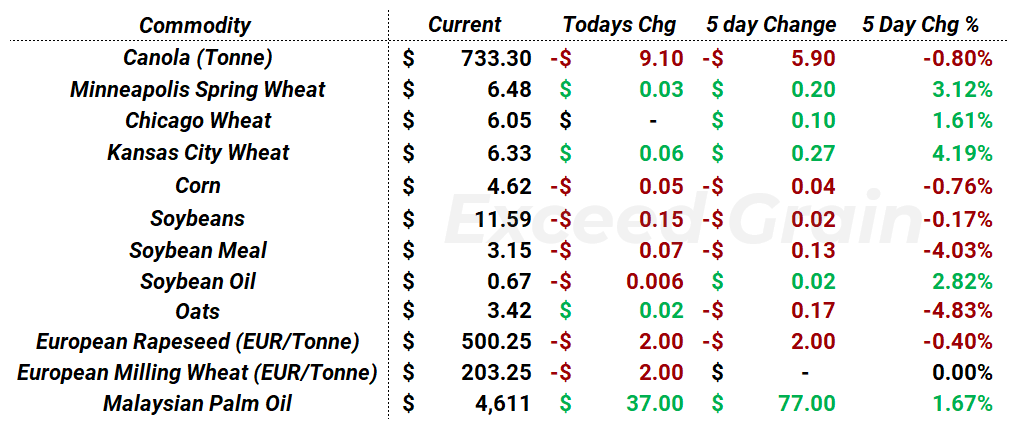

MARKET OVERVIEW

Markets waited all week to see the Renewable Volume Obligation and biofuel data set to be released by the EPA at the WhiteHouse this week. The blending mandates came in around what the market was anticipating. The market will begin to discount foreigh feedstock and their tax incentives beginning in 2028 at half the value. Although the wording is unclear, Canadian and Mexican feedstocks are anticipated to be considered “Domestic Feedstocks” and the discounts are more targeted towards the overseas feedstocks such as Used Cooking Oil. The vegoil market in general retracted by around 1.2% today for both Canola and Soybean oil futures markets. This announcement has been the “Big Story” markets have been awaiting and much of the rally in vegoils was dependant upon these numbers. Markets will shift their focus next week to the March 30th USDA prospective plantings report. Also we will begin to trade northern hemisphere weather stories. Most of the European Union looks alright in terms of soil moisture conditions right now, problem areas beginning to show ahead of planting in the United States. Canada still 3 weeks to 1 month away from planting.

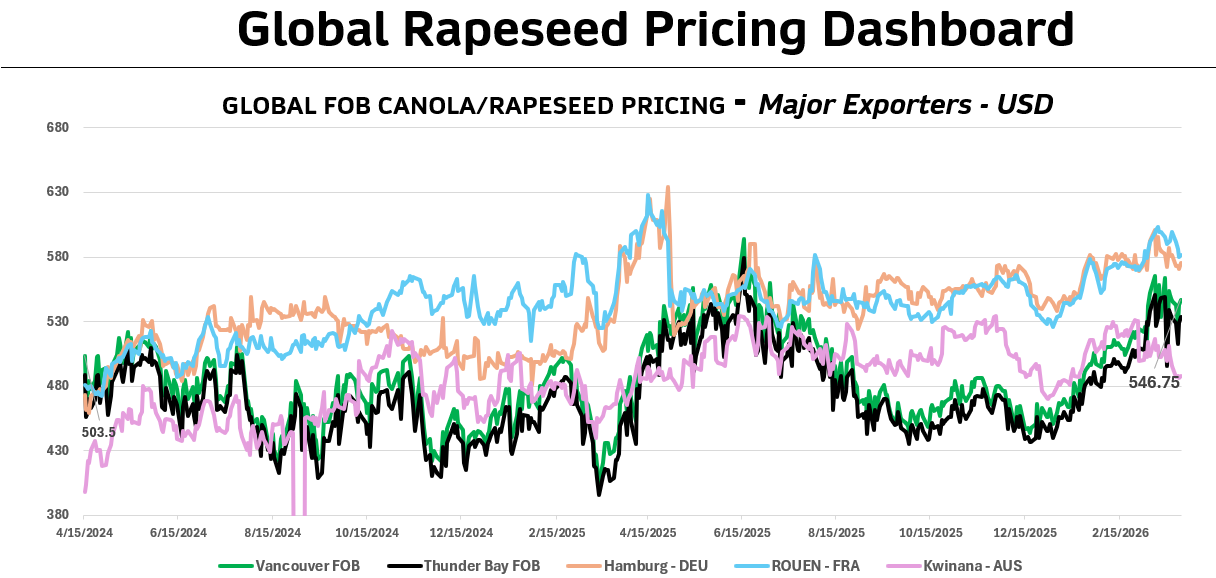

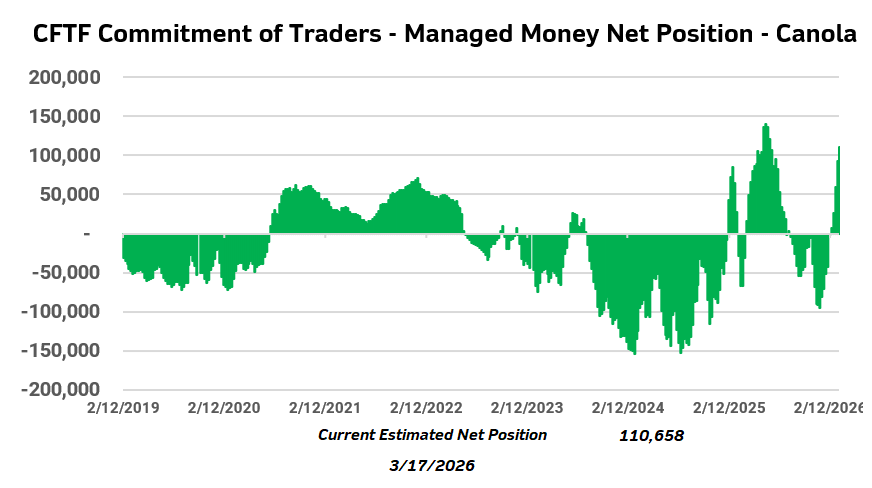

Futures chart, Canola futures are still sitting close to the highest levels since 2023 with the exception of Junes peak of last year but have been pulling off of peak values. This is war risk premium vs fundamental moves. If a fundamental move such as drought were to follow, could keep market supported. All futures have been taking a nice leap this past month. Canola and all these markets need to be closely monitor as especially for Canola we are entering some lofty futures levels we have not seen for quite some time.

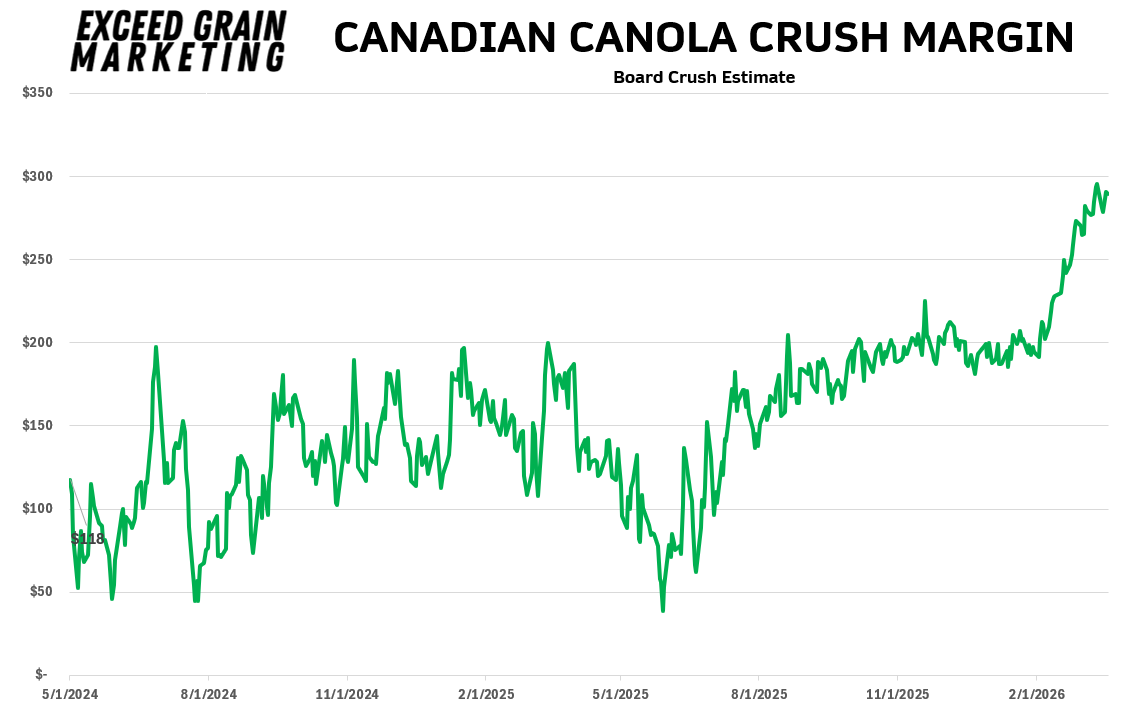

Canola has spent less than a week above these levels since late 2023. Work with your local advisor to make sure you are protecting yourself properly. The take home message for today is, know your risk and where you want to be situated in this market. Basis levels can typically widen out or basis can fill at crushers. We are seeing this happen at domestic consumers already. Know when you need your movement and remember that the crop needs to move eventually, just how are we going to go about the movement.

World will keep focus on the ongoing concerns of the Iranian war, mostly regarding the Straight of Hormuz as 35% of global nitrogen and 20%+ of global energy flow through the straight. Globe also shifting into focus on the Northern Hemisphere grain production regions and how they come out of winter wheat dormancy and how the weather prospects sit for Canada, European Union (Germany+France), United States, Russia, Ukraine over the coming weeks

Canola

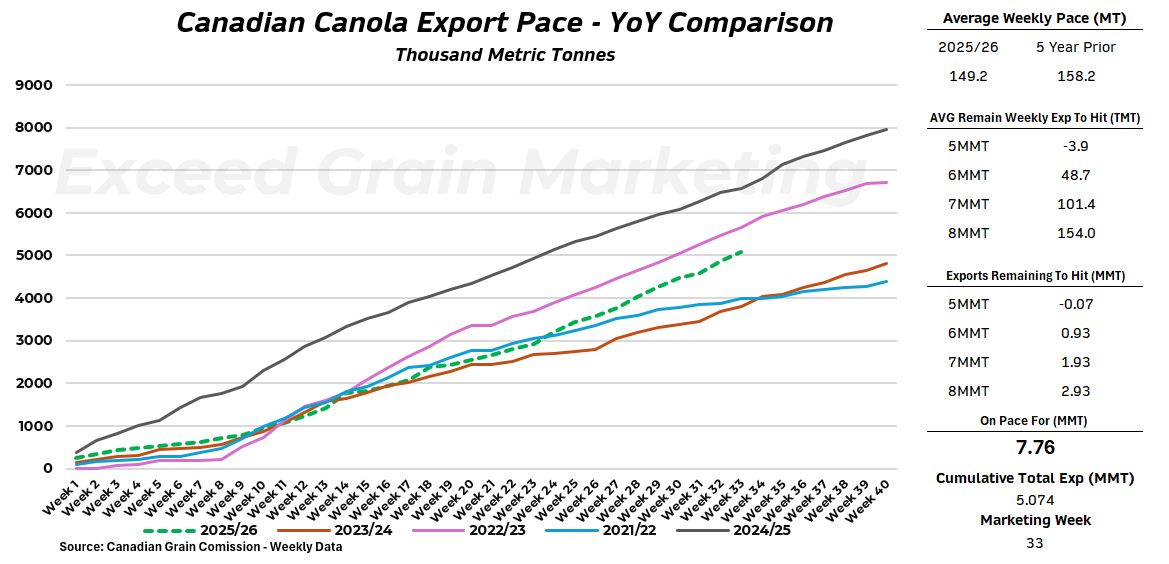

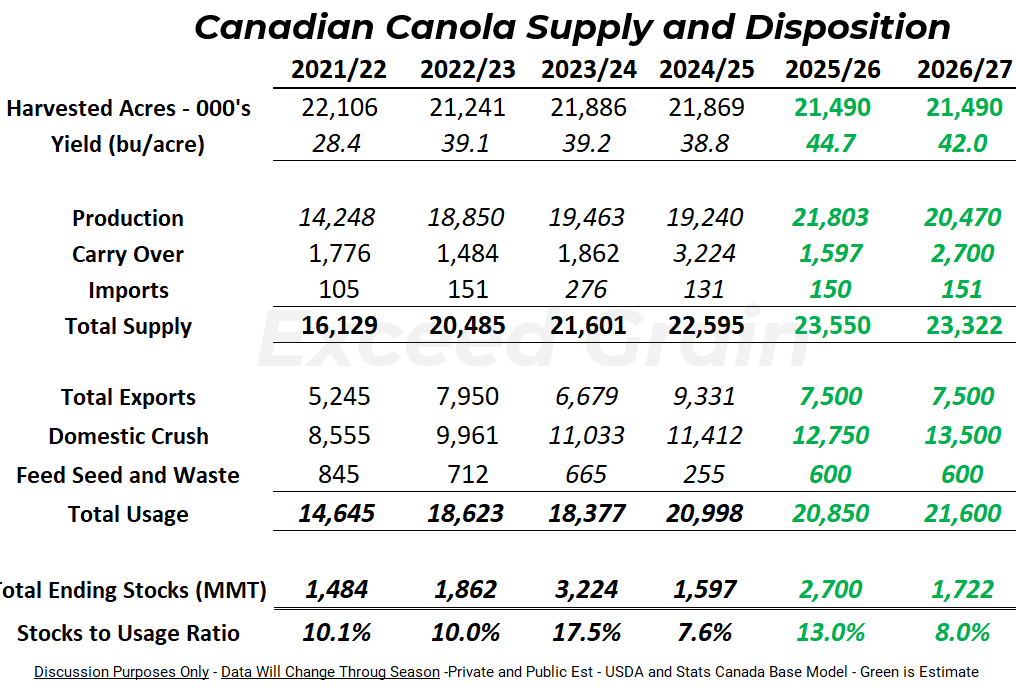

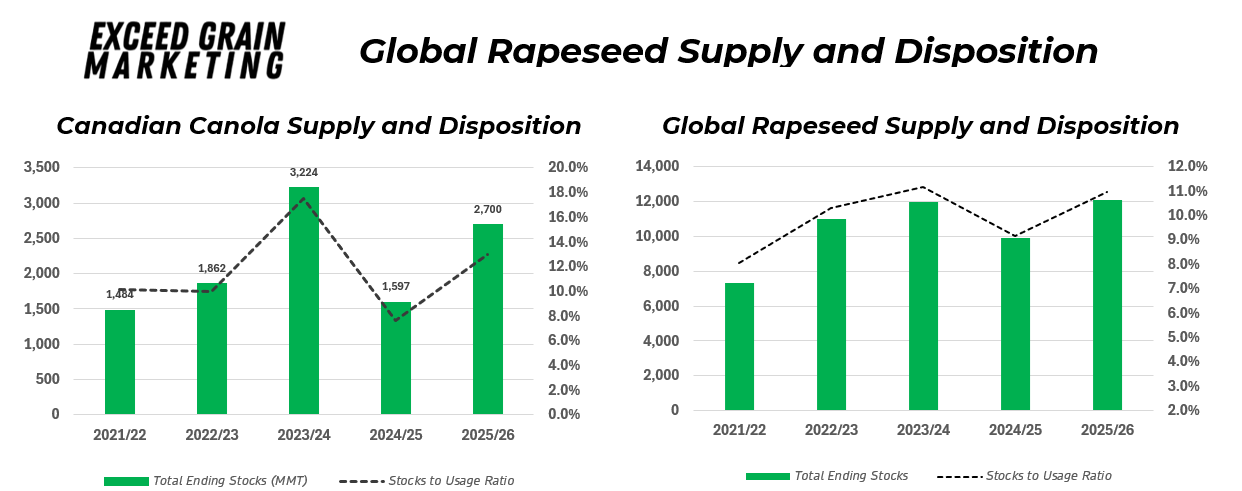

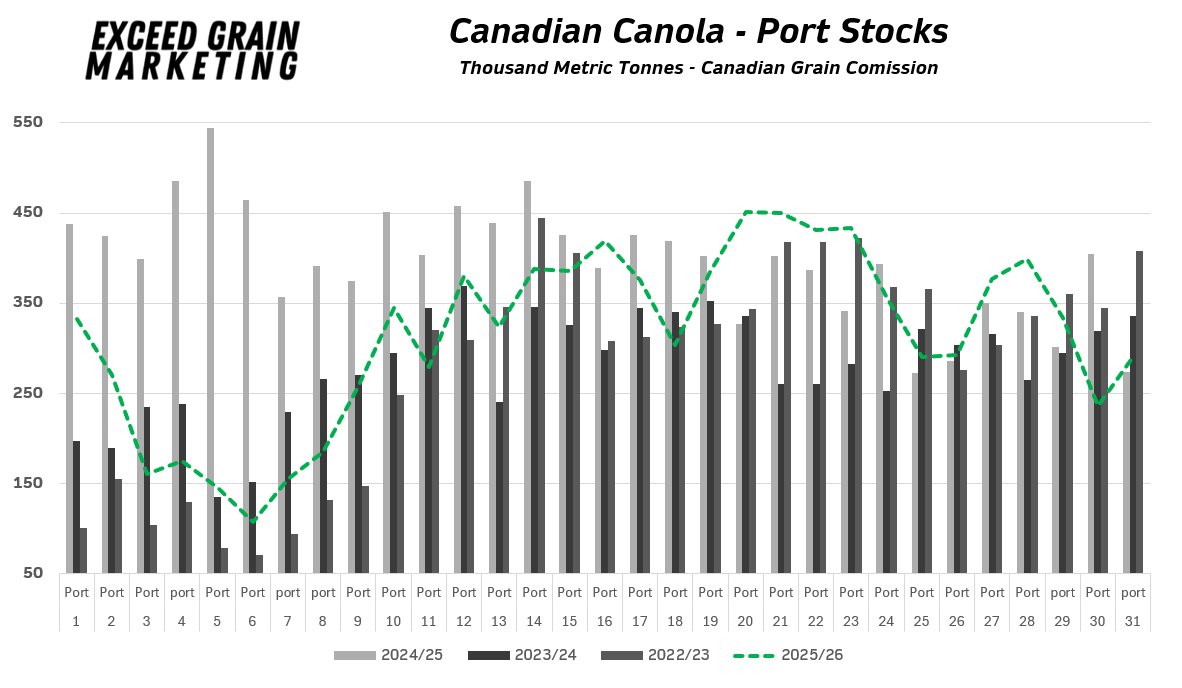

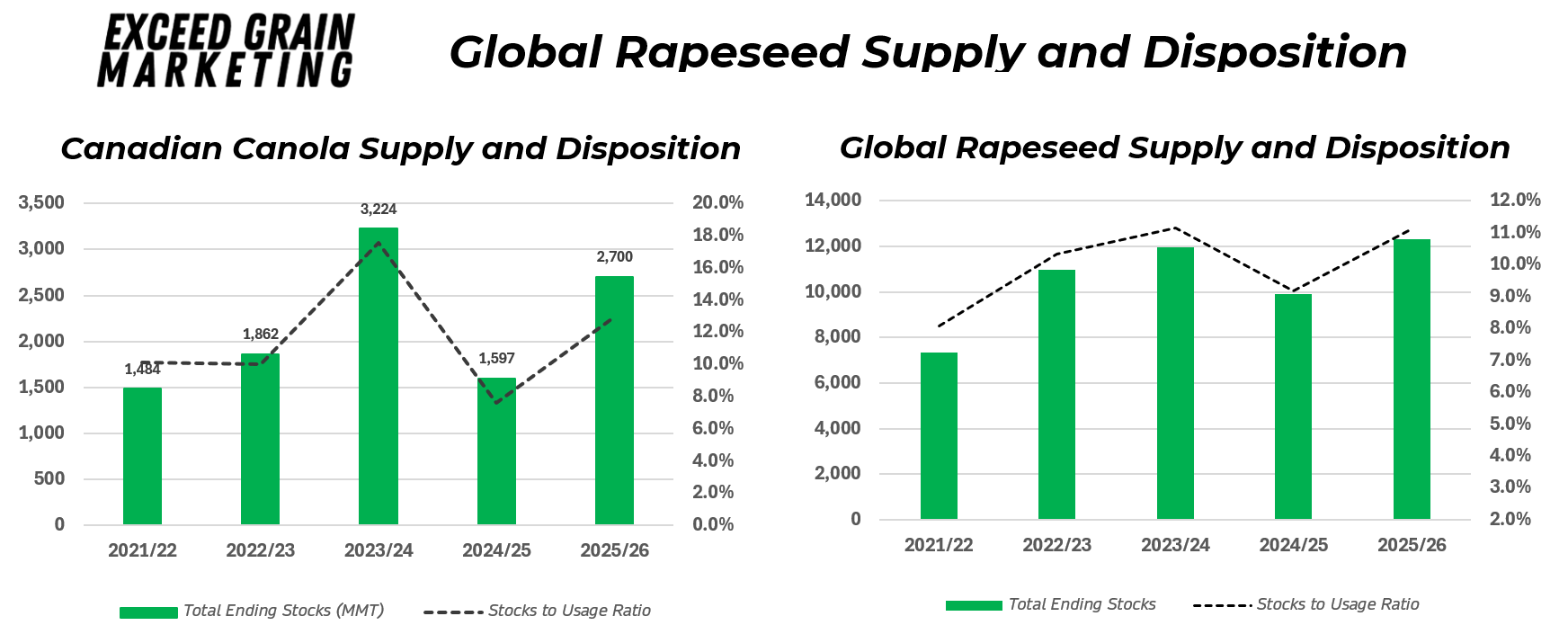

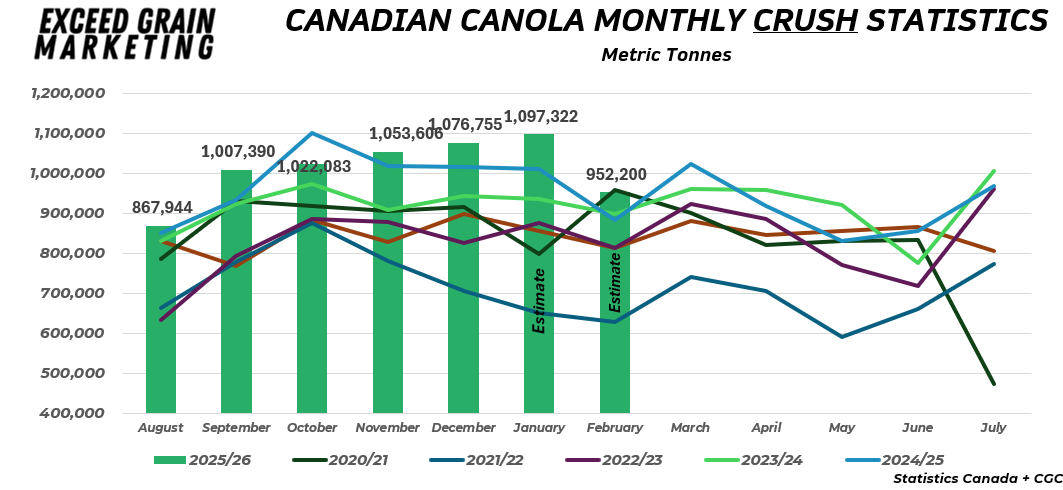

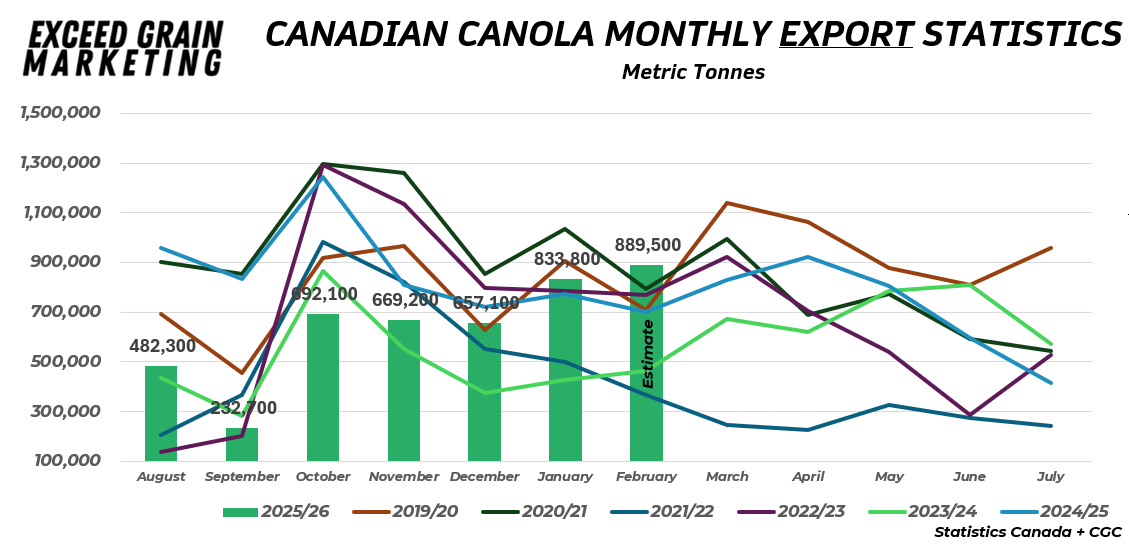

Canola futures levels playing in the range of values at or near the highest point since 2023. Producers need to be extra cognizant of direction from here on out. Much of this is war risk premium attached. Canola export pace of 7.8mmt is really getting exports going swiftly and export pace is up about 1.8mmt from where we were projected at the beginning of the crop marketing year. Keep in mind export expectations at the beginning of the year was 6.0mmt. Less grain in the ports due to aggressive sales in recent weeks, elevators inland are bidding higher and scouring for more tonnage. China has been in the market for around 11 publicly recorded shipments since announcing a reduced tariff on Canadian canola from 75% down to 15%. This week The tariff has been extended for 5 year and is listed at 5.9% plus the standard 9% tariff that is in place already on imported product.

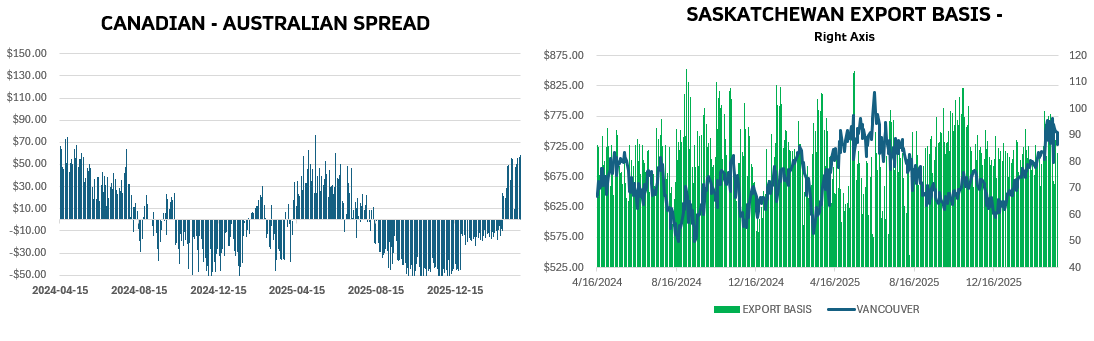

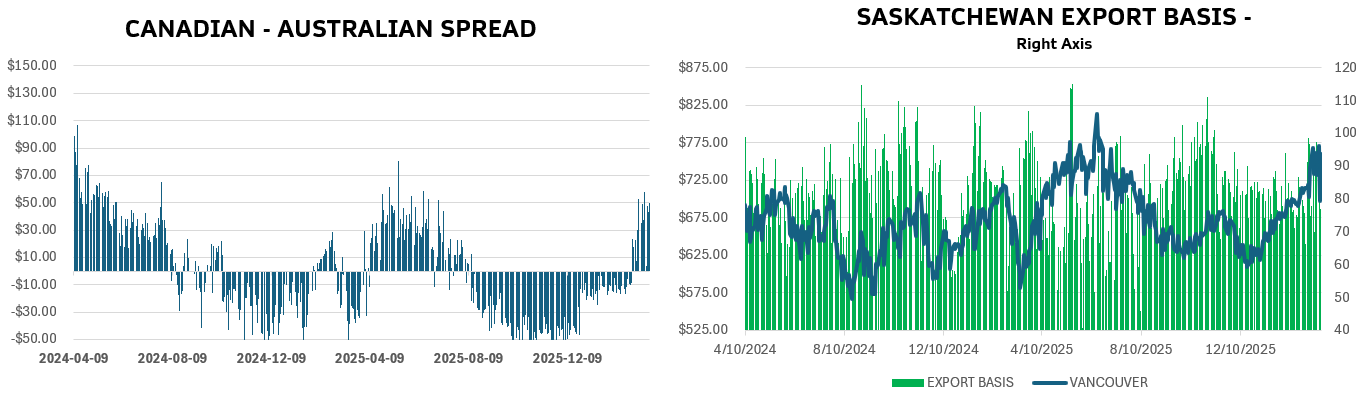

Australian Canola now cheaper than Canadian Canola. Need to keep close eye on this as it could hamper export flows. Chart attached for reference. China has been anticipated to be running low on rapeseed inventories. The market will continue to look to see how Chinese and Canadian relations move forwards from here. As of Week 33. Canola exports on pace currently for 7.8mmt. Domestic Consumption on pace for around 12.5 MMT vs last years 11.5mmt. We will see how new crush and what timeframe new capacity comes online to finish off the market year Markets need to see an export pace of closer to 8mmt to gain real ground and tighten up the balance sheet enough to draw down supplies to a sub 3mmt carry. Each week that progresses leaves less of a chance of pushing towards this number. European Union (20mmt per year producer) has a nice looking crop coming and is in its early infancy of the crop cycle. Watch for newsJuly on this harvest.

What to Watch For In Canola Markets:

- US BIOFUEL Policy –

United States Governement is expected to announce US Biofuel Policy for RVO’s which is Renewable Volume Obligations on or before March 27th. There is a “Celebration of Agriculture” March 27th at the White House to line up with the announcement.This was released today, March 27th at 12:30 Eastern Time. The news was neutral and largely met what the market was looking for. Selloff in vegoils on more of a “Buy the Rumour – Sell the Fact mantra”. Canola and Soybean Oil fell 1.2% on the trading session. - Iran War Crude Oil and Global Volatility on Energies and Market Sentiment.

- Basis At Major Risk of Filling. Crush capacity filling for Summer Months

- Canadian Export Pace. We are watching port stocks. Currently on pace for 7.8mmt. This pace if maintained pushes us below a 3.0mmt carryout.

- Canadian trade optics: How does US – Canadian relations play out heading into summer when USMCA needs to be renegotiated? Chinese and Canadian relations – Warming. First 11 ships have been spoken for and more have anticipated to have been sold.

- Northern Hemisphere Weather Stories: Lots of watch will be put into European Union Rapeseed Crops, US soybean growing conditions, Western Canadian weather. Much of the United States in early stages of drought. European crop is out of dormancy and growing and looks great.

New Feature: Swipe right or left through the Interactive Charts Below:

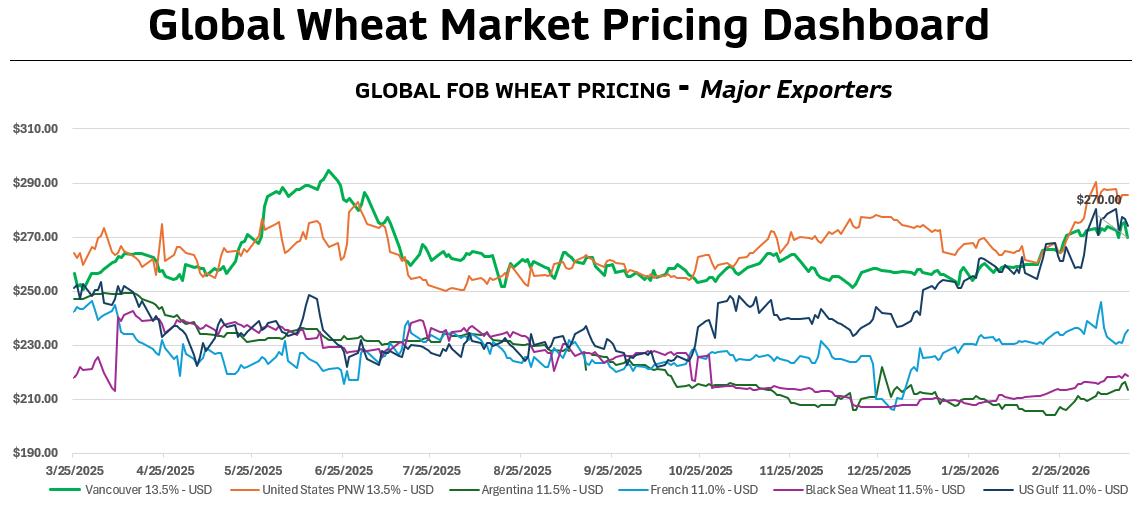

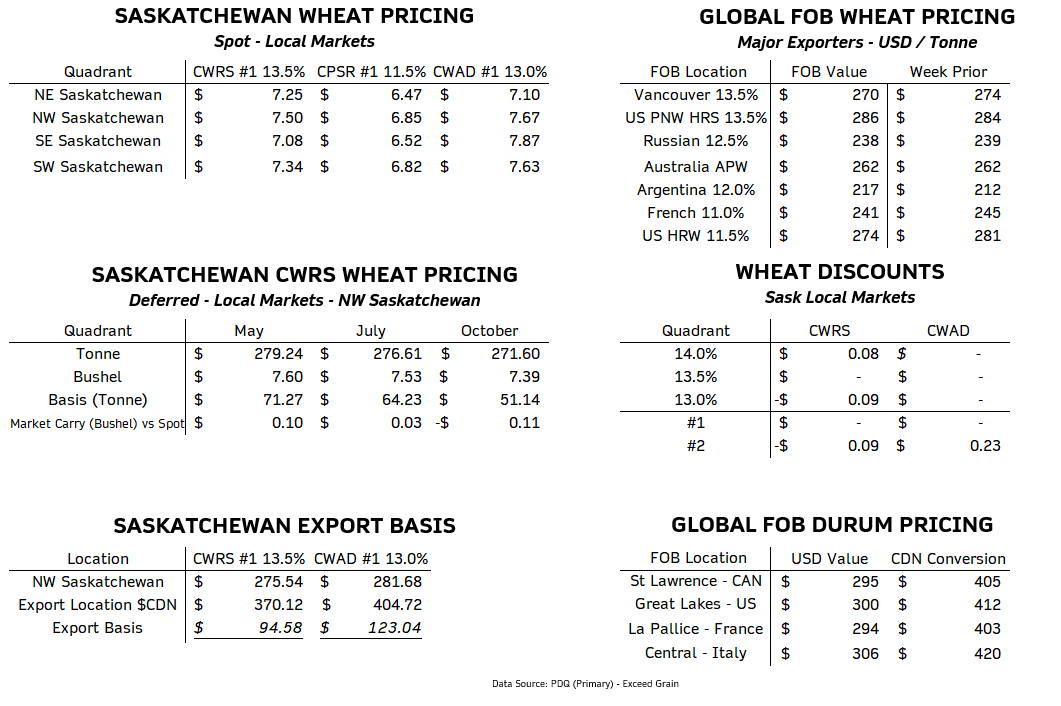

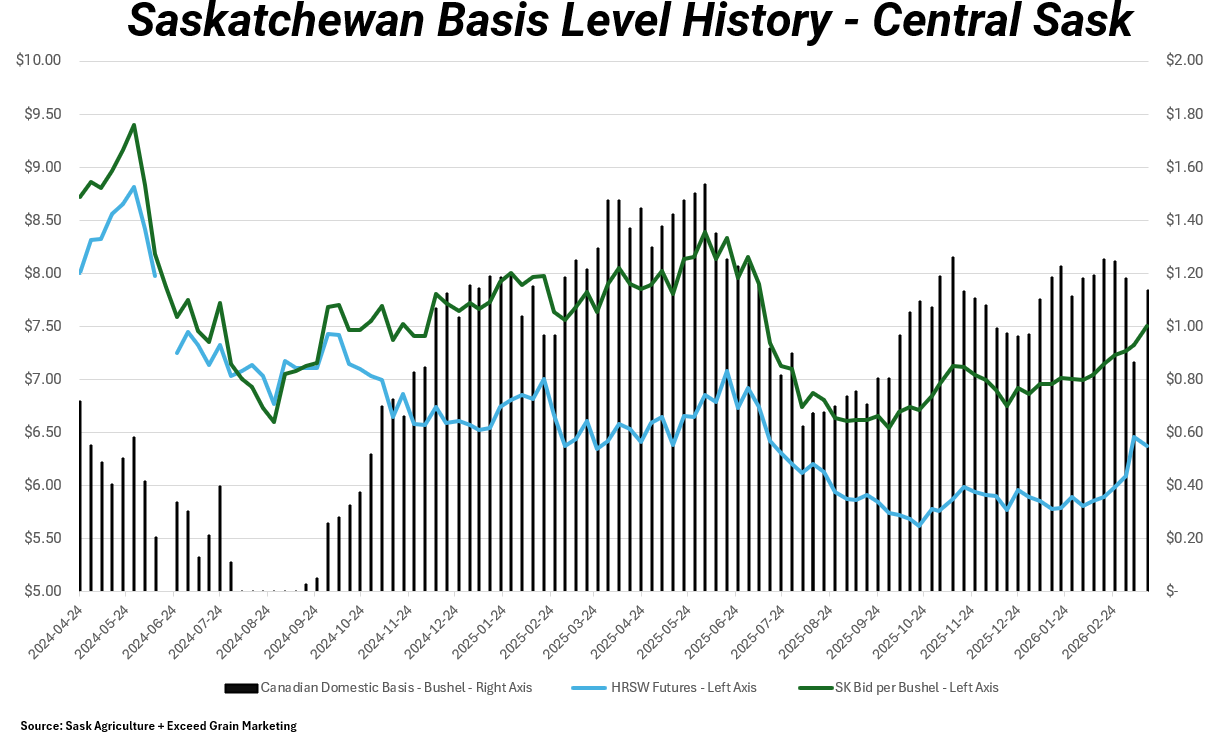

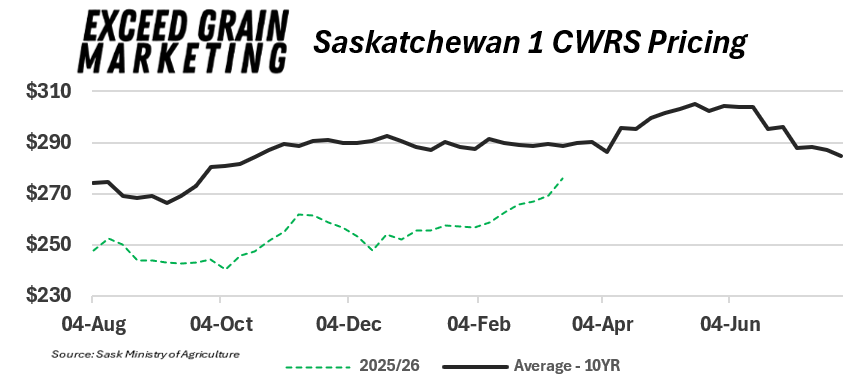

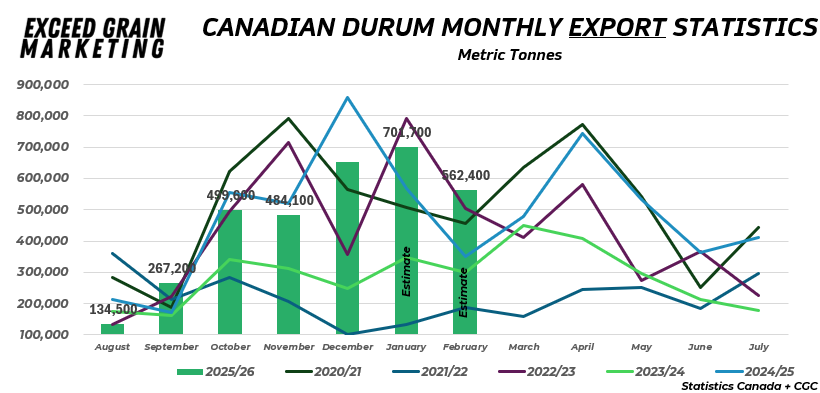

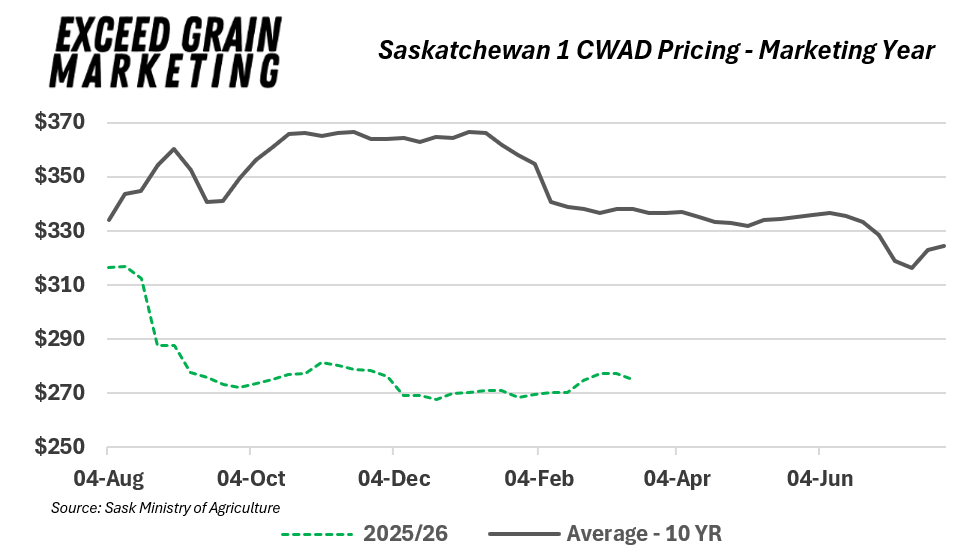

Spring Wheat + Durum Markets

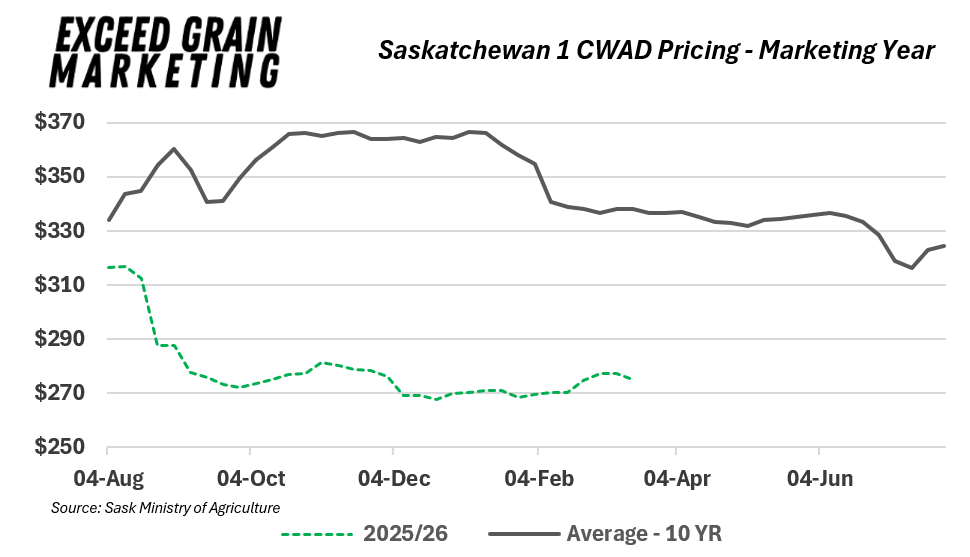

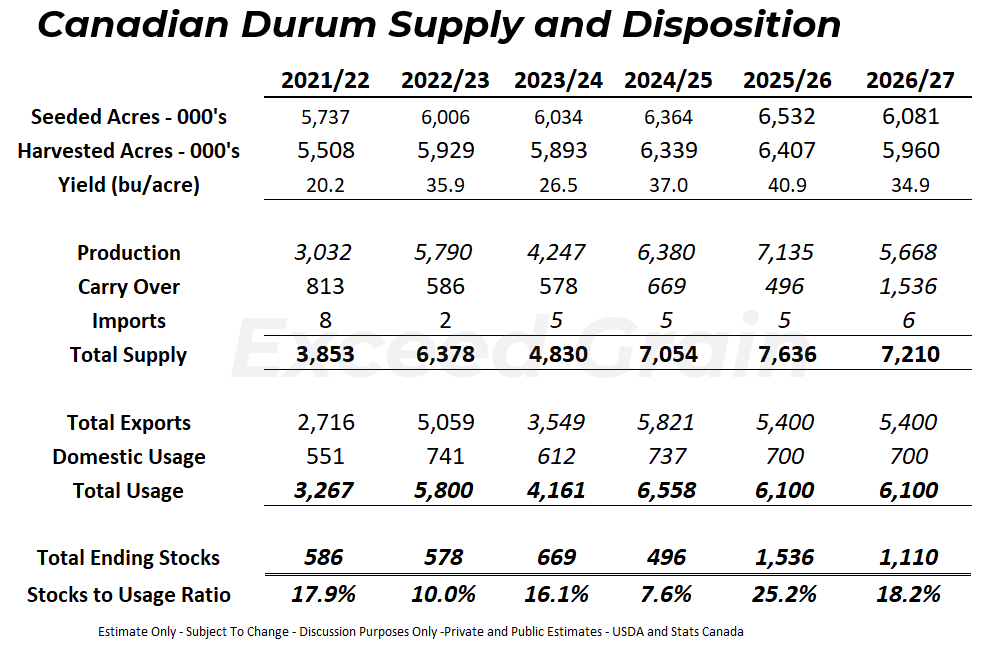

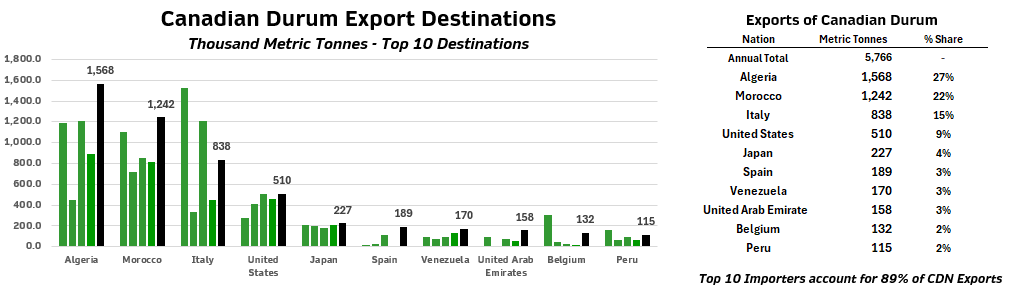

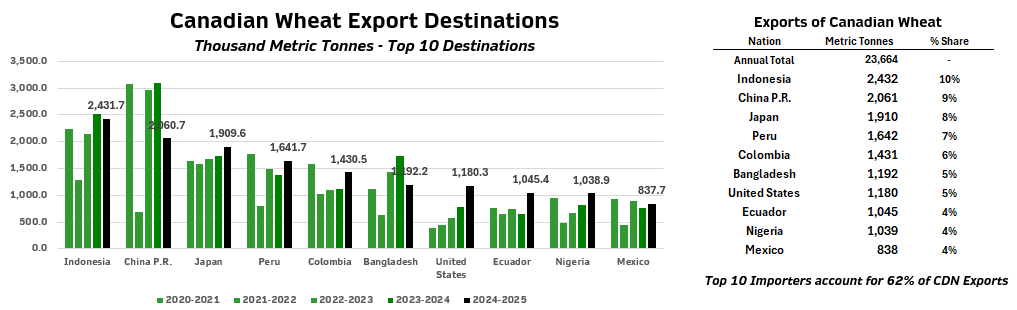

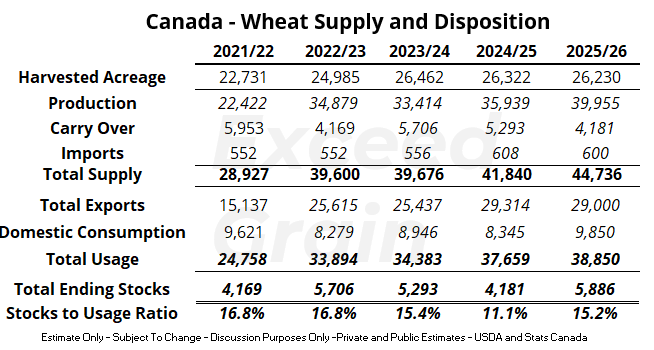

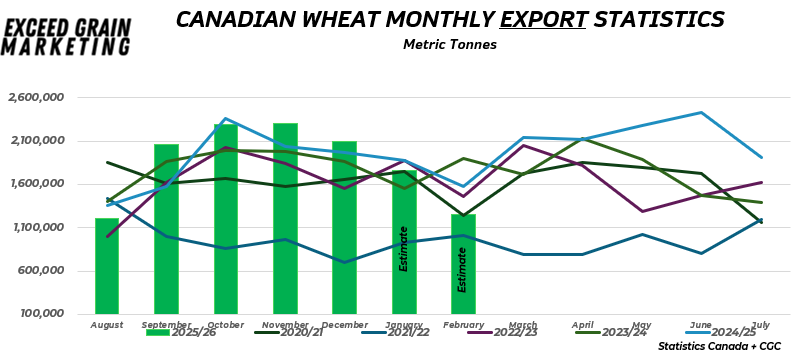

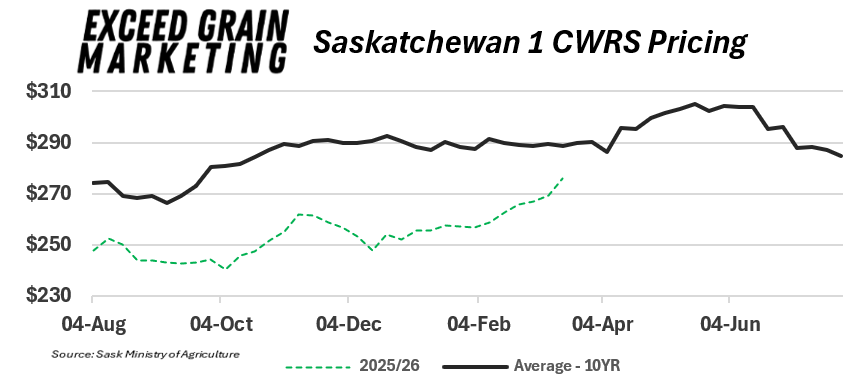

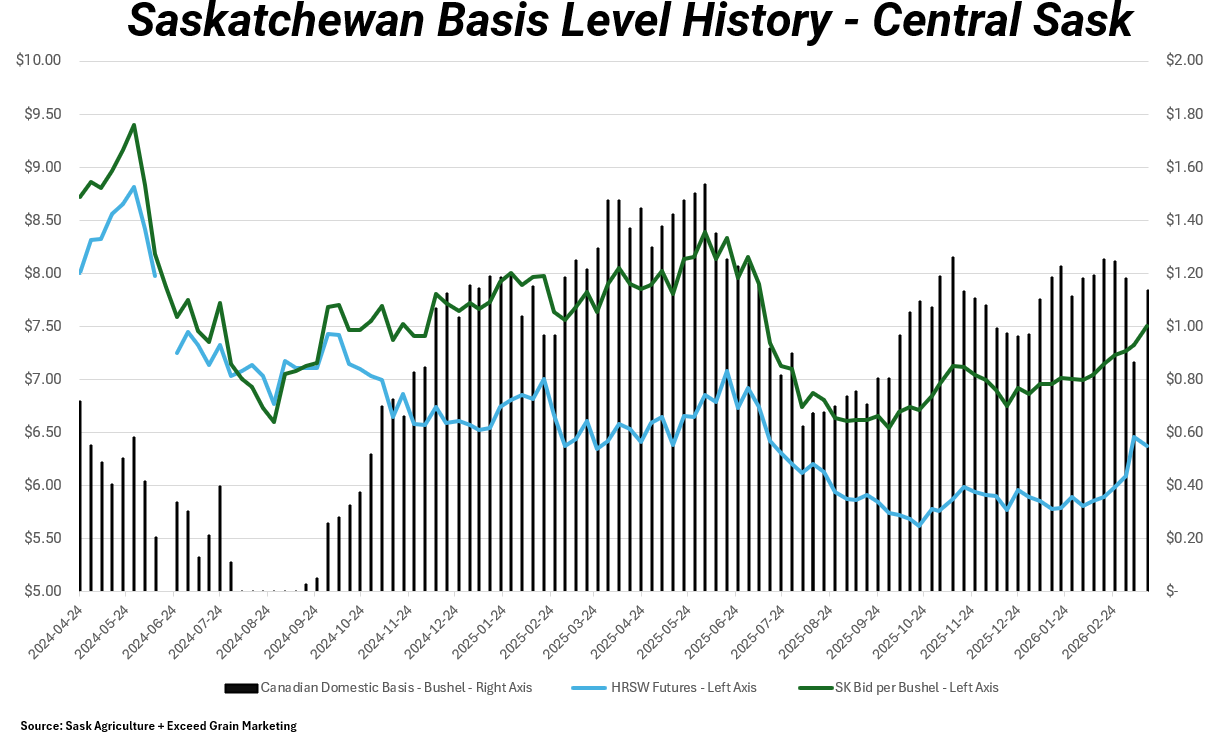

$8.25 bids central Alberta. Wheat bids playing close to $8.00 + per bushel values seen central Saskatchewan. Central Manitoba $8.50 and will benifit from the reopening of the Great Lakes shipping season as they begin to move grain after the winter shutdown. Slowing wheat export pace but still strong year over year up 5%. This has been slowing as was 15% ahead of pace at beginning of year. We have been seeing more of an emphasis from elevators to move canola and less wheat as export prospects improve for that crop but it seems that elevators have a good grasp on the values needed to grab tonnes out of the system. Canadian wheat still priced lower than other wheats of similar class and shipping competitively globally. Saskatchewan Durum values between $7.60 and $8.00 and appear flat. Great lakes and eastern shipping possible again.

What to Watch For In Wheat Markets:

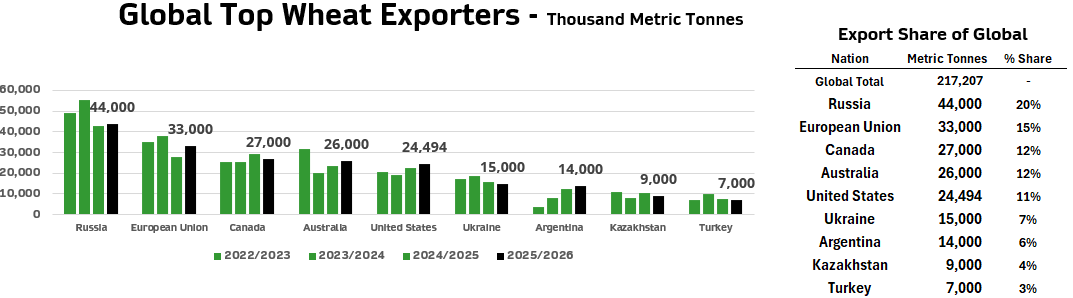

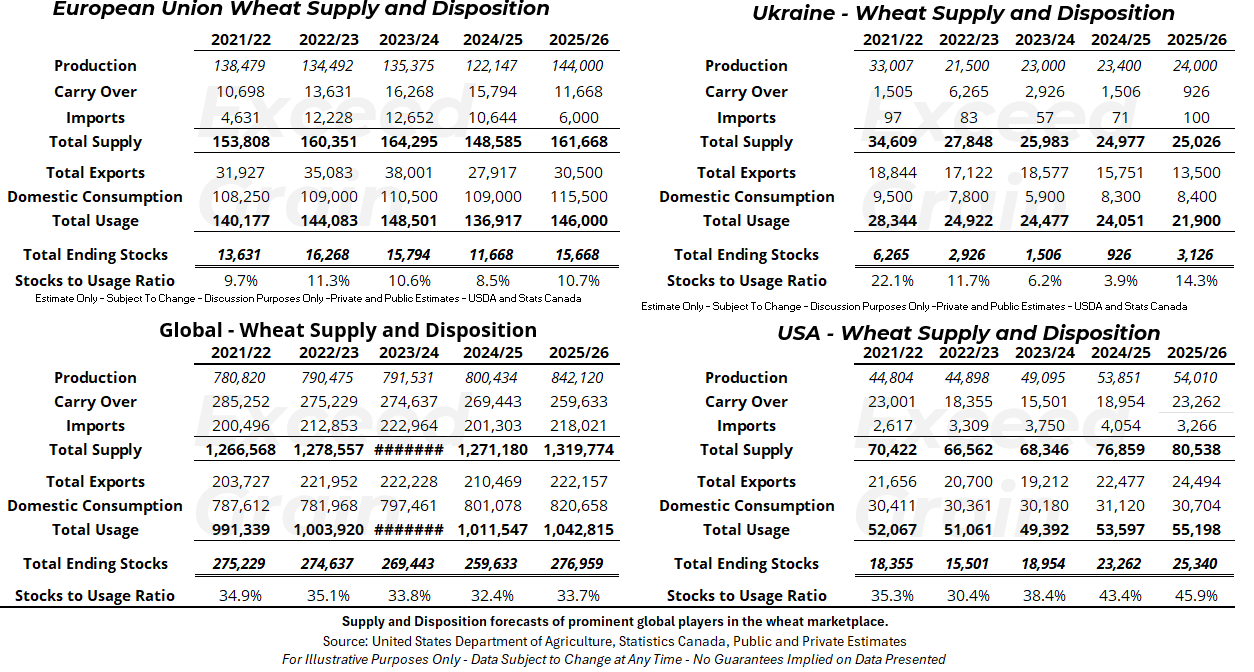

- Need to see continued strength in export pace for all wheat. Larger supplies in the market globally have been reported but the burdensome carryout can be partially mitigated by stronger exports. Many agencies reporting record global consumption of wheat which is overshadowed by the consistent market narrative of larger supplies. Exports up 5% year on year

- Canadian wheat export pace is good, but falling back from prior highs. Each tonne that gets shipped, milled and fed out or consumed is another tonne that does not sit on our balance sheets at the end of the year. Tightness creates price opportunities although we Need to chew through a larger crop overall. If demand weakens, we will see basis levels soften. Globe focused on larger crops in Argentina and Australian.

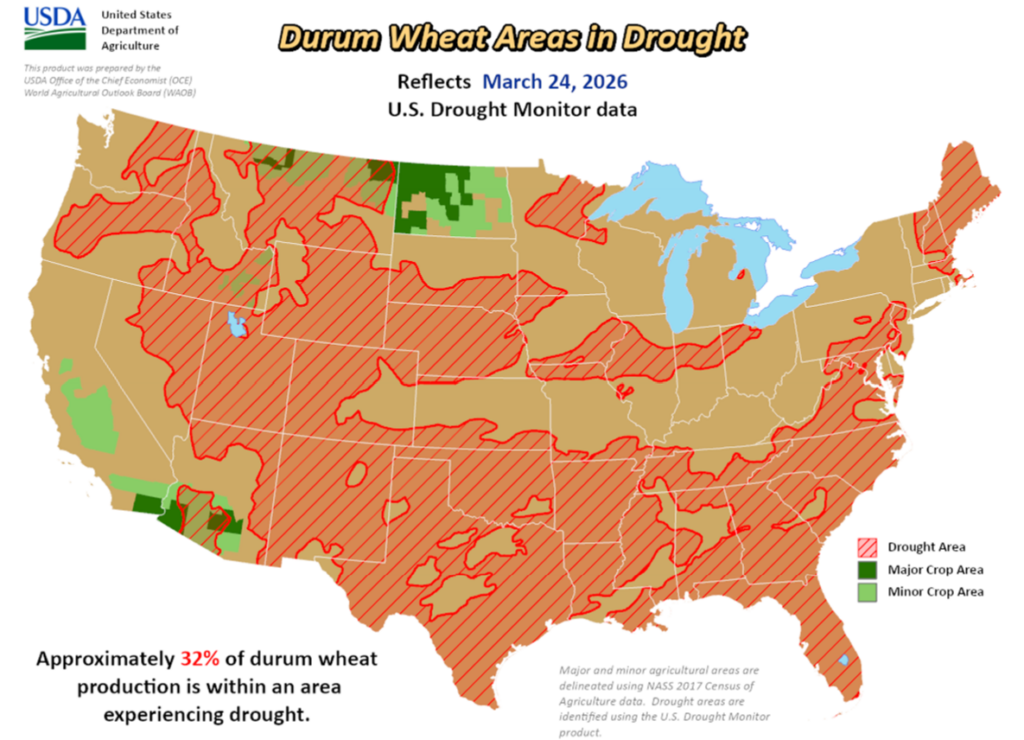

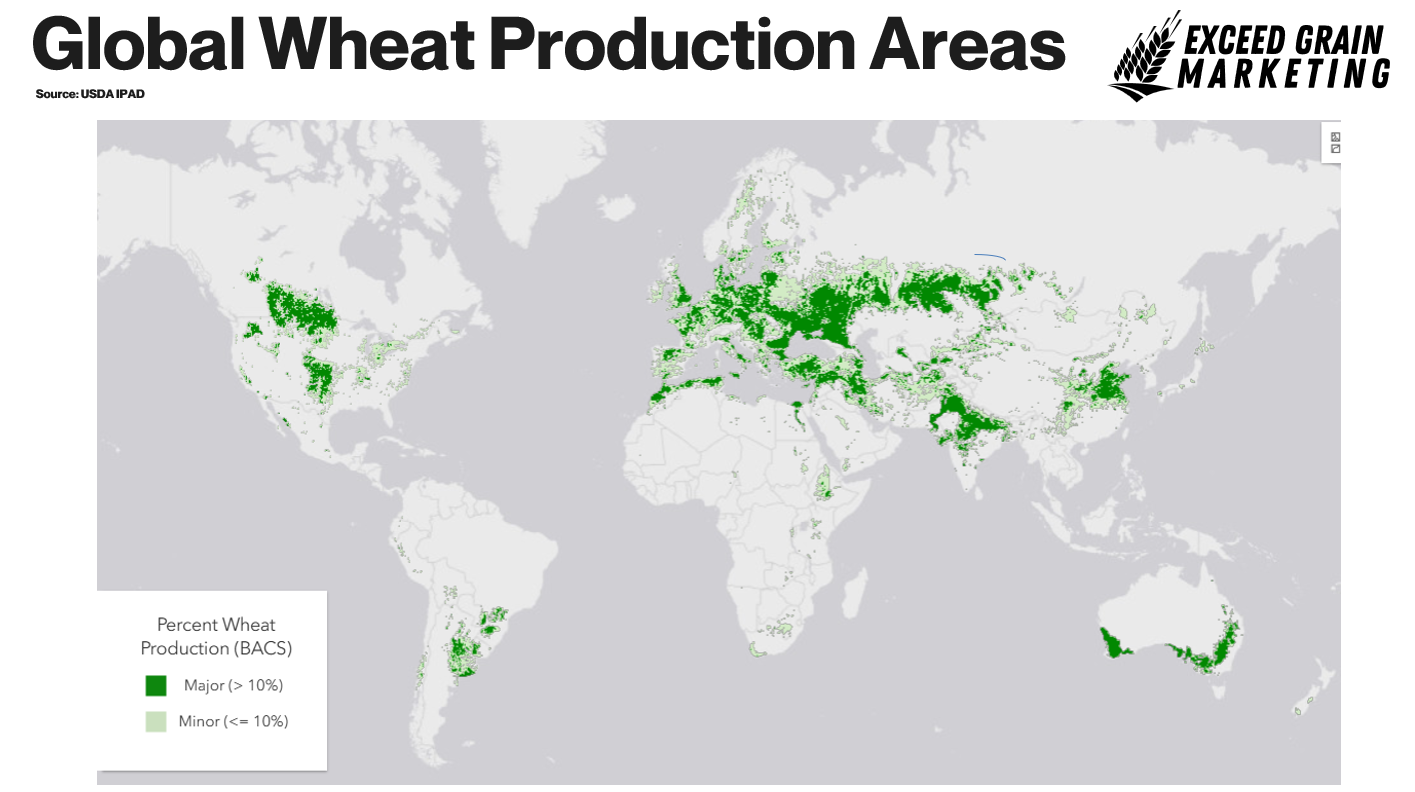

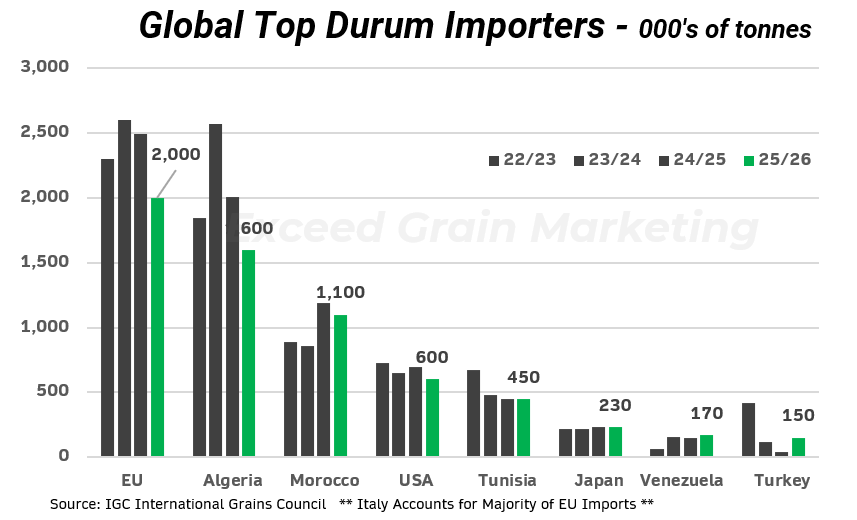

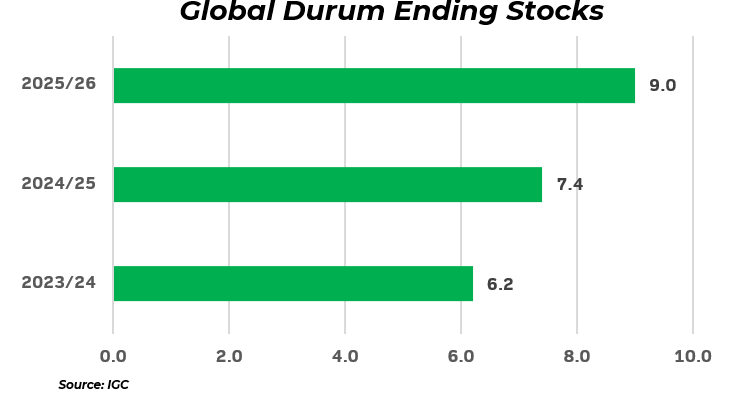

- For all Wheat, Durum and Spring Wheat, markets will be watching how the crops overwinter. Watch Euro Region, USA winter wheat regions for wheat overwintering. Watch French, Italian and North Africa for indications on durum crop quality. The region looks good so far. There are no issues to report and will keep markets uninterested for the time being. If drought or any other issue happens on the tail side of winter dormancy, there is opportunity.

- Market will focus on Demand through until late March/April and then look at how the crops coming out of dormancy in European Region, Black Sea and North America. We will see how northern hemisphere crops tend to shape up. Dry in some key growing regions of the United States for winter wheat.

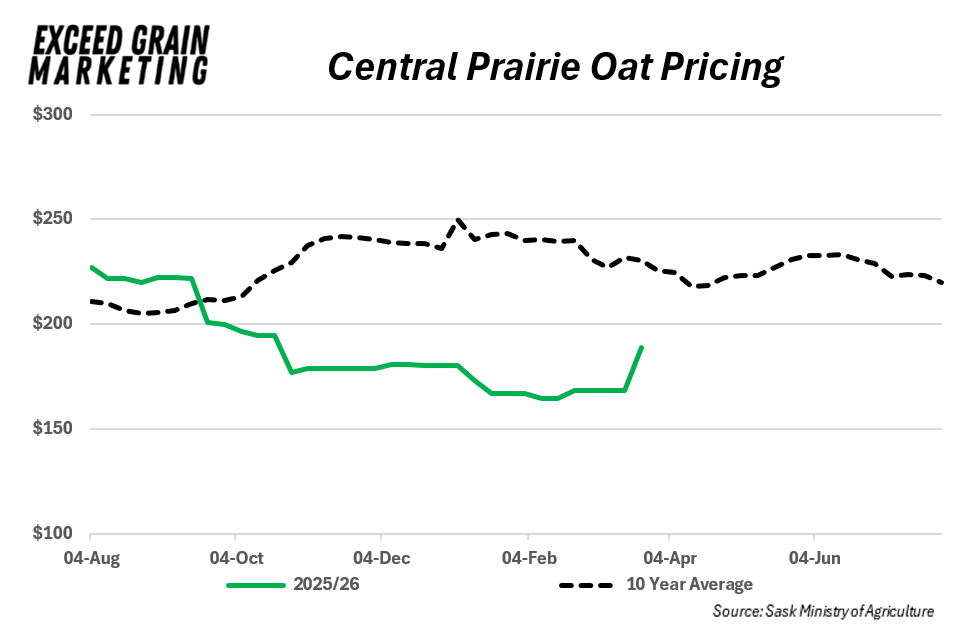

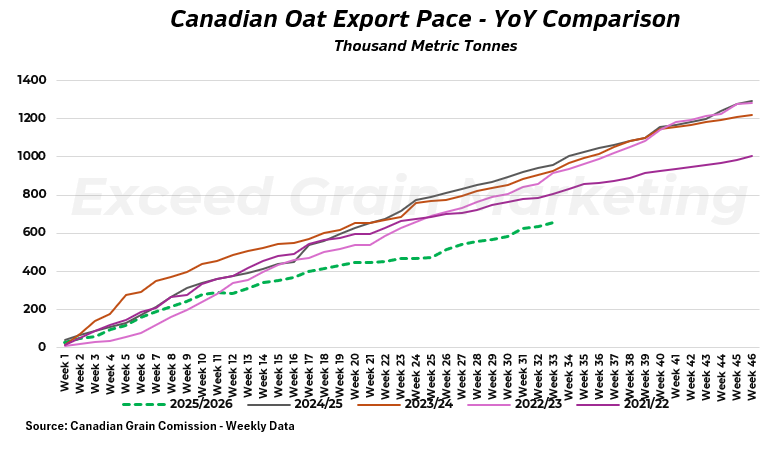

Oats – Early March Stats Can Seeded Acreage report showed less oat acres year over year but the sentiment from the market it that those acres could shrink yet. Many annecdotal producer reports has the crop down significantly. Seeing oat bids pick up slightly but still max $3.50 Central Sask up from $3.25 last week and touching $4.10 in central Manitoba. Canadian stocks report out February 6th showed less oats than anticipated from the market. Oat production was up around 600,000 mt from last year but stocks in the stocks report only showed a 200,000 mt gain. Some divergence in inventory estimates. Oat supply and disposition does not look overly burdensome by any means when compared to other crops. One thing of concern here although is how slow exports have become on oats. Supply and Disposition chart provided for readers. Export pace for oats and remaining crops in report below. Oat acres expected to drop significantly upcoming year in favor of other crops.

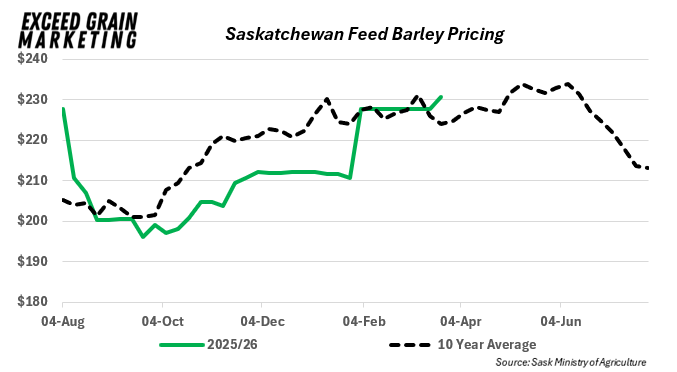

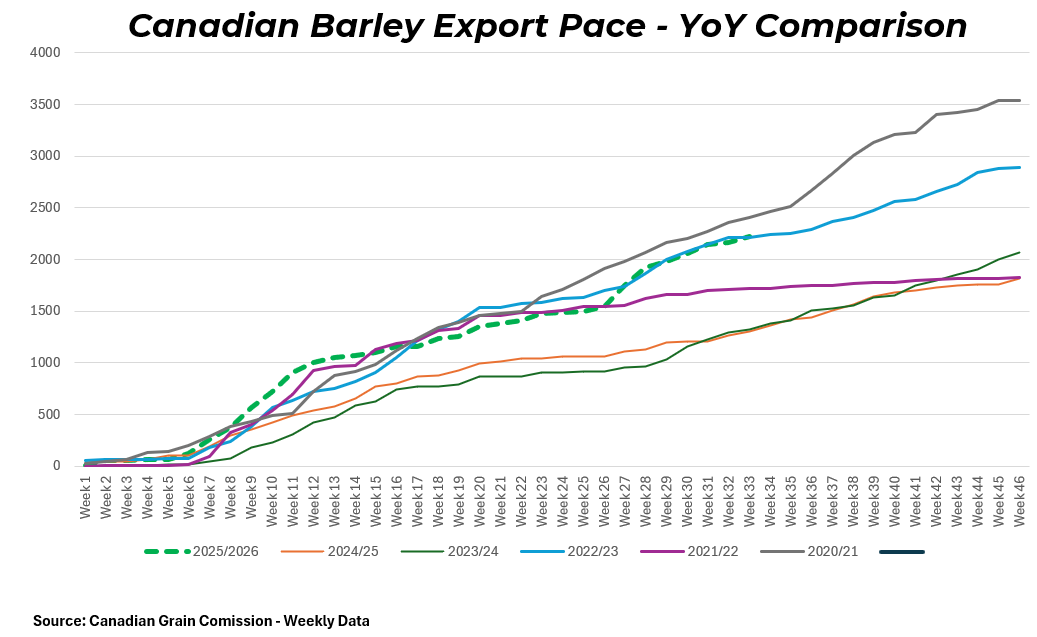

Barley – Feed Barley Values very strong. $6.00 Plus in many cases. Acreage estimated to be up 5% year over year. crop size revised higher by Statistics Canada. Exports have been relatively strong up 58% from last year. New crop barley bids up over $5.10 for new crop. Markets expecting a slight bump in acres for upcoming year. Major ramp up in exports in the past month. Canadian barley has been pricing itself well globally. Domestic user bids from the Maltsters have been able to cover off their needs. Starting to see some malt bids show up for old crop but $5.25+ range and keeping very little premium to feed barley. Producers need to fully understand their barley quality before making marketing decisions. Old Crop Feed values have improved to $5.50 to $6.00 and exceeding the value of Malt in many instances. Barley crop overall came in at a very large 9.7 mmt which is up year over year. Better exports have been helping to chew away at supplies .

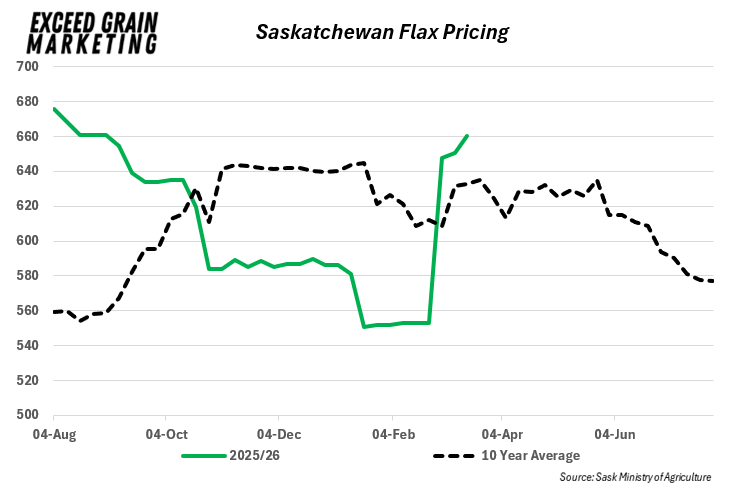

Flax – Canadian acres up large for next year. 21%. Canadian flax crop has been subject to respectable supplies. There has been a larger Kazakh flax crops and Canadian stocks to usage is forecasted to be quite large unless some unforeseen export demand does show itself. Values picking up on vegoils relative strength. The larger crop out out Kazakstan will keep global prices in check. Flax has been flat to lower most of the year but picking up value recently.

Canary Seed crop is expected to be of healthy production and push ending stocks to 171,000 tonnes which is considered a very heavy carryout. Expect less acreage in 2026. Canary seed bids have picked up slightly in the past weeks but bids still in the $0.20 per pound range and down from the $0.30 per pound seen back in the spring prior to seeding the crop. Canary seed typically carries larger ending stocks due to producers willingness to store the crop and its general lack of being used as a cashflow crop. This has sometimes been shown to benefit producers as the crop is held in “tighter hands” and ending stocks cant be used as the only tool when looking at the canary seed crop.

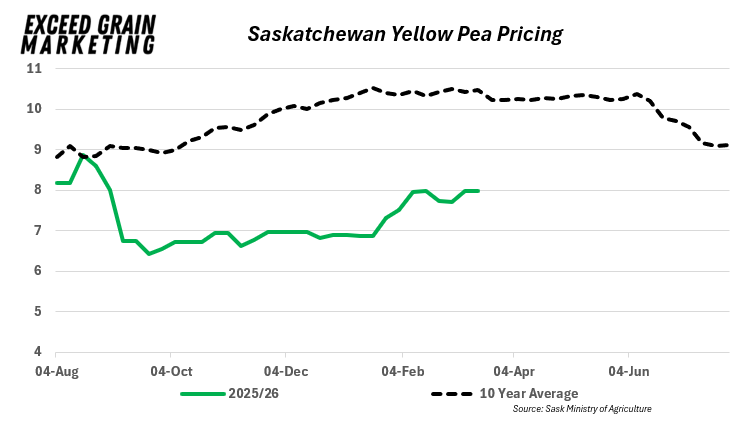

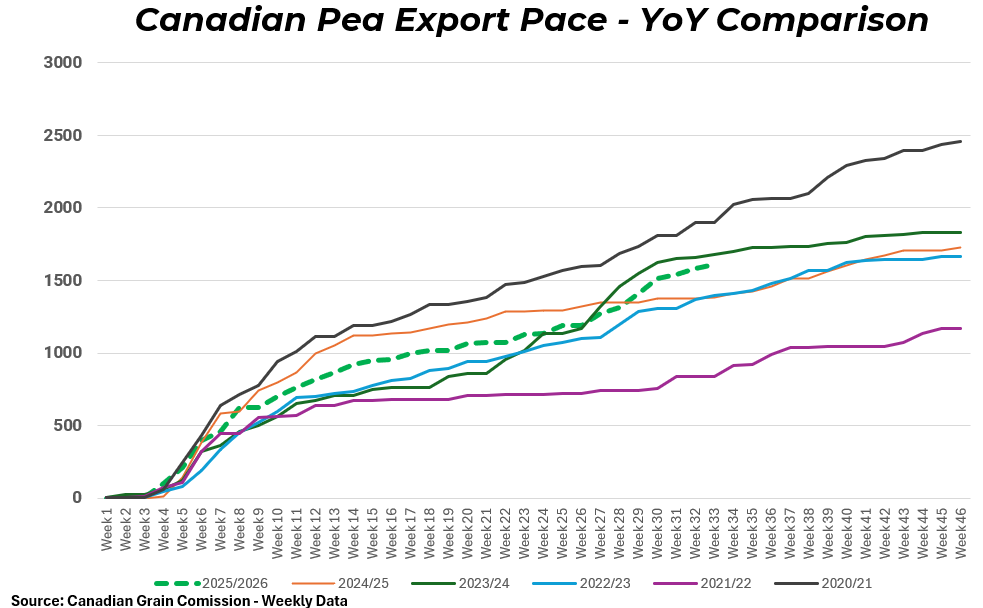

Peas – China has made a move to reduce pea tariffs to 0% from 100% and this will allow Canadian peas to fit back into that market. Domestic Pea Bids up by $0.50 per bushel to $8.00 after sitting at $7.00 for much of the fall and winter. China took around 500,000 tonnes of peas from Canada in 2024 and is a big offload of around 20% of the crop. India has a 30% tariff on Peas. Combined with larger overall supplies, the market will likely be met with farmer selling. New crop bids not anticipated to be aggressive and in the $8.00 per bushel range. Large carryout expected. Need to See China take tonnage to reduce the carryout. Carryout looks large regardless. Seeing foriegn yellow pea bids increase and letting markets play more with that $8.00 yellow market. Pulse acres expected to be down in general year over year. Acreage estimates out early March for Canadian crops.

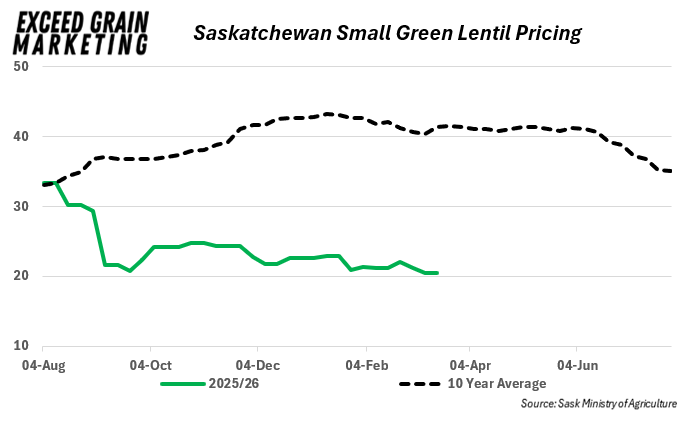

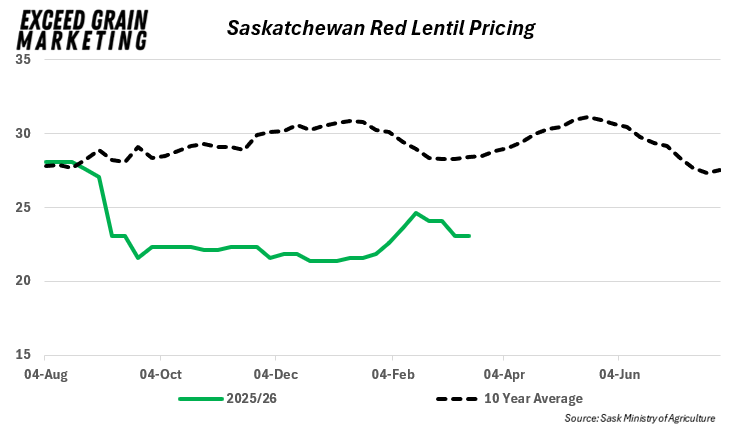

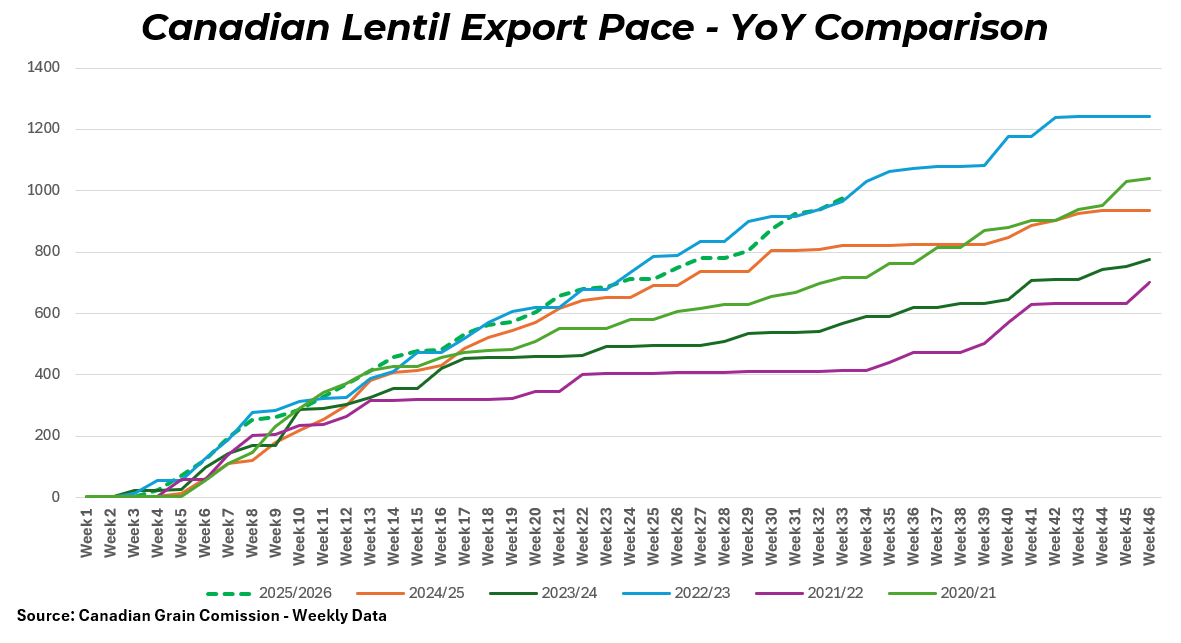

Lentil values sit in the $0.23 to $0.25 range on Reds. Small greens $0.20. Australian crop is large. Overall due to significant domestic production. We are now dependent on how winter crops will shape up in India as harvest nears. No issues out of there Heavy stocks will take time to work through. Indian prices for Yellow Peas, Red Lentils and Green Lentils are picking up and seeing red lentil values gaining ground slowly in Australia and Turkey, keeping some support and life in the market.

Soybean values for New crop in the $13.50 Manitoba range. Old crop remain in the $13.00 with the odd $13.50+ bid floating around. Soybeans spent the majority of Summer and into the fall months of October in the $11.00 to $12.00 range before gaining ground peaking around $13.75 prior to year end. Export pace has been quite strong but tends to flatten this time of year. Manitoba is the main focus in our market reports and producers able to find some marketing opportunities recently but need to be cognizant of how the pace could play out as exports typically very small further you get into winter . Soybean market is focused on the larger South American crop and what planting intentions could be in the United States for this upcoming spring. USA Seeded acreage report out March 30th.

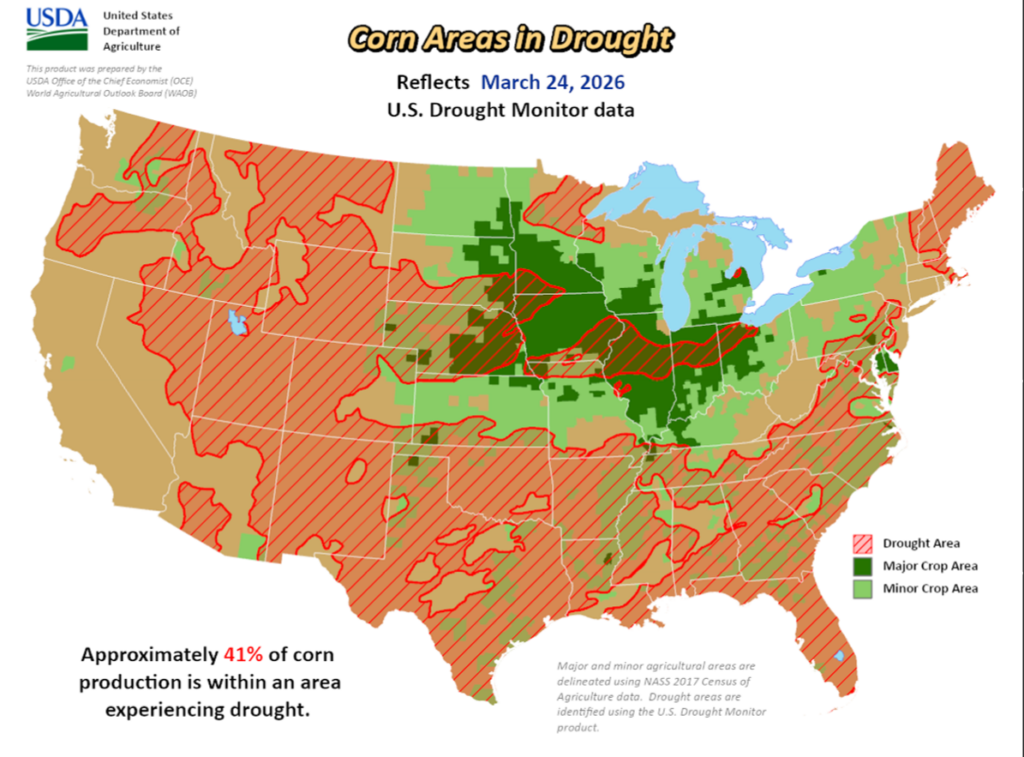

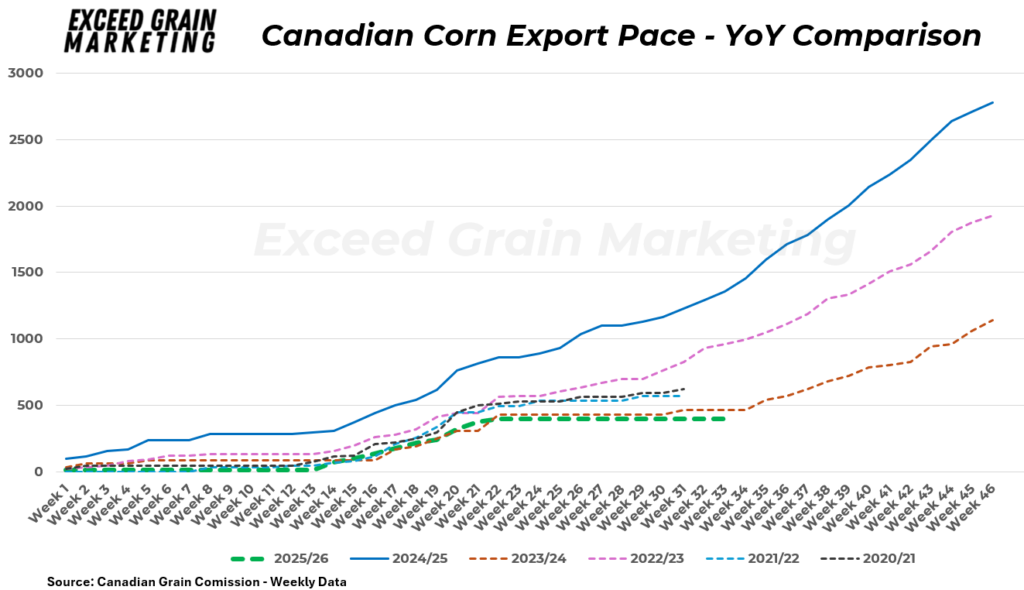

Corn values in Manitoba at the $5.25 picked up range. Values strengthen into Spring and fall bids stronger yet showing the market is comfortable with todays stock levels. New crop $5.75 roughly central MB. Manitoba cash values sitting $1.00 lower than last early winter. More abundance of feed grains and corn in Manitoba in general. Corn domestic usage is about flat with last year but exports are quite low, not unusual for the time of the season. Global corn stocks forecast looks like it will be on the tighter side of things and will if demand stays up, any risk to South American production could shake up markets. United States corn and bean regions looking dry before spring. 46% of the region in drought for corn. US Export pace is far surpassing early expectations and a drawdown in US or Global Stocks could be bullish

Our market intelligence reports incorporate information obtained from various third-party sources, government publications, and other outlets. While we endeavor to maintain the highest standards of accuracy and integrity in our reports, we acknowledge that the information provided may contain inadvertent errors or omissions. As such, we accept no liability for any inaccuracies or missing information in the data presented. Furthermore, these reports are not intended to serve as standalone investment or financial advice. We strongly advise that any financial or investment decisions be made in consultation with a professional market advisor. Reliance on the content or forecasting provided within of our reports for making financial decisions without such professional advice is at the sole risk of the user.