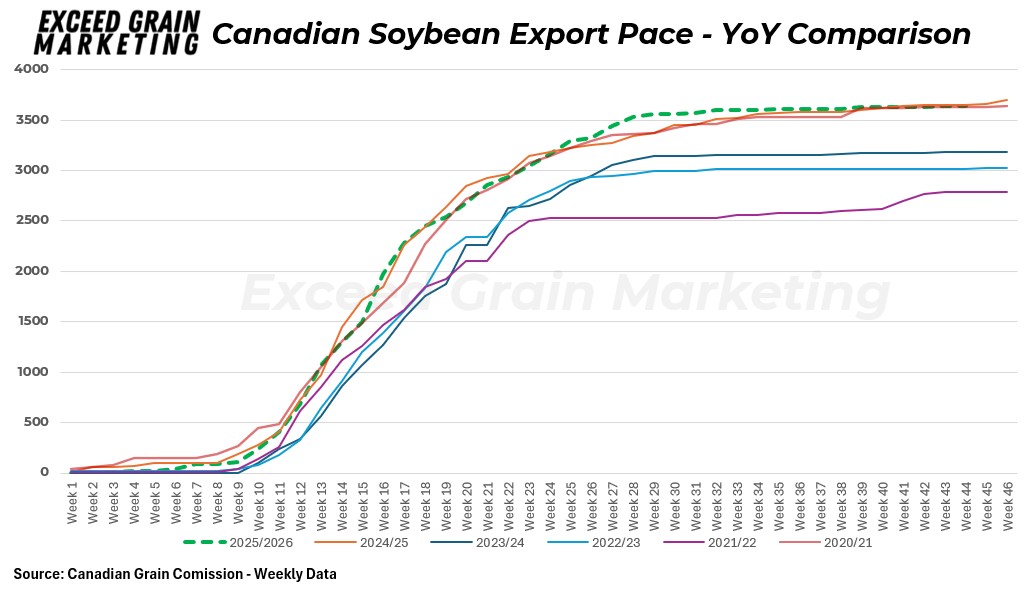

Soybeans- Manitoba new crop soybean bids continue trading around the $13.50 range with producers still able to find some marketing opportunities at times depending on delivery period and location.

Canadian soybean export pace has remained relatively strong overall this crop year, although movement typically begins slowing seasonally at this point in the year. Manitoba remains the primary focus for Canadian soybean pricing and export movement as the province continues dominating Canadian soybean production.

Markets shifting to US production season.

Corn Manitoba cash corn values generally around the $5.75 range for both nearby and new crop opportunities. Fall delivery bids continue carrying a slight premium which suggests the market remains relatively comfortable with current stock levels and is not aggressively chasing nearby supplies at this point.

Feed grain supplies across Manitoba remain more abundant overall compared to recent years with stronger corn production helping keep feed markets relatively well supplied. Domestic demand remains steady, however the market is not currently facing any major supply concerns locally.

Globally though, corn balance sheets remain tighter than they were just a few years ago. The USDA May report projected global corn ending stocks below 280 million tonnes compared to roughly 314 million tonnes seen only a few seasons back. Despite that, market direction moving forward will remain heavily dependent on the upcoming U.S. corn crop and summer weather conditions across the Corn Belt.

U.S. planting progress overall has advanced well so far with no major production threats developing yet. As planting wraps up, markets will increasingly shift focus toward weather, crop ratings and yield potential through June and July.

Our market intelligence reports incorporate information obtained from various third-party sources, government publications, and other outlets. While we endeavor to maintain the highest standards of accuracy and integrity in our reports, we acknowledge that the information provided may contain inadvertent errors or omissions. As such, we accept no liability for any inaccuracies or missing information in the data presented. Furthermore, these reports are not intended to serve as standalone investment or financial advice. We strongly advise that any financial or investment decisions be made in consultation with a professional market advisor. Reliance on the content or forecasting provided within of our reports for making financial decisions without such professional advice is at the sole risk of the user.